Over the years, through regulation changes and plan design mandates, the three predominant types of defined contribution retirement plans—403(b), 401(k), and 457(b)—have grown more similar.

However, a number of key distinctions remain.

Understanding the nuances between these plan types can be daunting. But for those plan sponsors with a choice, like private tax-exempt 501(c)(3) charitable organizations, digging into the differences may help clarify which plan type, or combination of plan types, to offer. Below are the most significant distinctions among the three types of plans, in order of importance.

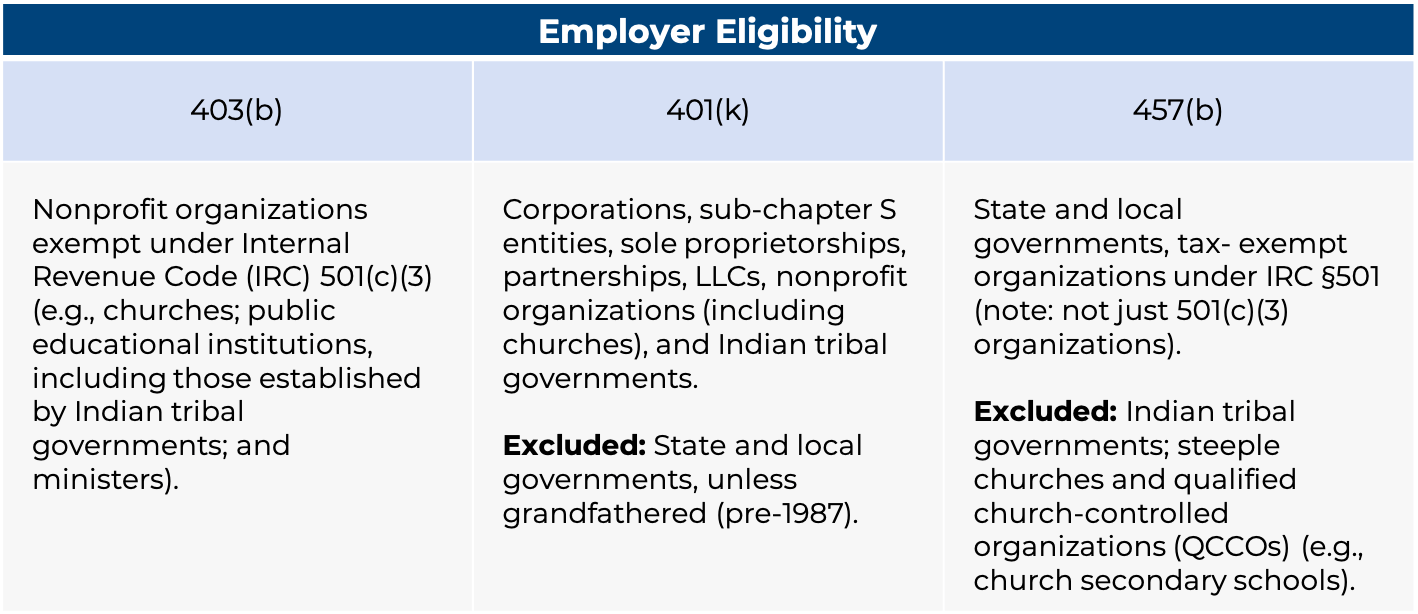

Employer Eligibility

One of the primary differences is the type of employer eligible to sponsor a particular type of plan. For example, state and local governments, public colleges, and universities may not offer a 401(k) plan unless their state maintained a 401(k) plan that was established before 1987.

Likewise, private tax-exempt organizations that are not 501(c)(3) educational or charitable organizations, such as associations and clubs, may not maintain a 403(b) plan. And while public and private colleges and universities may maintain a 457(b) plan, the rules governing these plans vary widely depending on employer type.

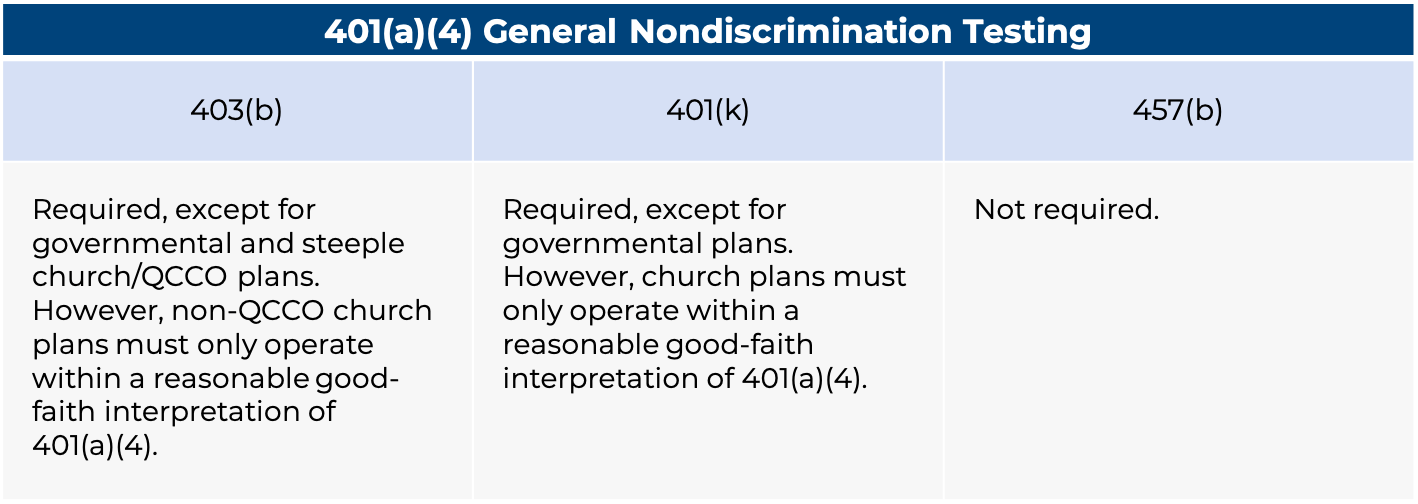

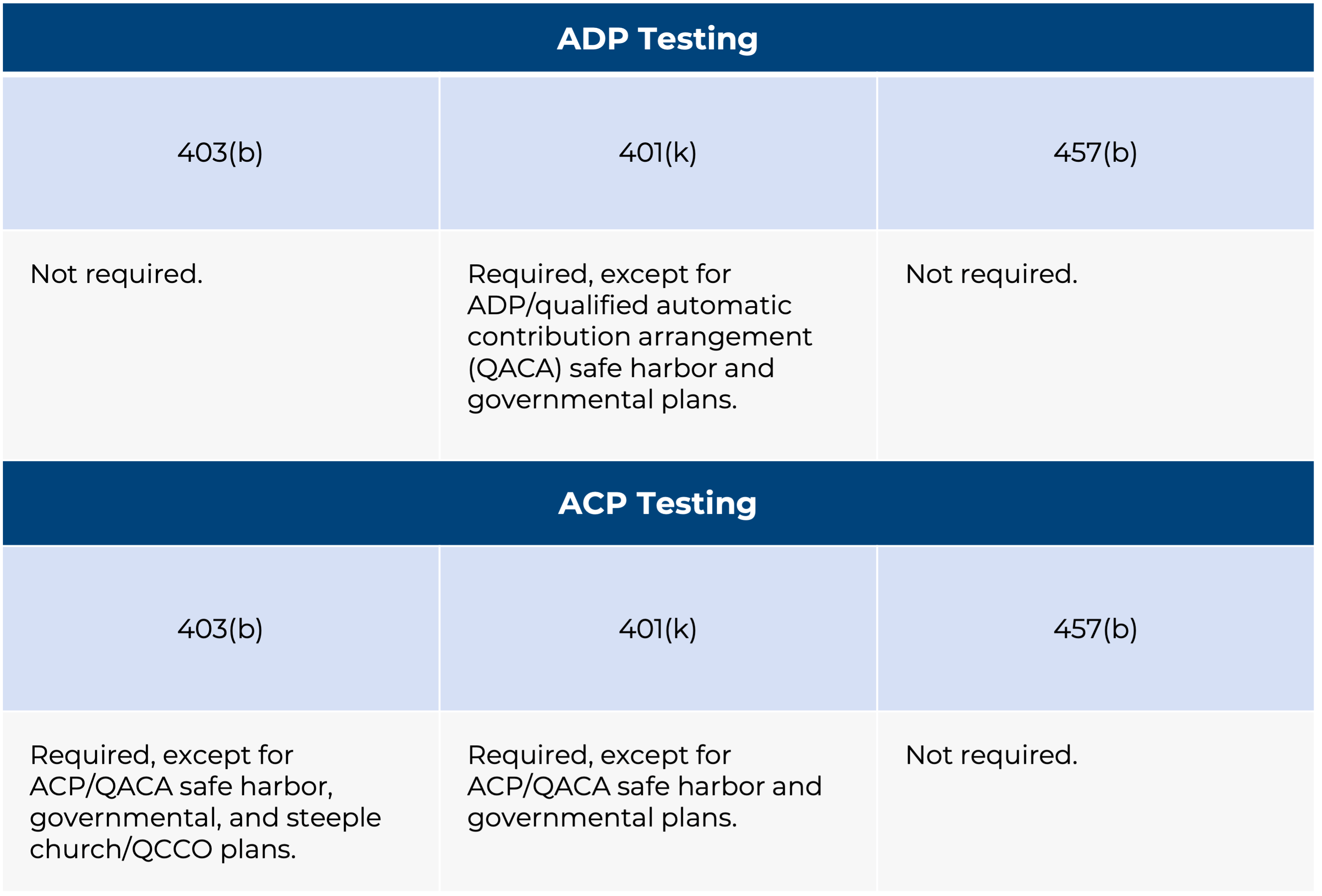

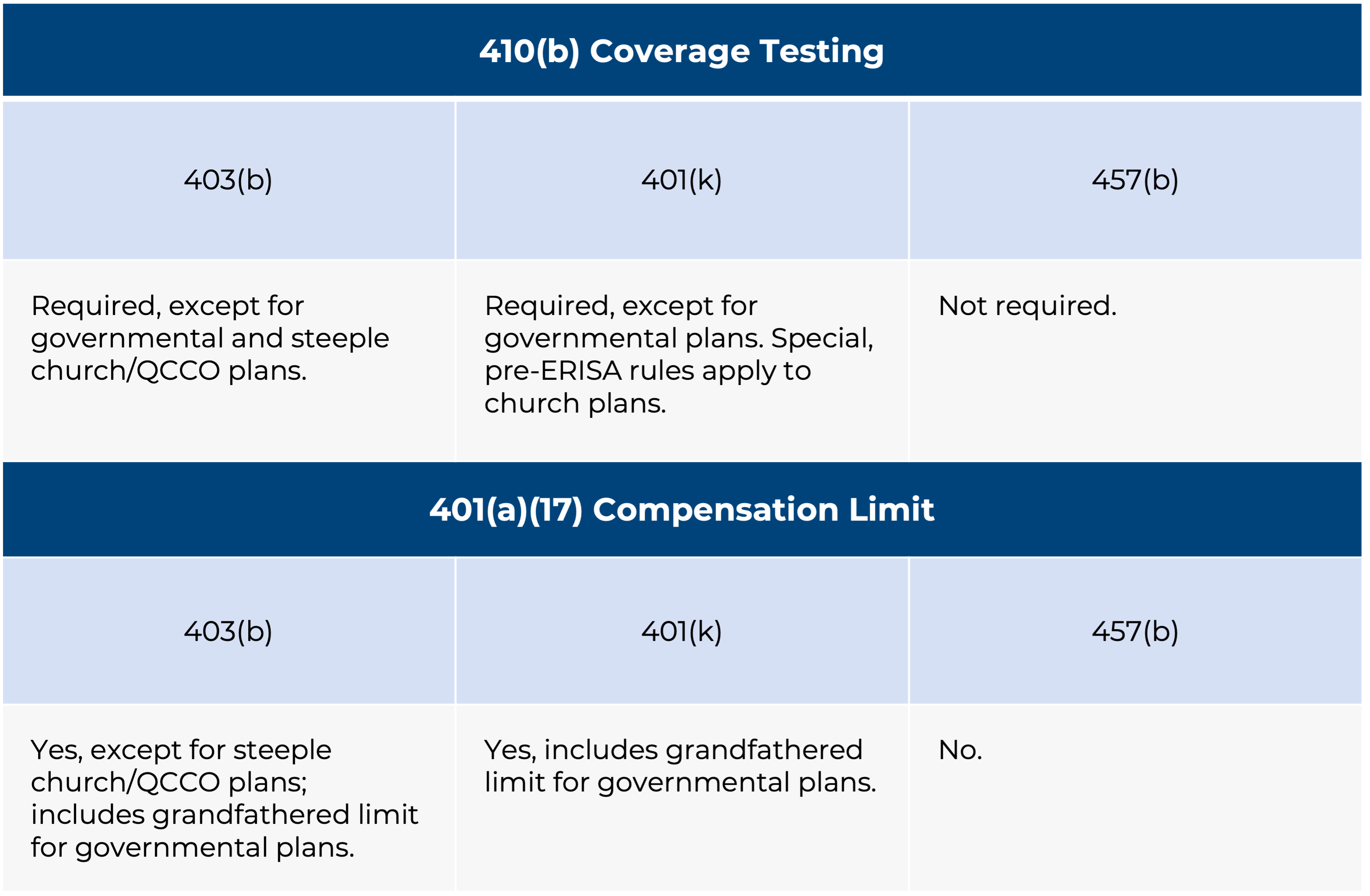

Nondiscrimination Testing

Nondiscrimination testing in 401(k) plans requires that highly compensated employees (HCEs), defined in 2025 as those earning more than $155,000 in 2024, stay within a specific contribution rate determined by the average contribution rate of non-highly compensated employees (NHCEs).

This testing is one of the key reasons why many private tax-exempt 501(c)(3) charitable entities, such as hospitals and colleges and universities, continue to use 403(b) plans instead of 401(k) plans. For 403(b) plans, it is unnecessary to test salary-deferred employee contributions. As a result, these HCEs have no additional limitations imposed on their ability to save other than the overall IRS 402(g) restrictions.

For example, in a typical private 501(c)(3) tax-exempt organization, unmatched elective deferrals for NHCEs average 2 percent (this average includes individuals not deferring anything). At this level, HCEs in a 401(k) plan are limited to approximately 5 percent of pay rather than the 2025 IRS limit of 100 percent of pay up to $23,500 per year (or $31,000 if age 50 or older, $34,750 if age 60-63). Thus, these higher-compensated plan participants face significantly restricted deferral limits, which are otherwise moot in a 403(b) plan.

A 457(b) plan presents the opposite problem for private tax-exempt entities. A 457(b) plan, sponsored by a private college or university that is not a 414(e) religious organization, is of limited use, since these top-hat plans are required to discriminate in favor of HCEs. Thus, they do not serve as the primary retirement plan for these organizations but are instead used as a supplemental plan for select groups of management employees.

An advantage of 457(b) plans is that employer contributions of any type can be discriminatory, whereas in 401(k) and 403(b) plans, employer contributions must be tested for nondiscrimination (with the exception of certain organization types exempt from testing).

Nondiscrimination testing is not a consideration for certain types of organizations. For example, governmental plans, such as those sponsored by public universities, are not subject to nondiscrimination testing, and 457(b) plans can be offered to all employees at these organizations.

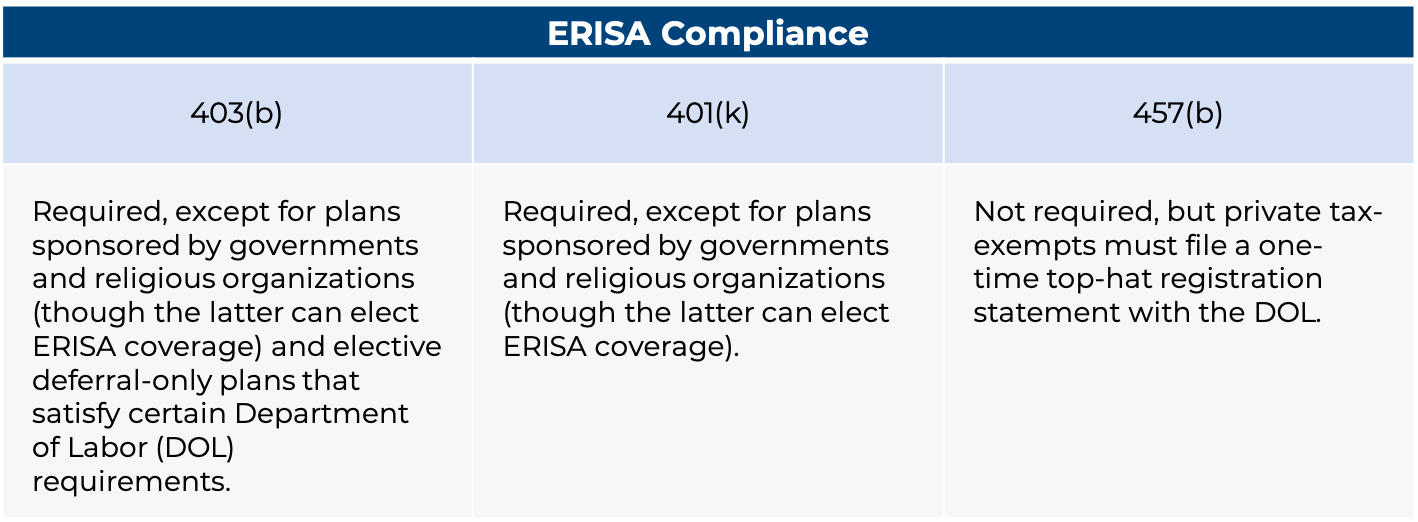

ERISA Coverage

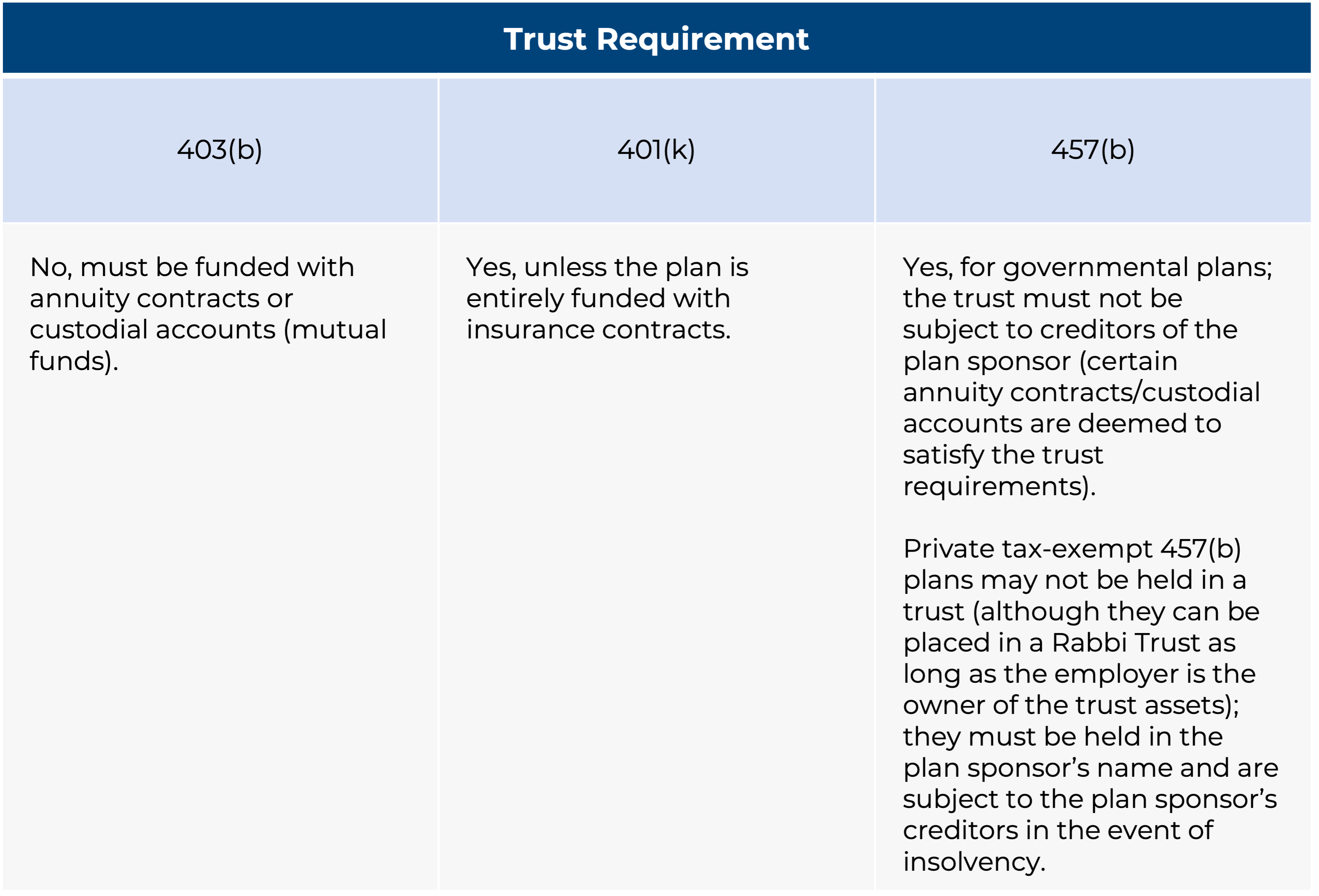

Another defining feature of 403(b) and 457(b) plans is that elective deferral-only plans of private 501(c)(3) charitable organizations are generally exempt from the Employee Retirement Income Security Act (ERISA). While this is uncommon among 403(b) plans, ERISA exemptions are not a possibility for 401(k) plans. Note, however, that public entities and churches are not subject to ERISA, regardless of plan type; churches may elect ERISA coverage, but it is rare.

Private education employer 457(b) plans are technically subject to ERISA, but a single top-hat filing with the government essentially exempts the plan from ERISA requirements.

For 403(b) plans to be exempt, plan sponsors must only permit elective deferrals (no employer contributions) and satisfy several other requirements that generally restrict employer involvement in the plan. This exemption means that for these plans, no summary plan descriptions are required, no annual Form 5500s or summary annual reports are required to be filed and distributed, and an annual audit is unnecessary—the audit alone can be a significant cost factor as well as an administrative burden. While the 403(b) exemption is not as attractive as it once was due to new regulatory requirements, the ERISA exemption remains an important option for 403(b) and 457(b) plans, one that is unavailable in the 401(k) world.

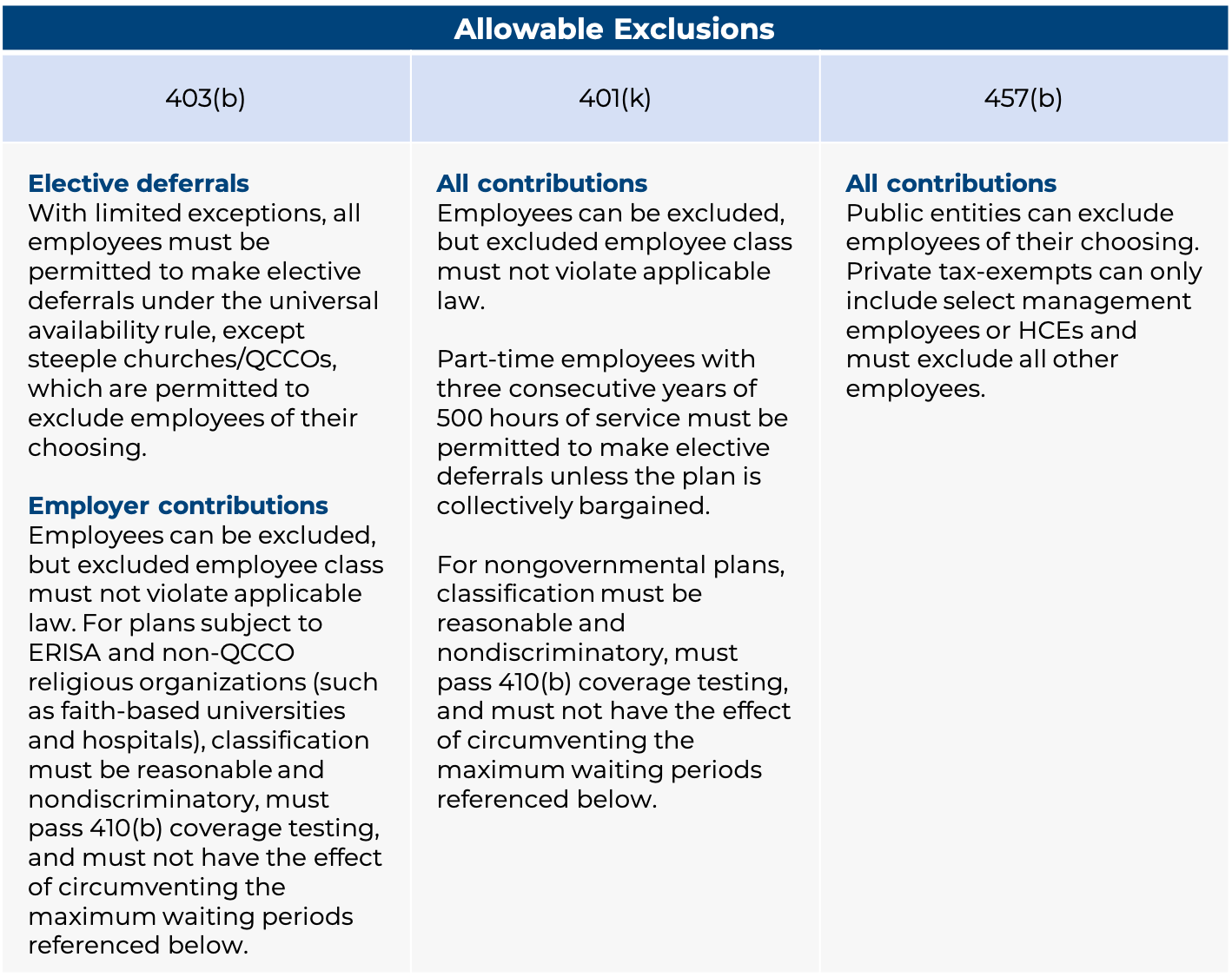

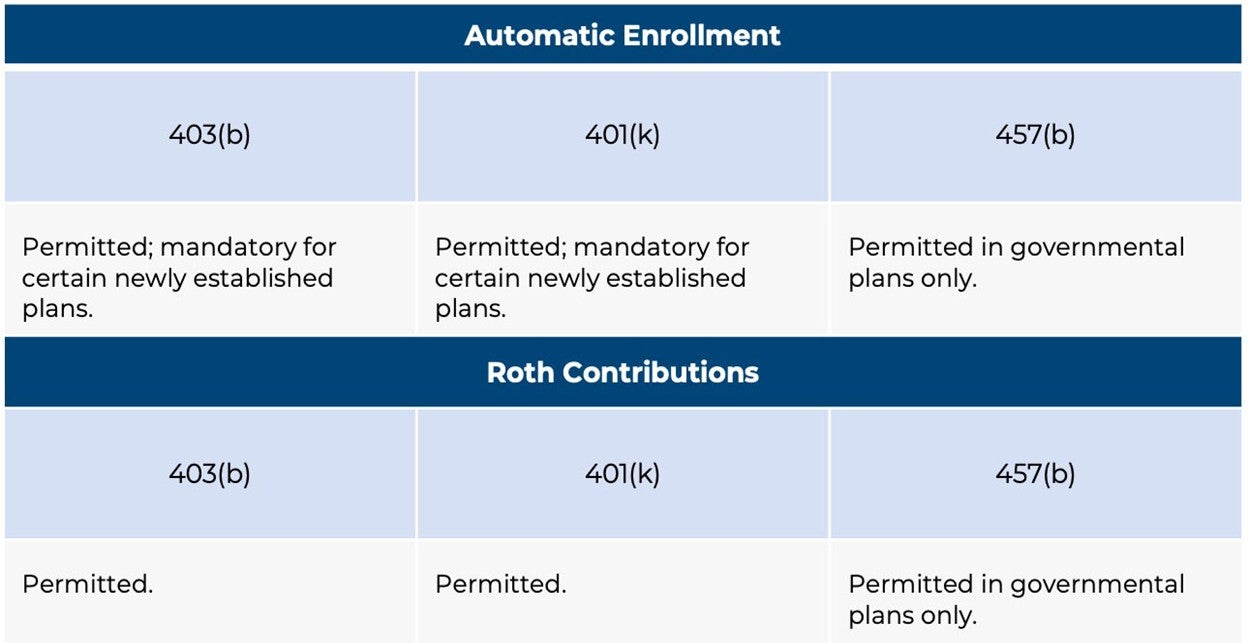

Universal Availability

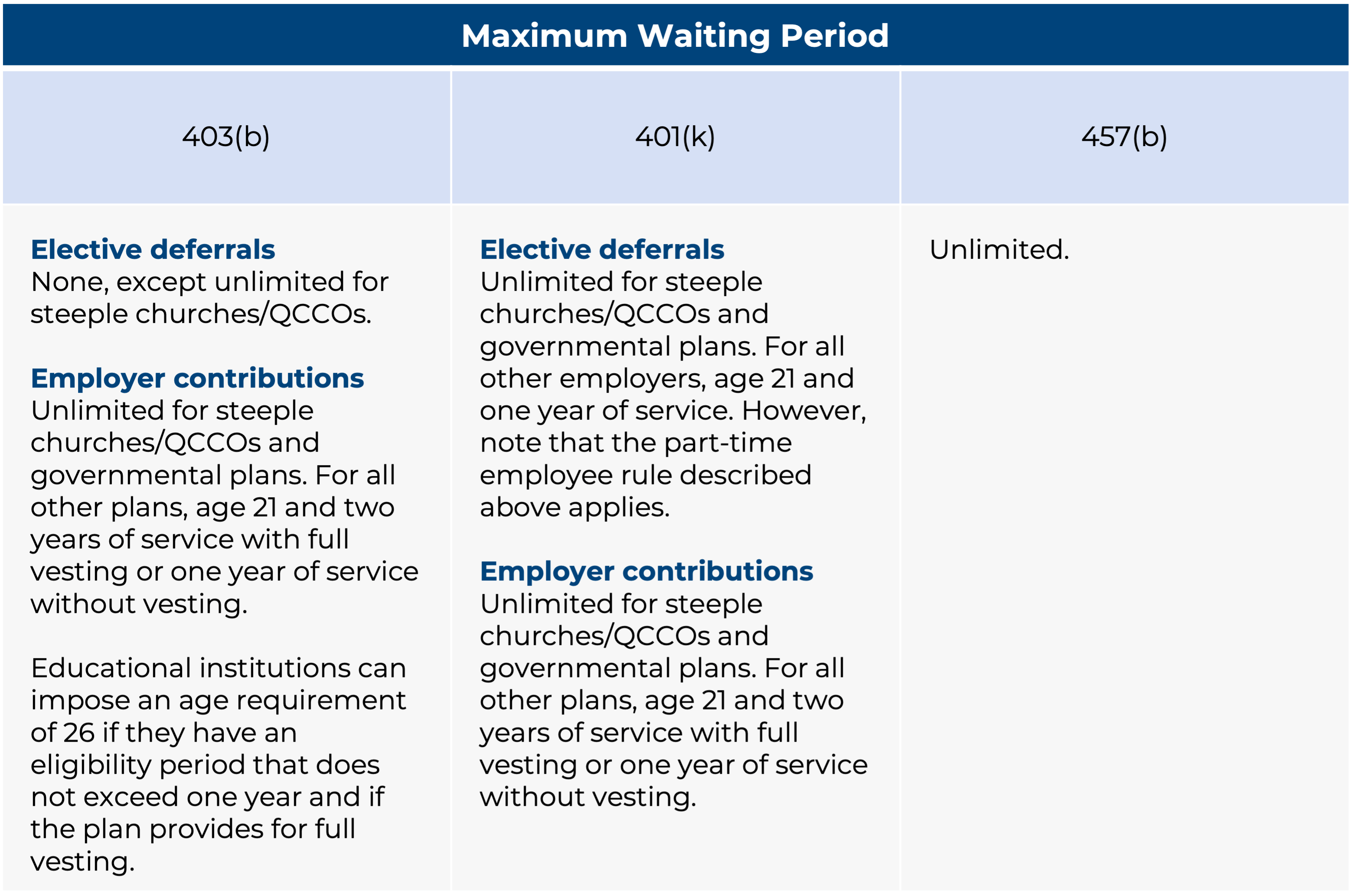

The universal availability requirement is unique to 403(b) plans. Universal availability requires that all employees, with limited exceptions, be permitted to make elective deferrals from the date of hire. This contrasts with 401(k) plans, for which eligibility to make elective deferrals can be restricted, subject to nondiscrimination testing requirements. It is important to note that the recently enacted Setting Every Community Up for Retirement Enhancement (SECURE) Act now requires the inclusion of certain part-time employees in these 401(k) plans.

Public 457(b) plans have no eligibility requirements, meaning that plan sponsors can allow all or any employees of their choosing to participate. As previously noted, private tax-exempt 457(b) plans can only permit select management and HCEs to participate. Additionally, independent contractors are permitted to participate in 457(b) plans, but not in 401(k) or 403(b) plans.

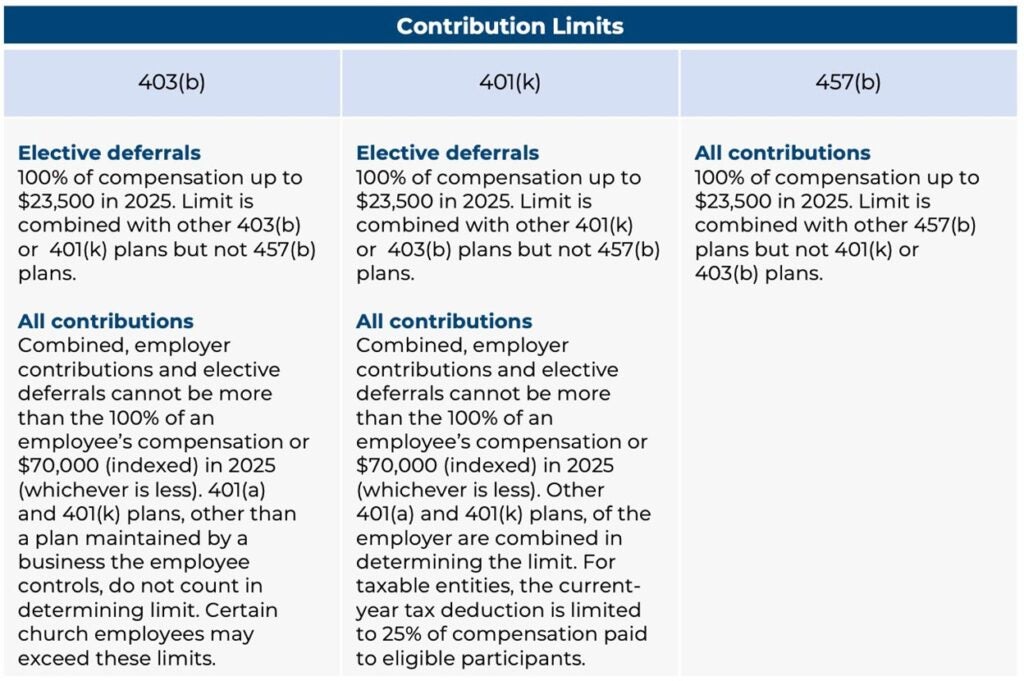

Contribution Limits

While elective deferral limits to all three plan types are $23,500 in 2025, there are some other important contribution limit distinctions. In 457(b) plans, the limit on combined elective deferral and employer contributions is the same as the elective deferral limit ($23,500). In both 401(k) and 403(b) plans, the combined elective deferral, and employer contribution limit is significantly larger—up to $70,000 in 2025, depending on compensation.

While the combined 457(b) limits are lower, the 457(b) elective deferral limit is not offset by 401(k) or 403(b) deferrals. Thus, the maximum deferral limit of $23,500 may be contributed to a 457(b) plan, regardless of whether any deferrals or employer contributions have been made to a 403(b) or 401(k) plan. For organizations offering a combination of these plans, this presents an opportunity for a participant to contribute to both.

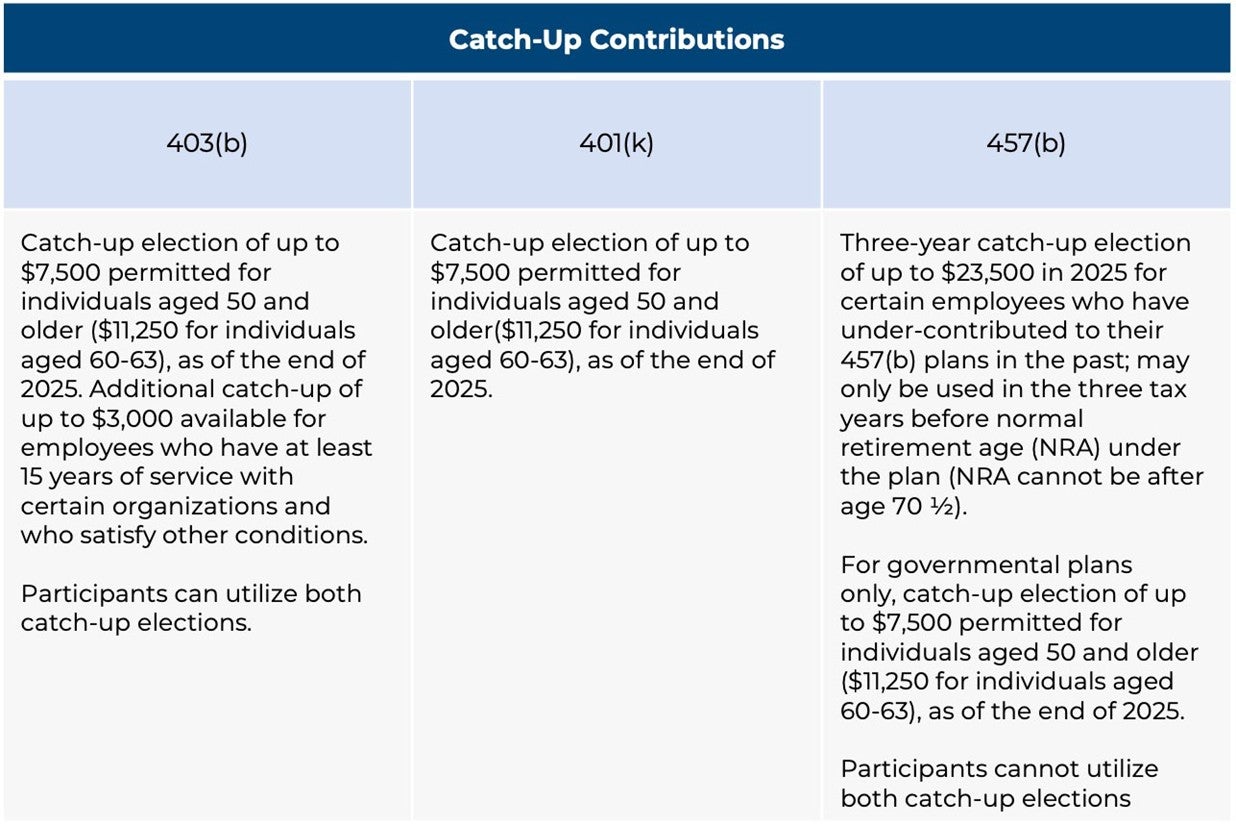

Special elections allow additional elective deferrals based on certain factors. The age 50 catch-up election, which expands the $23,500 limit in 2023 to $31,000, is available in 403(b), 401(k), and public 457(b) plans but is unavailable for 457(b) plans of private tax-exempt organizations. The same is true for the new Age 60-63 catch-up election under SECURE 2.0, which expands the $23,500 limit to $34,750.

Unique to 403(b) plans is the 15-year catch-up election, which allows a plan to permit employees who have 15 or more years of service and who satisfy additional requirements to defer up to an additional $3,000 beyond the 402(g) limit of $23,500 ($31,000 if age 50 or older, $34,750 if age 60-63) in 2025. However, this election can be complicated to calculate. The 457(b) election permits those in their final three years of employment prior to retirement to defer up to an additional $23,500 in 2025.

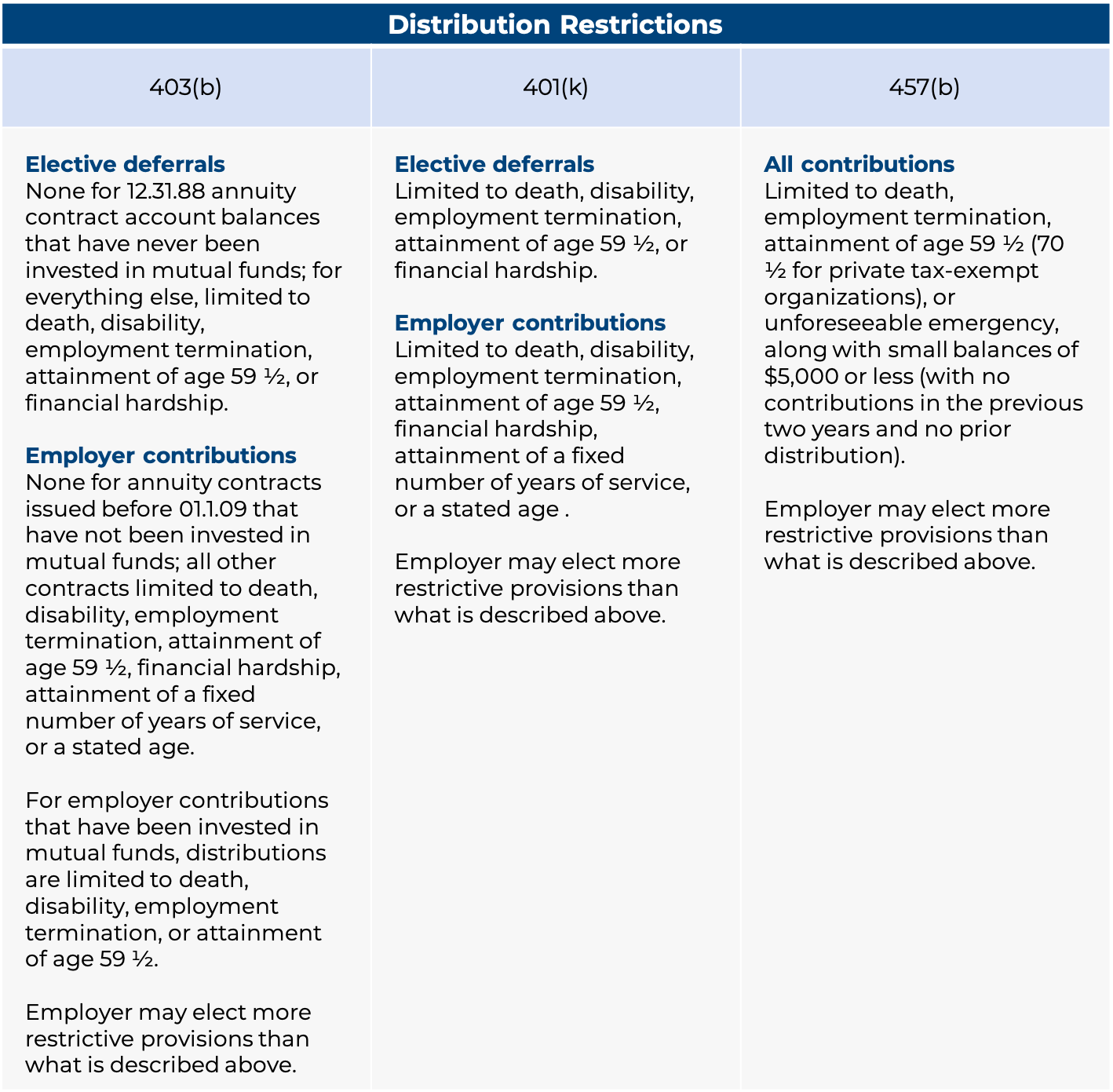

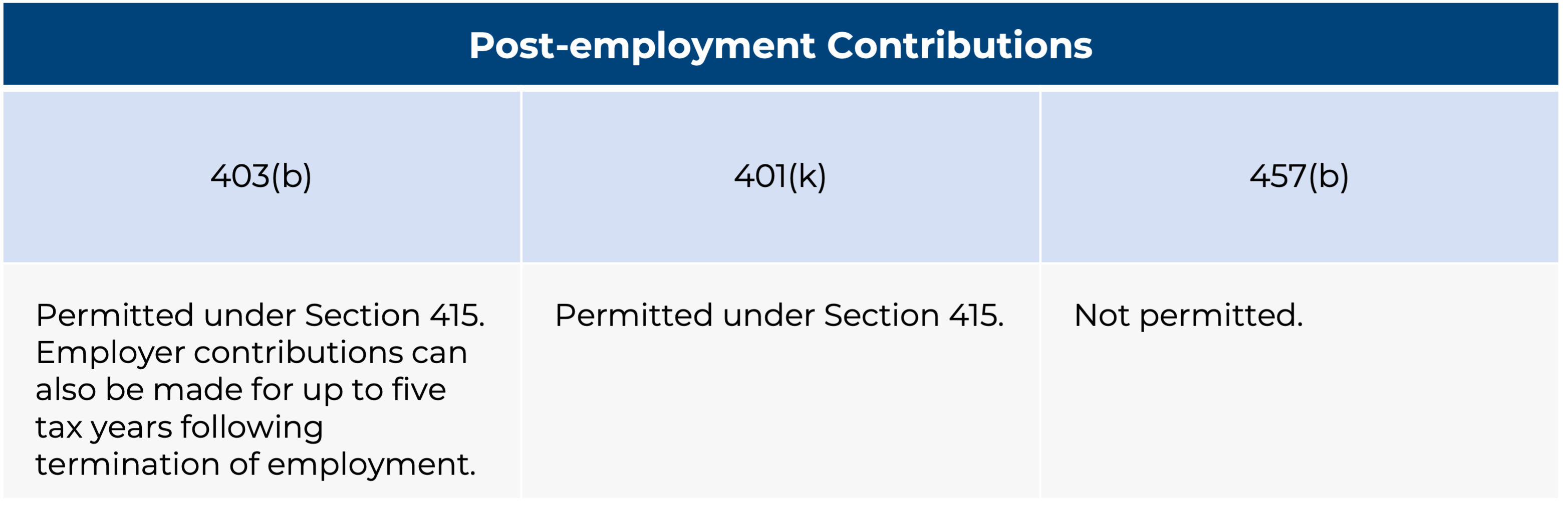

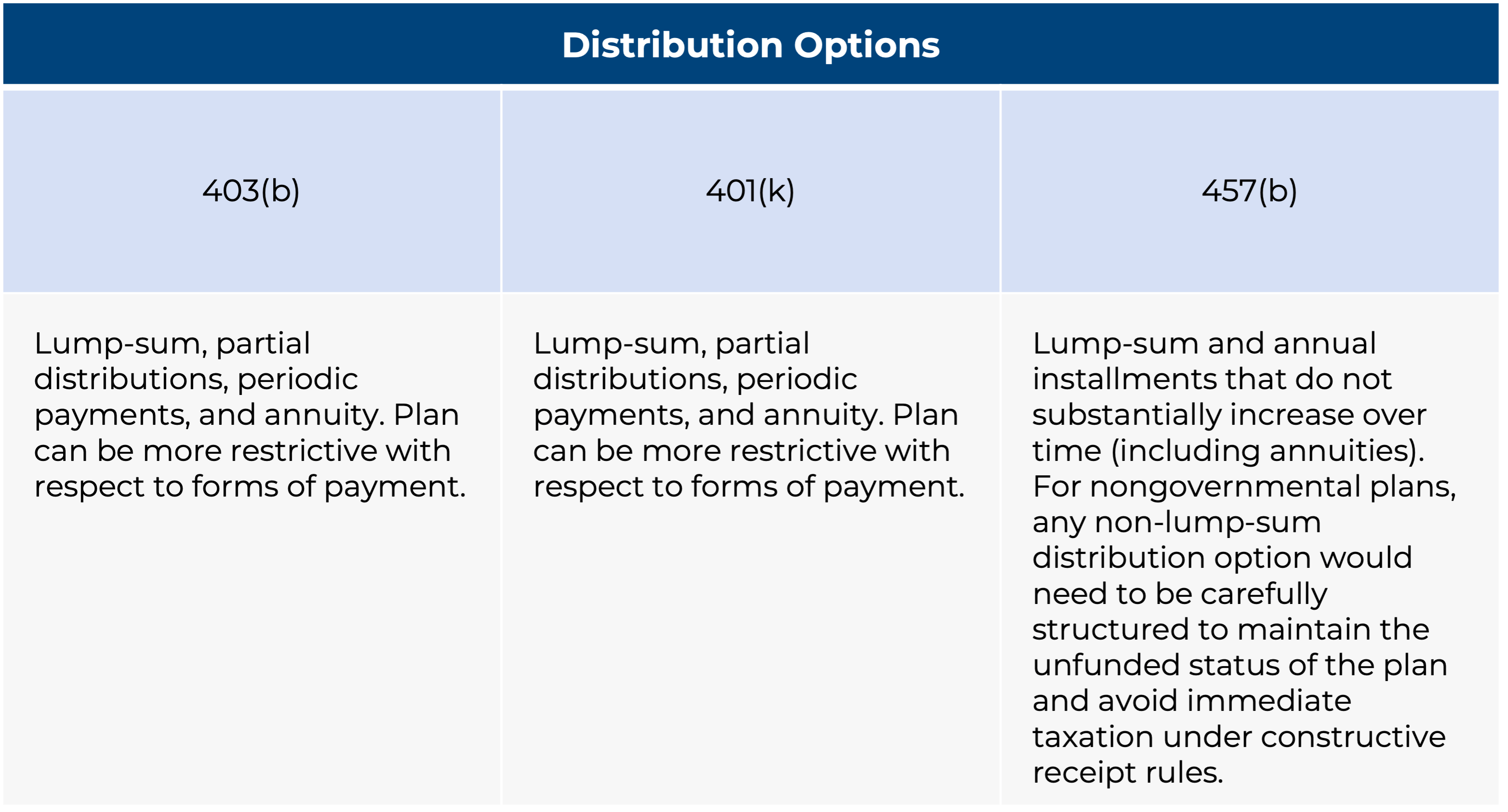

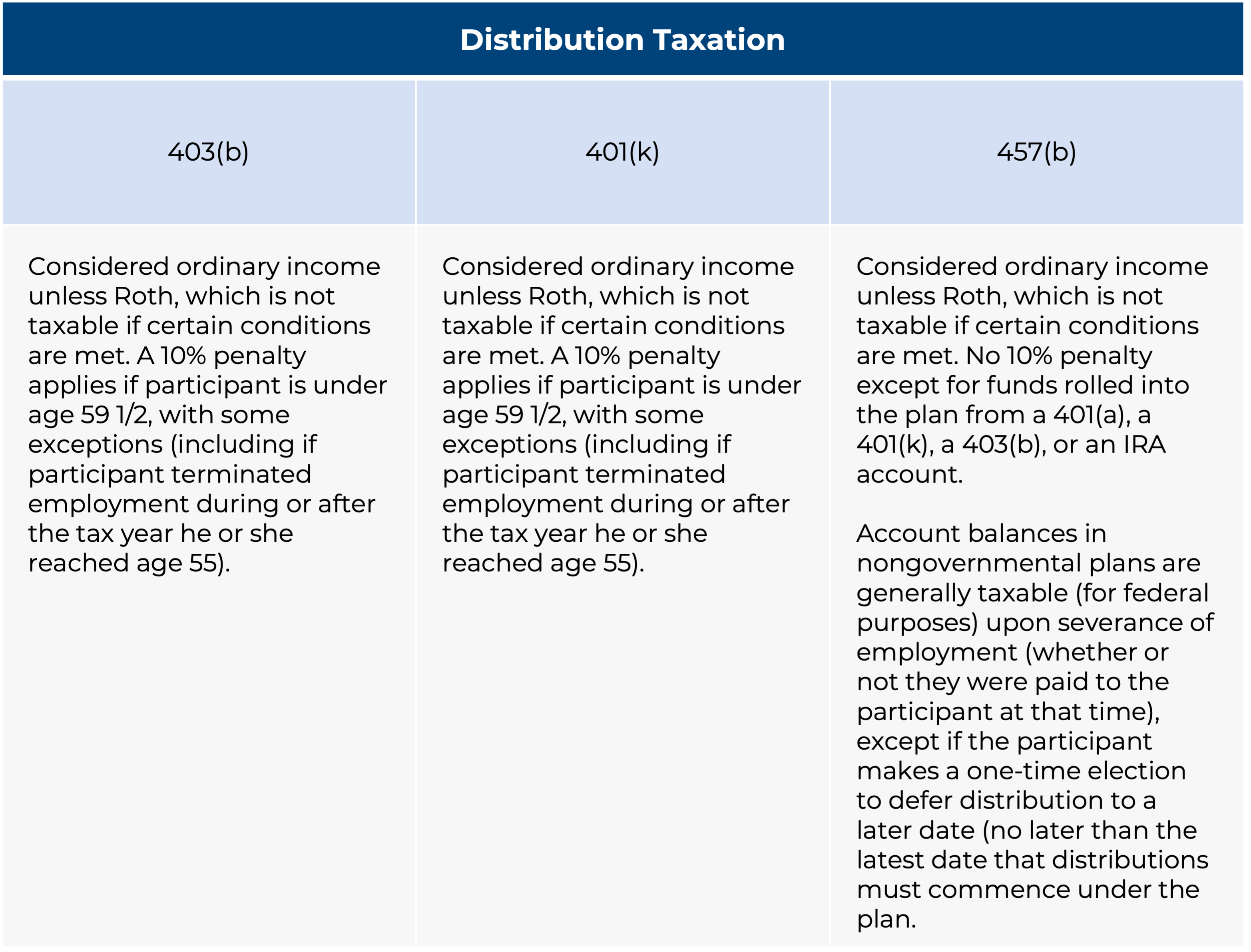

Distributions

The 403(b) and 401(k) plans generally mirror each other in terms of distribution restrictions. For example, elective deferrals may not be withdrawn in either plan type until the attainment of age 59 1/2, termination of employment, hardship, death, or disability.

However, 457(b) plans have different restrictions. Contributions may not be withdrawn until severance of employment, attainment of age 59 1/2 (70 1/2 for private tax-exempt organizations), or occurrence of an unforeseeable emergency (different rules than hardship withdrawals). For 457(b) plans at private tax-exempt organizations, there are additional restrictions as to the type of distributions that can be taken, and rollovers are not permitted. One advantage of 457(b) plans, however, is that the 10 percent excise tax for distributions prior to age 59 1/2 does not apply.

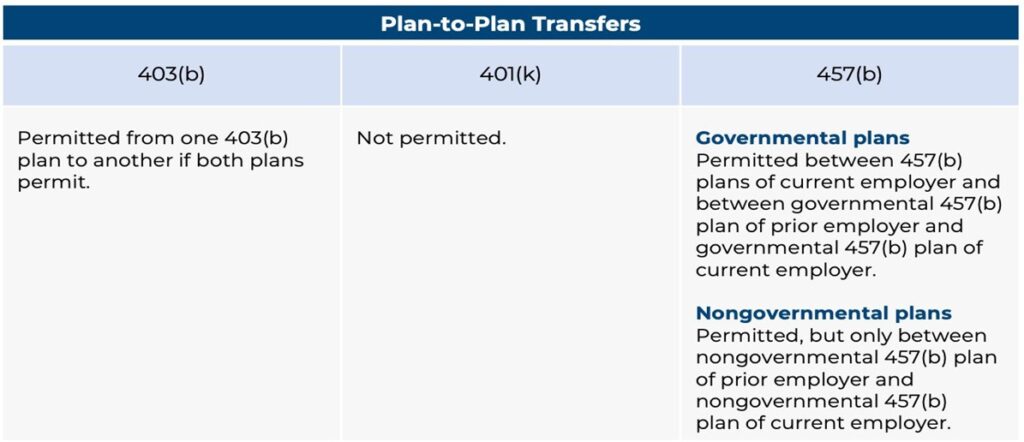

Transfers and Exchanges

In 401(k) plans, the most common reason for plan-asset movement is employer-directed transfers due to the transition to a new recordkeeper. The situation is similar for 457(b) plans; however, some participants use plan-to-plan transfer provisions for cases in which a rollover is not permitted (i.e., private tax-exempt plans).

For 403(b) plans, there is more flexibility; however, even this has been somewhat restricted by the final 403(b) regulations that became effective a few years ago. Employers may transfer plan assets from one provider to another, but these transfers are more likely to be restricted at the provider contract level than in the case of a 401(k) plan. Plan participants may transfer plan assets in the form of an exchange to any approved provider in a 403(b) plan. Plan-to-plan transfers are also permitted, though employees often opt for a rollover instead.

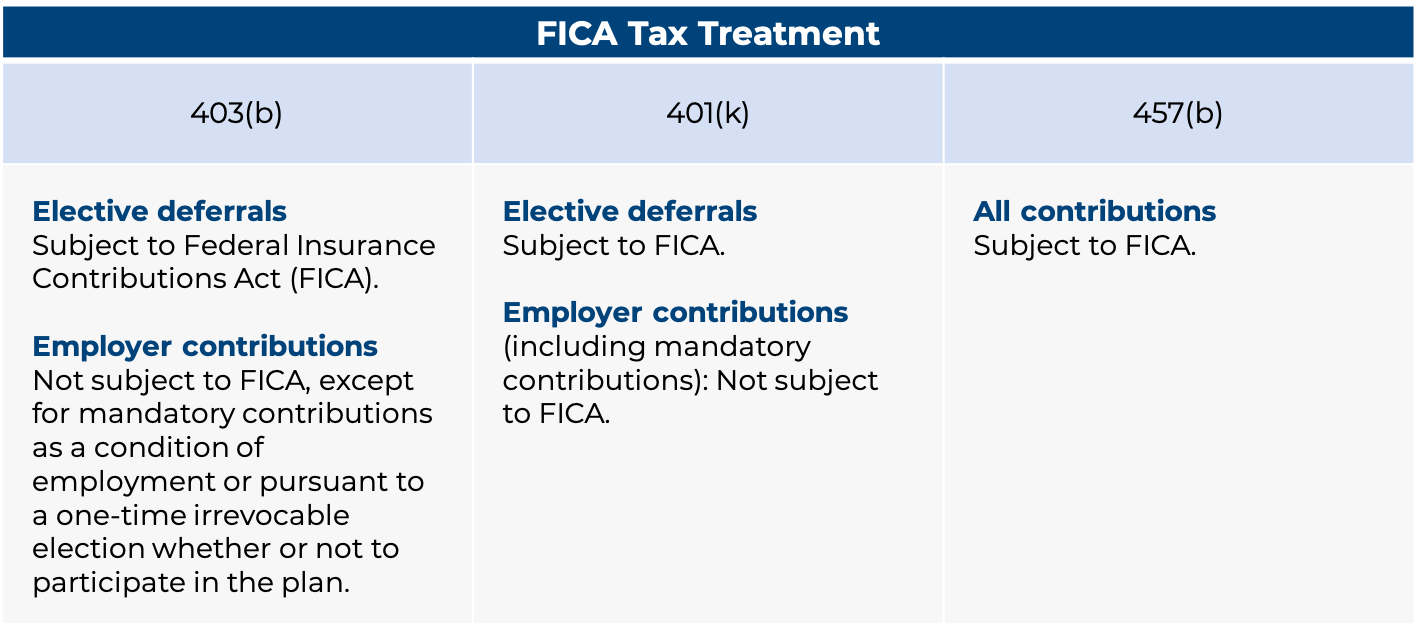

Payroll Taxes

Contributions from employers with 401(k) and 403(b) plans are generally not subject to payroll taxes, such as FICA or Medicare. Since 457(b) plans are deferred compensation plans rather than retirement plans, employer contributions are treated as compensation that is subject to payroll taxes.

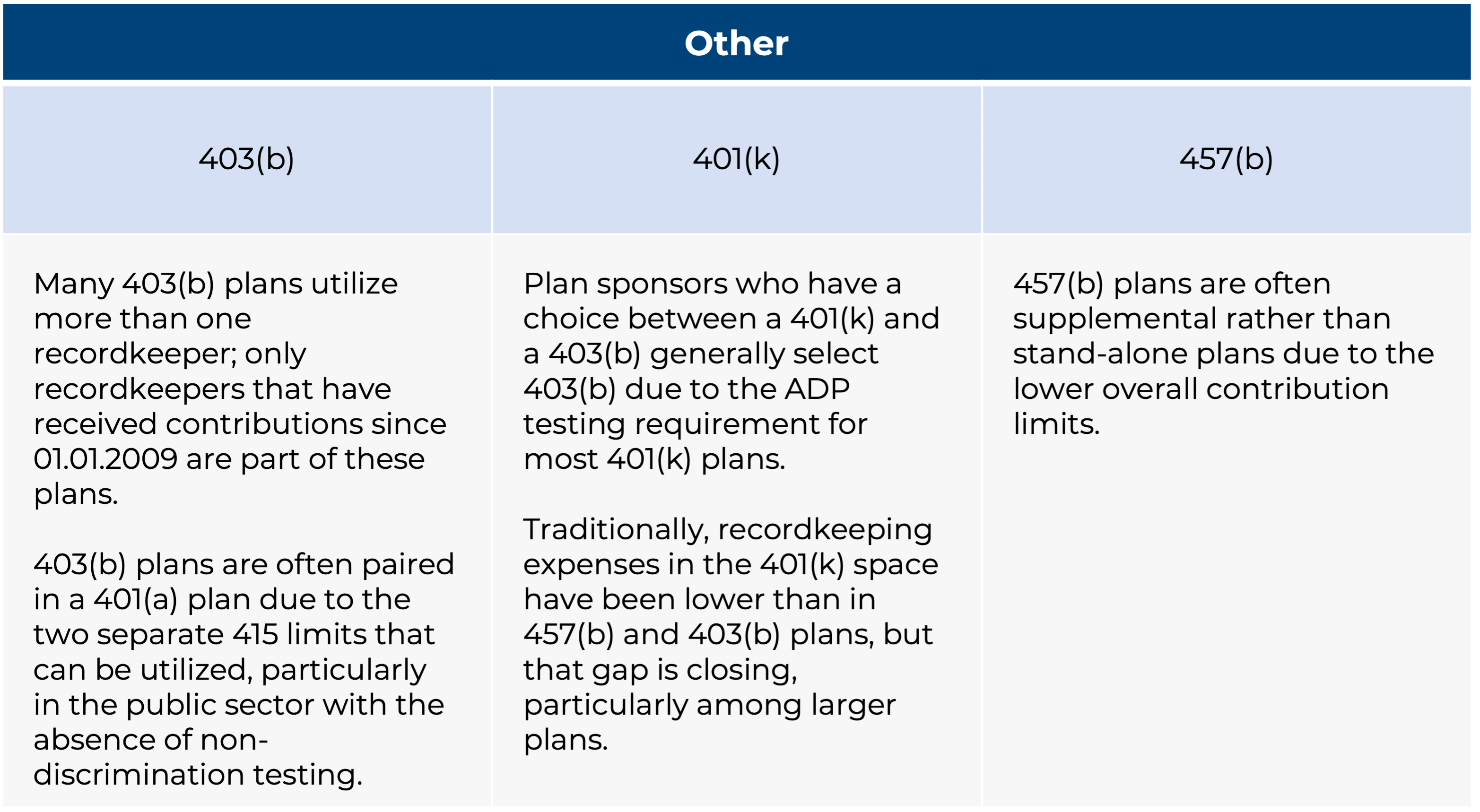

Provider Availability

A myriad of recordkeepers service 401(k) plans. Meanwhile, 403(b) and 457(b) plan assets are concentrated among a smaller selection of vendors. While this relative lack of competition can affect pricing and marketplace advancements for larger plans, 401(k), 403(b), and 457(b) product and service offerings are often comparable. While it is not uncommon for multiple recordkeepers to be offered within a 403(b) plan, it is less frequent in 457(b) plans and rare in 401(k) plans.

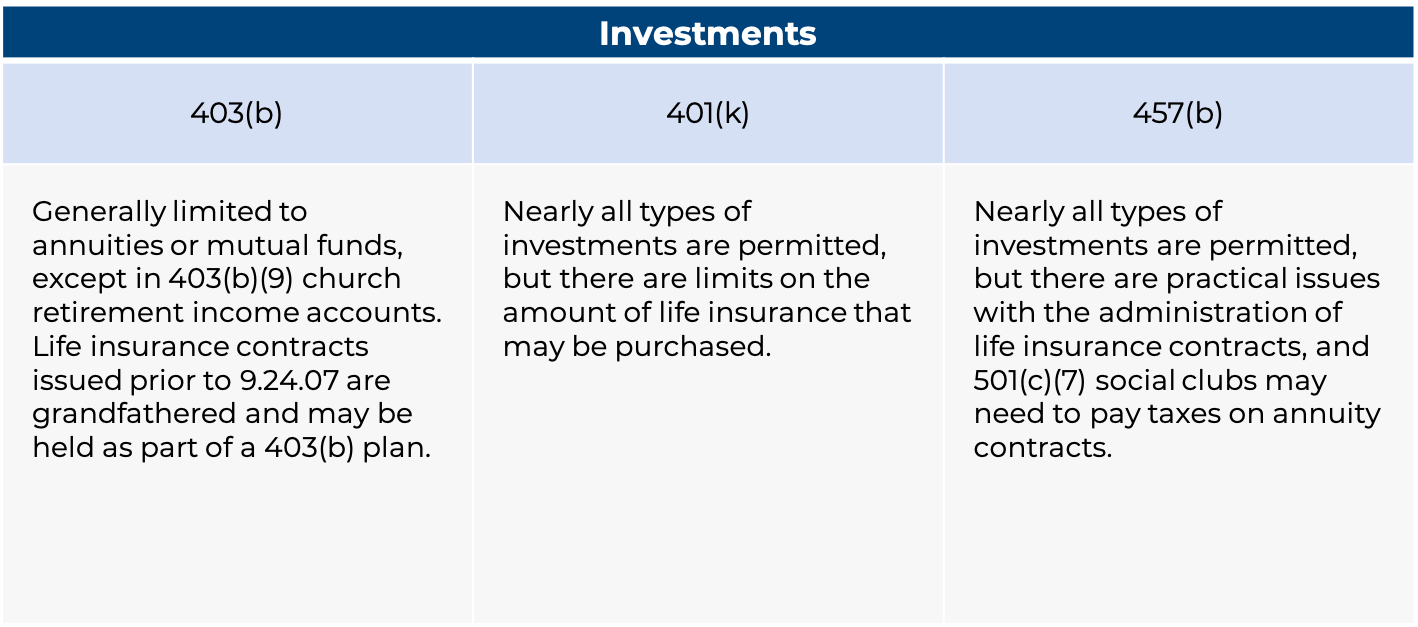

Investments

Another important distinction for 403(b) plans is their limitation in terms of the investment types that can be offered. In these plans, investment types are limited to 403(b)(1) fixed and variable annuities and 403(b)(7) custodial accounts (known more commonly as mutual funds). Investments that are permitted in 401(k) and 457(b) plans, like individual securities, are prohibited in 403(b) plans. As of this writing, there is legislation pending that would permit Collective Investment Trusts, or CITs in 403(b) plans, but that legislation has not been passed as yet. It should also be noted that some 457(b) plans are subject to investment-type restrictions by law.

Providing a competitive retirement plan benefit is often an important component of an organization’s recruitment and retention efforts. Understanding the availability, benefits, and limitations of the different plan types can help plan sponsors craft and maintain the most impactful retirement plan offering.

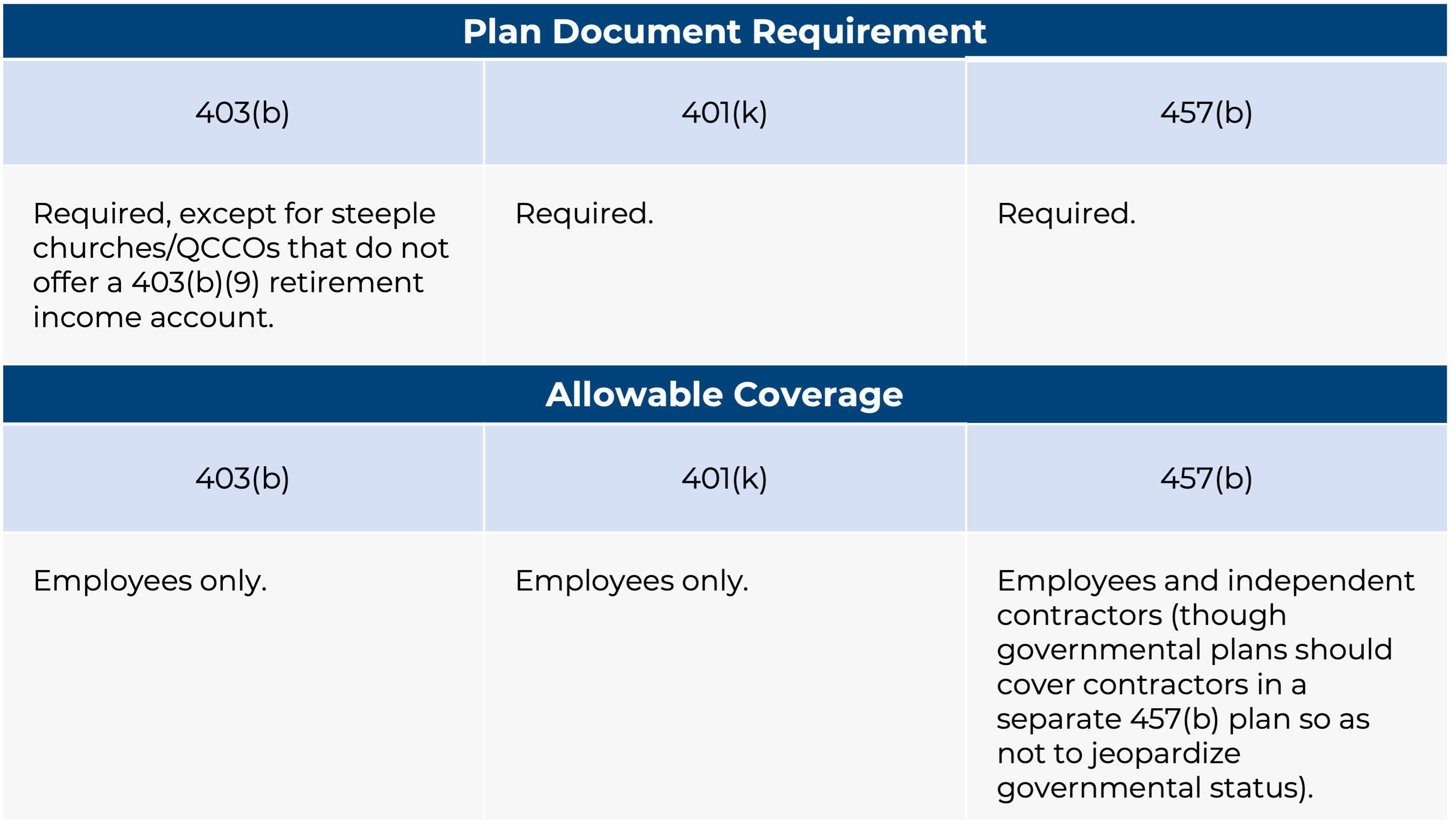

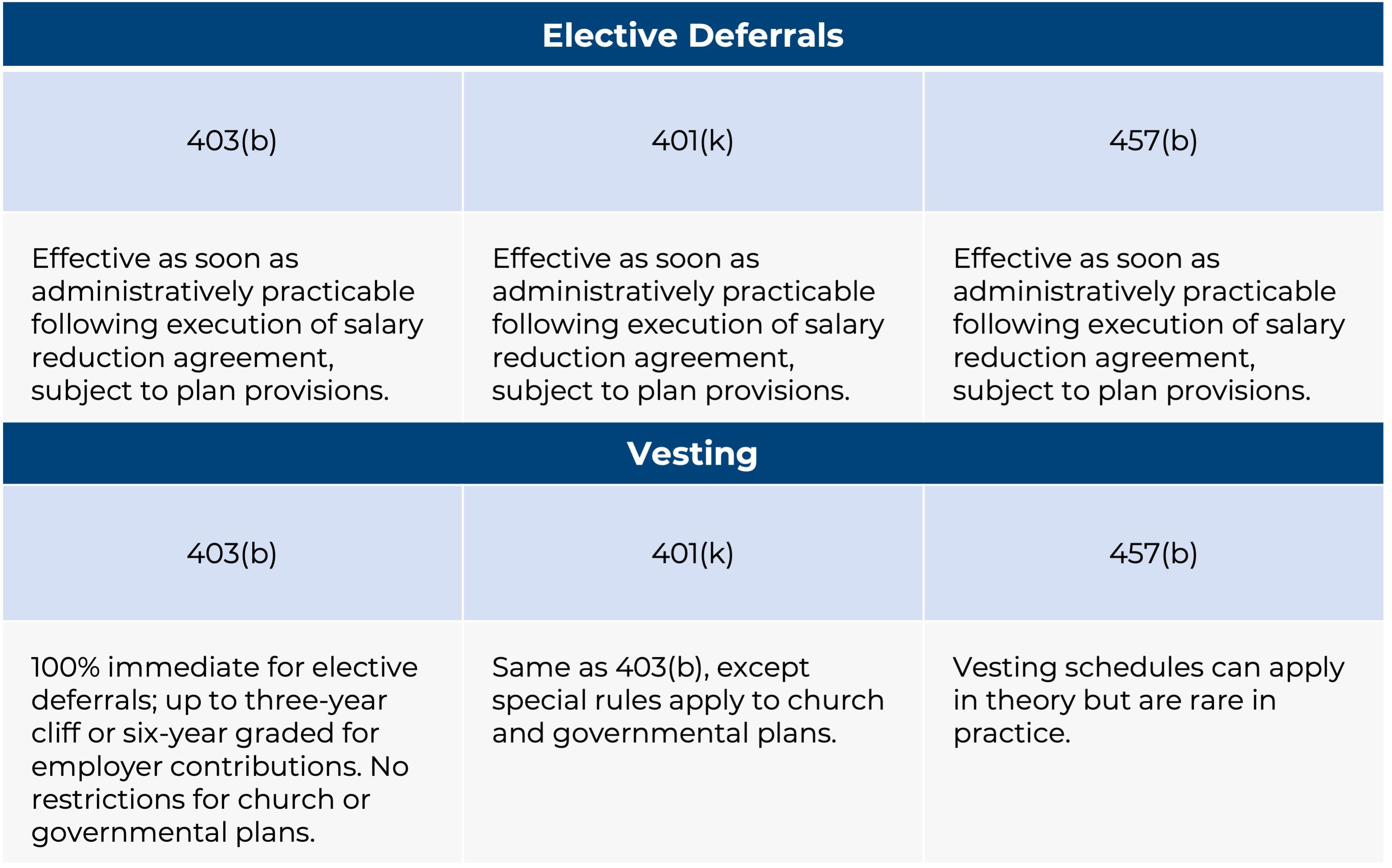

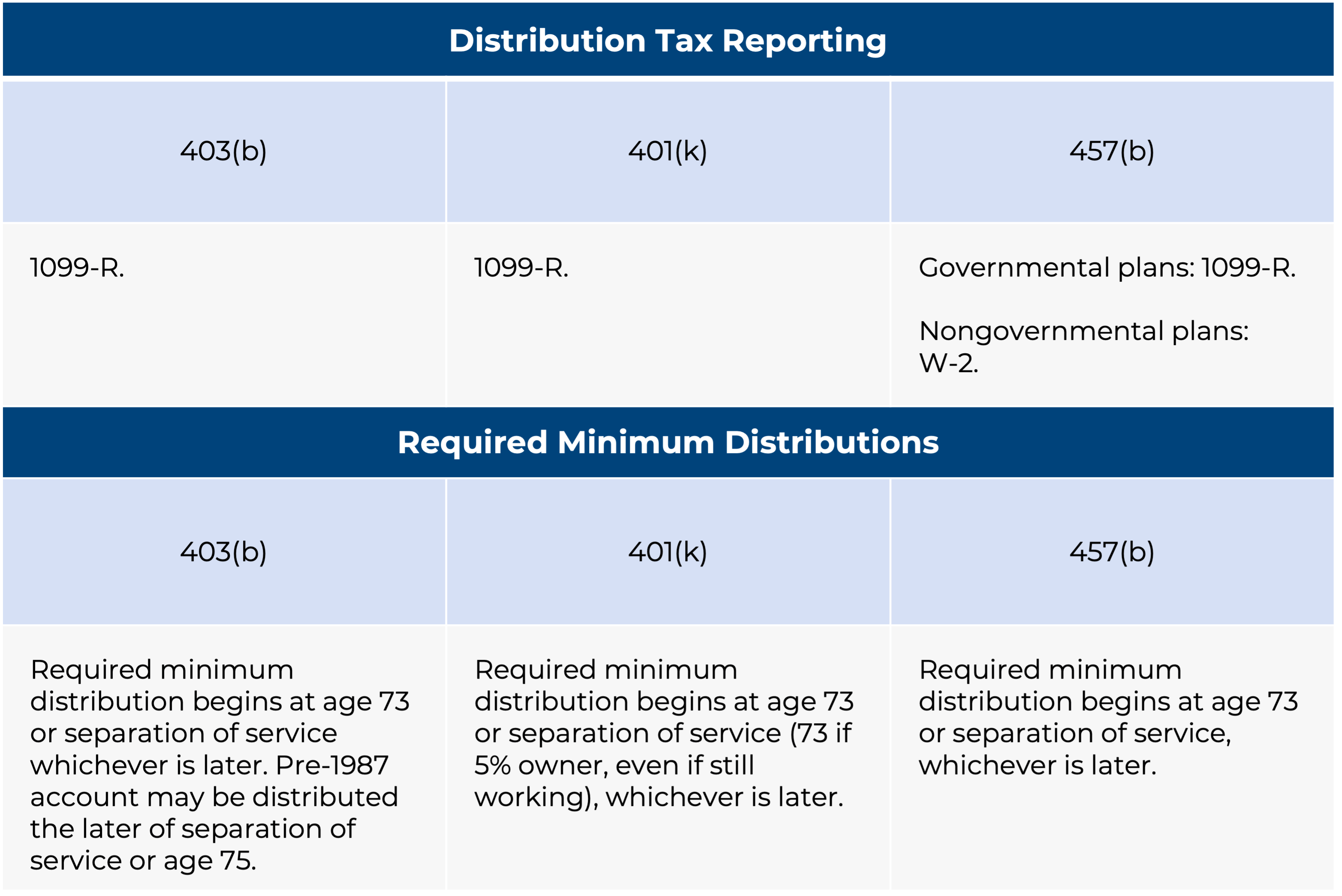

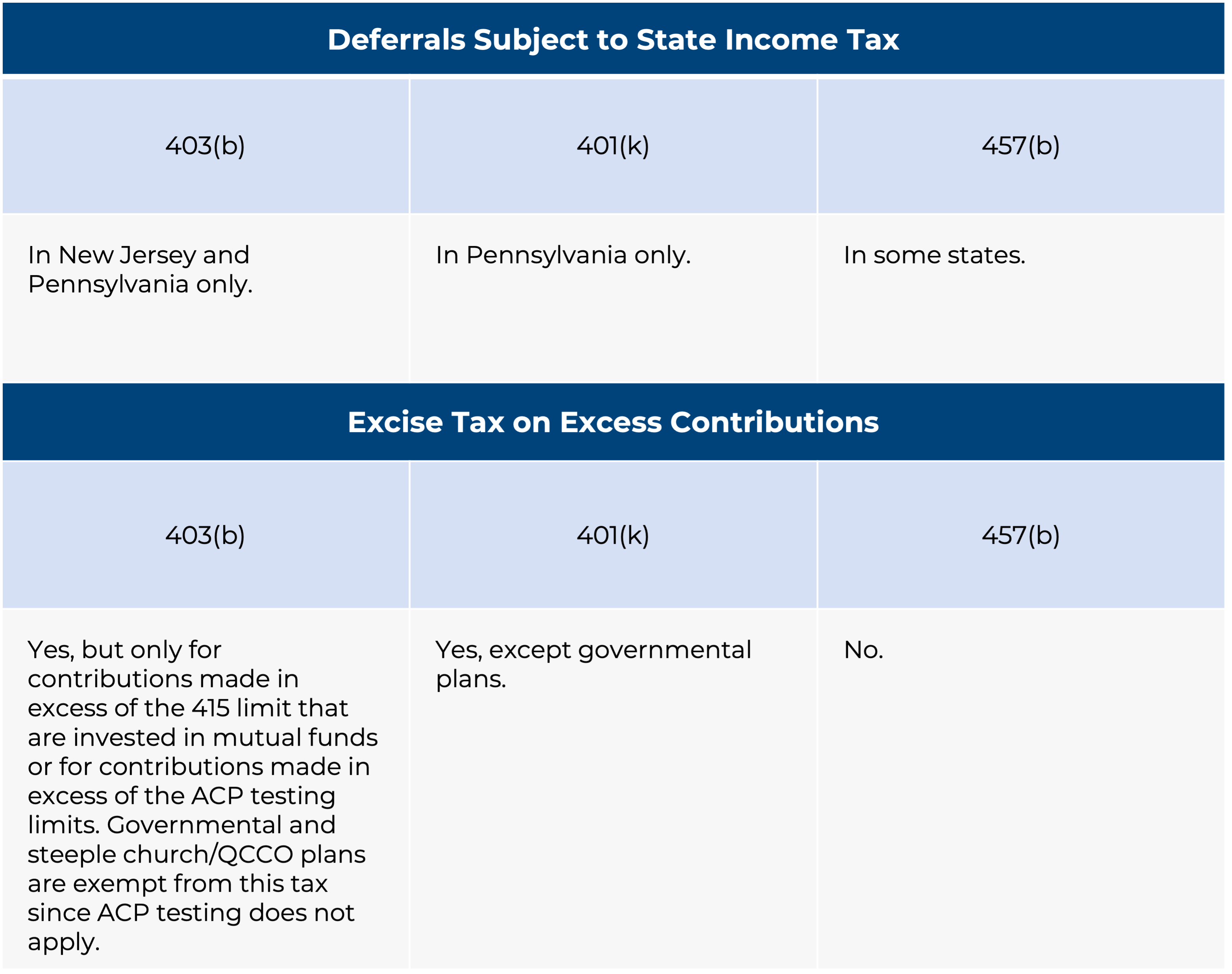

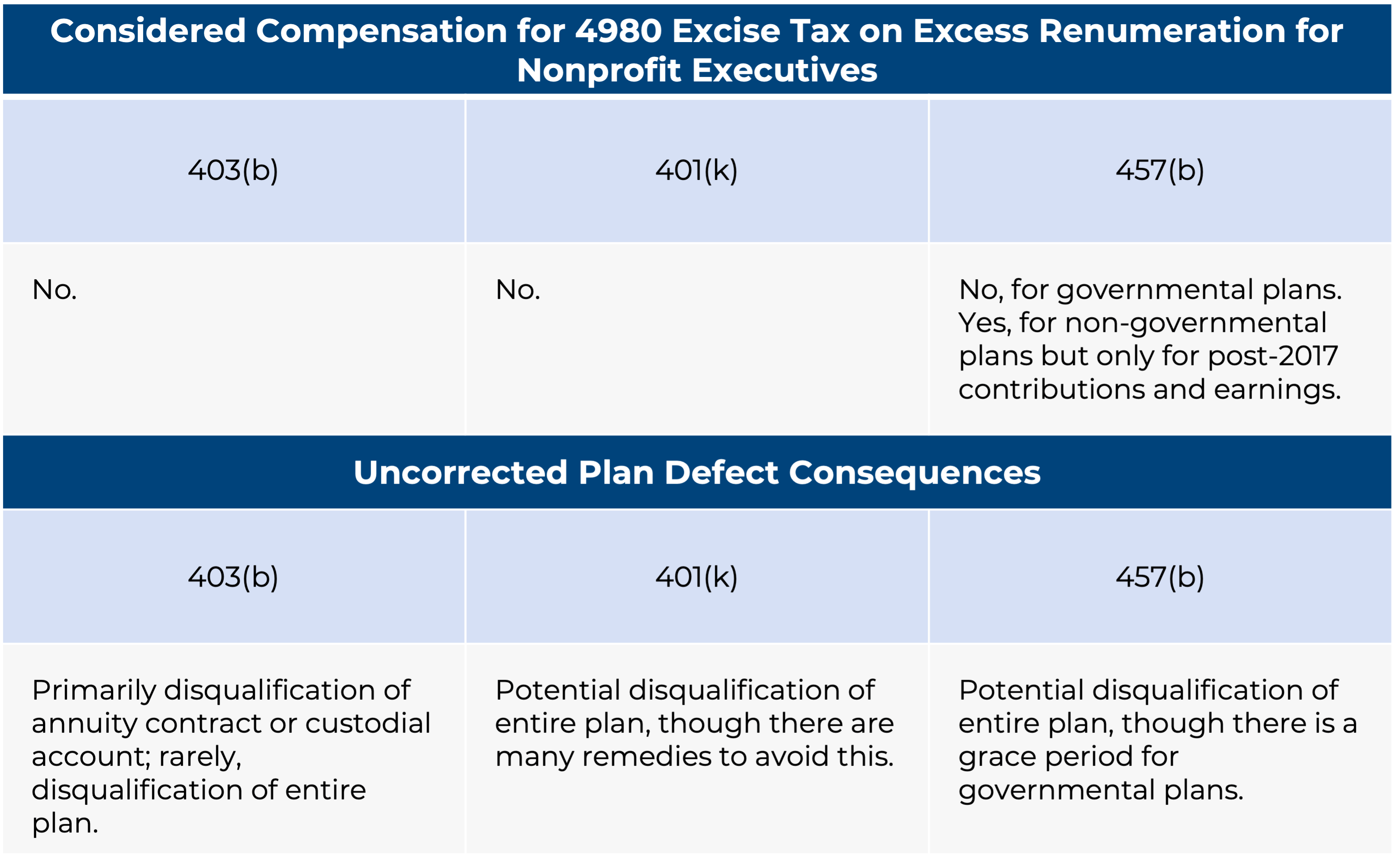

In addition to the key distinctions listed above, Figure One provides a comprehensive comparison of the remaining similarities and differences between 403(b), 401(k), and 457(b) plans.

Figure One: Digging Deeper into the Similarities and Differences of 403(b), 401(k), and 457(b) Plans

Excise Tax on Large Endowments

The law expands the existing 1.4 percent excise tax on net investment income for colleges and universities with large endowments. Now, more institutions may meet the threshold based on the size of their assets relative to student enrollment.

If you’re affiliated with a school or donor network affected by this provision, it’s worth reviewing your exposure.

Two Key Changes to Charitable Deductions

The new law enables more taxpayers to take charitable deductions. Currently, only about 10 percent of taxpayers itemize their taxes1, which means most of the remaining 90 percent receive no tax benefit for their giving. The OBBB addresses this by allowing all taxpayers to deduct a portion of their charitable giving: up to $1,000 for individuals and $2,000 for married couples.

Second, high-income donors will see tighter limits on itemized deductions, including charitable contributions. While the charitable deduction remains intact, the cap on total itemized deductions, sometimes called the Pease limitation, has been reinstated for certain earners. This change could affect giving behavior among major donors.

Private Foundation Reforms

Private foundations also face new compliance expectations, including:

- Stricter reporting requirements. While the IRS has not released all implementation details, the bill signals likely changes such as expanded disclosure of related-party transactions, more detailed grant-making reports, tighter tracking of administrative expenses, and faster or more frequent reporting cycles.

- Revised self-dealing rules. The new rules broaden the definition of self-dealing, making it easier for certain transactions, like loans, leases, or services involving insiders, to trigger penalties, even if they were previously considered permissible.

- Heightened scrutiny of donor-advised funds (DAFs). Foundations may face additional disclosure requirements.

These updates may lead to more administrative oversight and planning considerations for foundation boards and staff.

Proposed increases on excise taxes for private foundations did not make it past the Senate. These increases would have had a significant impact, especially on the largest private foundations, amounting to an estimated annual tax increase of $2.9 billion.2

Funding for the IRS and Oversight

The bill increases funding for IRS oversight of tax-exempt organizations, signaling a likely rise in audits and enforcement activity in the years ahead.

The Bottom Line

While this legislation is primarily tax-focused, it also has implications for the nonprofit sector. Now is a good time to review governance policies, assess compliance processes, and revisit planned giving strategies with your advisory team.

If you have questions or want to talk through next steps, your CAPTRUST team is here to help.

1 “Trends in Itemized Deductions Since TCJA,” USAFacts

2 “Understanding Proposed Tax Changes for U.S. Private Foundations,” United Philanthropy Forum

The information provided is for educational purposes only, and does not constitute an offer, solicitation, or recommendation to sell or an offer to buy securities, investment products, or investment advisory services. Nothing contained herein constitutes financial, legal, tax, or other advice. Consult your tax and legal professional for details on your situation.

Many Temporary Tax Cuts Are Now Permanent

Several provisions from the 2017 Tax Cuts and Jobs Act (TCJA) are here to stay.

- Federal income tax brackets will remain where they are, permanently, with annual inflation adjustments applied to the 10 percent, 12 percent, and 22 percent tax brackets.

- The standard deduction increases in 2025 to $31,500 for couples filing jointly, $23,625 for heads of household, and $15,750 for single filers, all with ongoing adjustments for inflation.

- The child tax credit rises to $2,200 from $2,000 per child starting in 2026.

- The mortgage interest deduction limitation becomes permanent and generally only permits interest deductions on mortgage debt up to $750,000 (or $375,000 for married individuals filing separately).

- The state and local tax (SALT) deduction increases from $10,000 to $40,000, adjusted for inflation of 1 percent each year through 2029. The maximum deduction begins to phase down for households with $500,000 or more in income. This will revert to $10,000 in 2030.

- The increased alternative minimum tax (AMT) exemption becomes permanent. The AMT helps to ensure high earners pay a minimum annual tax amount despite deductions and credits.

- In 2026, the estate tax exemption increases to $15 million for individuals and will be indexed for inflation on an annual basis.

- Several business-related provisions were also made permanent, including expensing for research and development, 100 percent bonus depreciation, and the 20 percent pass-through deduction under Section 199A.

Changes for Seniors, Young Families, Students, and Tip-Earners

These are changes to keep an eye on, especially if you’re a high-income filer or retiree:

- People over 65 with income under $75,000 (or $150,000 for couples) can deduct up to $6,000 from their taxable income between 2025 and 2028. This deduction phases out completely once income meets the threshold of $175,000 per individual or $250,000 for couples.

- A new Trump Savings Account allows families with children born between 2025 and 2028 to contribute up to $5,000 a year per child, with a one-time $1,000 federal match.

- Standard repayment plans or repayment assistance plans will replace the income-contingent repayment plan for student loans. The law also limits Pell Grant eligibility and loan amounts for graduate and professional students.

- Workers receiving tips, as defined by the U.S. Treasury, can deduct up to $25,000 of their tipped income from their federal income taxes in 2025 through 2028. They will still have to pay payroll taxes and any applicable state income taxes.

- Similarly, overtime pay up to $12,500 for individuals or $15,000 for married couples is eligible for a federal income tax deduction from 2025 through 2028. Both the tip- and overtime-related maximum deductions begin to phase out if you make more than $150,000 per year or $300,000 for couples.

Other Tax Changes at a Glance

- Beginning in 2026, taxpayers who don’t itemize will still be able to deduct charitable donations (up to $2,000 for couples and $1,000 for individuals). Also starting in 2026, those who itemize deductions must donate at least 0.5 percent of their adjusted gross income before charitable contributions count toward a tax deduction.

- A new individual tax credit, worth up to $1,700, will be available for donations to approved scholarship-granting organizations. Also starting in 2027, scholarships awarded to a dependent from these organizations won’t count as taxable income.

- Tax credits for electric vehicles will end for cars bought after September 30, 2025. Credits for energy-efficient home upgrades and clean energy systems will also expire for anything installed after December 31, 2025.

- From 2025 through 2028, individuals earning less than $100,000 can deduct interest payments on car loans (up to $10,000 of the financed amount) for newly purchased vehicles assembled in the U.S.

What This Could Mean for You

This legislation may reshape your tax and estate strategy. While some provisions take effect in 2026, others start immediately.

This is a great moment to revisit your financial plan. Reach out to your CAPTRUST advisor to explore what these changes could mean for you—and how you might adjust your investment portfolio, estate plan, or withdrawal strategies to navigate the new tax landscape.

The information provided is for educational purposes only, and does not constitute an offer, solicitation, or recommendation to sell or an offer to buy securities, investment products, or investment advisory services. Nothing contained herein constitutes financial, legal, tax, or other advice. Consult your tax and legal professional for details on your situation.

When it comes to safeguarding your family’s financial future and protecting your wealth, life insurance plays a pivotal role. Regularly reviewing your life insurance portfolio with an experienced advisor should be an integral part of your financial planning.

Understanding Your Life Insurance Portfolio

Life insurance is often an undermanaged insurance asset. Conducting a periodic or annual review of life insurance policies can identify weaknesses and lead to opportunities for improvement that can substantially reduce risk and potentially improve your long-term results.

Over time, policies acquired may not perform as originally expected. Couple this with life’s changing financial, family, and health circumstances, and it becomes imperative to monitor your life insurance policies and coverage needs regularly.

Key Considerations in Life Insurance Policy Reviews

- Tax Efficiency: Life insurance can have significant income and estate tax implications, both during your lifetime and after. Strategies like creating an irrevocable life insurance trust or using tax-advantaged investment options within your policy can lead to reduced tax consequences.

- Identifying Coverage Gaps: Over time, financial obligations, taxes, and other liabilities can change. Your financial advisor can conduct a thorough review of your insurance coverage to identify any gaps and recommend appropriate adjustments to help ensure you and your family are adequately protected.

- Optimizing Your Insurance Portfolio: Life insurance policies vary widely in terms of structure and features. Ask your financial advisor to help you assess whether your current policies are suitable for your needs. They can explore options to optimize your policies, such as converting term life insurance to permanent insurance or adjusting the coverage amount to align with your current financial situation and objectives. In some cases, policies can lapse before life expectancy, or there will be deadlines within the policies that must be adhered to.

- Life Insurance Investment Performance: Some life insurance policies, particularly permanent policies such as variable universal life insurance, include cash value components that can be invested. When conducting life insurance policy reviews, an advisor can assess the performance of these investments within your policies and assist with adjustments or reallocations to optimize returns and align with your risk tolerance.

- Cost Efficiency: As you age and your circumstances change, the cost-effectiveness of your policies will also be an important consideration. An advisor can help you evaluate whether you’re getting a fair value for your premiums and explore cost-efficient alternative options, if necessary.

As you develop your financial plan, many elements could be labeled as set-it-and-forget-it aspects. Life insurance is not one of them. To remain effective, it requires regular attention and adjustment. Regularly reviewing your life insurance portfolio within the context of your wealth, estate, and business preservation planning is not just a prudent practice; it’s essential.

Nonqualified deferred compensation (NQDC) plans are a key tool for attracting and retaining top-tier executives, allowing high earners to save beyond the limits of qualified retirement plans. But understanding how to maximize this benefit isn’t always clear.

Increasingly, plan sponsors are realizing that many NQDC plan participants are underinformed or simply unaware of how to take full advantage of their plans. The result? A growing need for robust financial wellness solutions that offer not only education but personal financial advice.

“It’s easy to assume that people who earn a higher income must be financially well educated or financially savvy,” says Katie Securcher, a senior manager on CAPTRUST’s nonqualified executive benefits team. “But the truth is that these folks need help—help understanding their benefits and making the best use of their plan.”

The Case for Better Education

The 2024 NFP “U.S. Executive Compensation and Benefits Trend Report” found only 29 percent of participants fully understand their NQDC benefits. That’s a problem, especially when participants are making long-term decisions with complex tax consequences.

The good news is, for the most part, employers know that communication and education need to improve. According to the 2024 Newport/PLANSPONSOR “NQDC Plan Trends Survey,” 72 percent of plan sponsors say improving communication and education is their top priority for NQDC plans. This outpaces other enhancements like digital tools (32.8 percent) or investment menu reviews (32 percent).

It’s important to remember that Section 409A, which created and governs NQDC plans, has only been around for 20 years. “We spent the last two decades rolling out these plans, making the benefit available, and trying to get people to participate,” says Securcher. “But the industry hasn’t done a great job advertising them or teaching people how they work.”

Financial Wellness as the Fix

That’s where financial wellness comes in. “The best financial wellness programs, like the best financial advisors, don’t just explain how things work,” says Securcher. “They help participants connect the dots between their income, savings, tax strategy, and long-term goals. They show people how to balance all the various pieces of their finances and view them as part of a holistic picture.”

In the past few years, financial wellness programs have become an increasingly popular employee benefit. For both employers and employees, they have been highly desirable. And they seem to work.

A recent PLANADVISER spotlight noted a 60 percent drop in extreme financial stress among employees who engaged with one financial wellness tool. These aren’t just feel-good benefits. They have a measurable impact on participant well-being and performance.

“We have an opportunity to make a real difference for participants—but that requires engagement,” says Chris Whitlow, senior director and head of CAPTRUST at Work, the firm’s financial wellness solution for employers and retirement plan sponsors. “Many participants don’t fully realize the strategic nature of nonqualified plans until they’re at a decision point, often under pressure. That’s why education and early planning are so critical.”

Three Distinct Phases of NQDC Participation

Whitlow says a more tailored approach to education starts with recognizing where someone is on their NQDC journey. “We tend to see participants fall into one of three phases—early, middle, or late,” says Whitlow. “Each phase comes with a unique set of questions and planning considerations.”

- Early-phase participants are just getting started with their NQDC plan. They may not fully understand what it is or how to make smart elections.

- Middle-phase participants are actively contributing and need more advanced planning, plus advice on how to balance deferrals with current income, manage taxes, and plan distributions.

- Late-phase participants are preparing to receive their distributions and need clarity on liquidity, tax strategy, and integrating NQDC income into their retirement income plan.

“Effective education must be tailored,” Whitlow says. “Someone just getting started needs foundational guidance. Someone preparing for distributions needs highly specific, scenario-based advice. A segmented approach makes education far more relevant—and ultimately more actionable.”

How to Deliver NQDC Education

Here are a few examples of what some plan sponsors are doing to educate participants.

- Use live sessions to spark engagement: Whether virtual or in person, regular sessions give participants the opportunity to ask questions and get clarity. “Employers sometimes have a hard time explaining the ins and outs of their nonqualified plan,” says Securcher. “But they can tap their financial advisor or plan administrator to help. Once people hear things without jargon, it usually clicks.”

- Provide support before the enrollment window: Most key decisions and elections need to be made during open enrollment or onboarding windows. “We want participants to start investigating and learning about their options before it’s decision time,” says Whitlow. “If we wait, we’ve likely missed the window to influence an appropriate outcome.”

- Pair digital tools with human help: A well-designed portal is useful, but nothing replaces a personal conversation. “Typically, the participants who really understand their plan are the ones who got personalized advice from a human,” said Securcher. “A coach, an advisor, someone who explained the ‘why.’”

- Tailor communication to senior leaders: For executives, delivery matters. Keep communication concise, context-specific, and benefit-focused. Consider incorporating tax projections or scenario modeling into conversations.

What’s In It for Plan Sponsors?

When employees maximize their NQDC plan they’ll value it more, and they’ll advocate for it. What are the benefits for plan sponsors?

- Recruitment and retention: In a tight labor market, NQDC plans can help attract and keep key talent—but only if participants see them as a clear value-add.

- Reduced liability: When participants understand how their elections work, the risk of complaints or misunderstandings goes down. “Participants—regardless of role—deserve a clear understanding of how their decisions today affect outcomes later,” says Whitlow. “That clarity helps ensure the benefit is experienced as a strategic advantage, not a surprise. It’s about setting the right expectations and building trust.”

- Increased plan utilization: More participation typically leads to better alignment between compensation strategy and retention goals. “In our experience, the companies that lean into education often see higher deferral rates and stronger engagement,” says Securcher.

- Improved financial wellness culture: Integrating NQDC education into your broader wellness strategy can help build trust and loyalty across the organization. “When employers invest in education around benefits like NQDC, it reinforces that they value their people’s long-term financial well-being,” says Whitlow. “That message builds confidence and loyalty.”

Enter Generative AI

Generative AI has the potential to revolutionize participant education by making it smarter, faster, and more personalized. AI-powered tools can offer on-demand explanations of plan provisions, simulate distribution strategies, or help participants model the tax impact of deferral decisions—all in natural language.

“AI can play a meaningful role in lowering the barrier to entry for participants who may feel hesitant or unsure,” says Whitlow. “When applied thoughtfully, it can personalize the experience, introduce a sense of empathy, and help participants ask more informed questions when they engage with their advisor.”

Instead of reading through dense plan documents, participants could one day ask detailed questions about their unique financial situation and receive a tailored, plain-English answer—instantly.

AI can’t replace good, human advice, but it can be a powerful first step. Especially for early-phase participants who are intimidated or unsure, AI can help reduce the friction of getting started. “If technology helps participants approach a conversation with greater clarity and confidence, that’s a win—for them and for their advisor,” says Whitlow. “It’s not a replacement for human advice, but it can be a powerful complement.”

Moving Forward

Whether your NQDC plan is a legacy benefit or a recent addition, now is the time to re-evaluate how well participants understand it. Do they know how to elect deferrals strategically? Are they choosing thoughtful distribution schedules? Do they understand the tax implications?

If not, the solution isn’t just plan redesign—it’s education.

“Sometimes, we hear from employers that NQDC participation is low and people don’t seem to take advantage of the benefit,” says Securcher. “Almost always, what’s happening is not a lack of interest. It’s a lack of clarity. When people get clear on what the plan can do for them—they use it.”

DISCLOSURE: The information provided is for educational purposes only, and does not constitute an offer, solicitation, or recommendation to sell or an offer to buy securities, investment products, or investment advisory services. Nothing contained herein constitutes financial, legal, tax, or other advice. Consult your tax and legal professional for details on your situation.

Investment advisory services offered by CapFinancial Partners, LLC (“CAPTRUST” or “CAPTRUST Financial Advisors”), an investment advisor registered with the SEC under The Investment Advisers Act of 1940.

Estate planning is an iterative process organizing finances and belongings. Each estate plan varies depending on your unique situation. It reflects the complexity of your financial life, building on early foundations as complexity layers. Estate planning can ensure that transfer of property aligns with your wishes during life and after death. It can also mitigate costly expenses like estate tax and probate fees. Always consult an estate planning attorney to draft documents relevant to your specific situation.

Considering your stage in life helps identify some common estate planning steps that could be helpful to consider. Regardless of your stage in life, there are essential documents applicable to all adults.

The Five Essential Estate Documents:

- Last Will and Testament: Names an executor, appoints a guardian for children, and details how you want your property distributed after death.

- Durable Power of Attorney: Appoints a designee to make legal and financial decisions for you should you become incapacitated.

- Healthcare Power of Attorney: Appoints a designee to make medical decisions on your behalf should you become incapacitated.

- Living Will: Specifies your wishes for end-of-life care, also known as an advance healthcare directive.

- HIPPA Authorization: Authorizes doctors and insurance providers to release your medical information to a designee.

Young Adult

These five essential estate documents listed above are important documents from the time a child turns 18 years old. The child is legally an adult, and the rights that parents previously had to discuss medical choices or deal with financial matters cease.

Even though a young adult may not have substantial assets, it is important to establish basic documents. A simple will granting their estate to their parents or siblings should be considered.

Another priority is establishing a Durable Power of Attorney and Healthcare Power of Attorney. Consider parents or another trusted adult for these responsibilities. In the event of an unexpected medical or personal emergency, these legal documents allow a trusted person(s) to handle the affairs of an adult unable to make decisions on her or his own.

Establishing Living Will and HIPPA Authorizations help the trusted person(s) operate within the wishes of the individual drafting the documents, empowering them to share necessary information.

Ensuring primary and contingent beneficiaries are listed on investment accounts and insurance policies also impacts the ease of asset transfer, ensuring that wealth impacts the people you want it to.

For Unmarried Partners

If you have a committed partner but aren’t legally married, it is important for couples to discuss and execute estate planning documents, since a non-married partner is not granted many of the state-law and federal benefits of a married spouse. A non-married partner will not have certain inheritance rights that a married couple would have. A will or trust is crucial to help ensure that upon one partner’s death the other receives intended assets, without family or government intervening. Without one, state laws usually prioritize your closest relatives, which could mean your partner is left out entirely.

For Married Couples

As you plan your future together with your spouse, it is critical to discuss and prepare your estate plan. When you get married, your legal and financial status changes. As you potentially begin obtaining shared income, purchasing property together and filing joint tax returns, you will also want your estate plan to reflect a married relationship. Along with the five essential estate planning documents you will want to review your beneficiaries and possibly change the ownership of assets to joint.

Parents

Establishing guardianship in the event of the death of a parent is non-negotiable for parents. Without doing so, the court may determine where children may live. That may conflict with the wishes of parents with a much more intimate understanding of their children’s needs.

Life insurance is also important, as it can provide financial support to your family in the event of an untimely death, helping to replace your income and ensure your family’s needs are met.

Beyond wills, you might consider setting up a trust to oversee your children’s inheritance if both parents die simultaneously. Trust provisions can provide detailed instructions about your intentions for when and how your children receive their inheritance.

Parenthood also opens the opportunity to leverage 529 Plans to help save for children’s education. Parents can super-fund these flexible tax advantaged accounts, meaning they can contribute the equivalent of five years’ worth of annual exclusion gifting without filing a gift tax return.

Early Retirement

Reviewing the essential estate planning documents, account beneficiaries, and any trust documents is imperative. Levels of assets, age of beneficiaries, and the time from the last draft of the document could have changed. This means that your documents may no longer reflect your wishes.

Advanced Age

If you are elderly or dealing with illness, it’s important to create or update your will and think about setting up a revocable living trust. Make sure you have a durable power of attorney and a clear healthcare directive in place to guide decisions if you become unable to speak for yourself. Communicate your wishes openly with your family and ensure they know where to find your essential documents.

Resource by the CAPTRUST wealth planning team

Standard Tax Rules for Annuities

The taxation of annuities is straightforward. Income from the annuity contract is split between two categories: return of investment (basis) and earnings. Basis is not taxed; however, earnings are taxed. Further, earnings are taxed at ordinary income tax rates, rather than capital gains tax rates.

Annuities are subject to early withdrawal penalties, similar to other retirement accounts. Distributions from non-annuitized annuities taken before age 59 ½ are subject to a 10 percent early withdrawal penalty tax, if those dollars are earnings rather than basis. However, early withdrawals from an annuity are taxed on a last-in-first-out (LIFO) basis, meaning all earnings must be exhausted before basis can be returned tax free.

An exception to LIFO taxation is the use of the exclusion ratio for annuitized payments received by annuitants. Instead of paying taxes on all earnings up front, annuitants can use the exclusion ratio to spread the taxable portion of each payment over their lifetime, based on the proportion of earnings to the annuity’s total value.

Example: How Early Withdrawals Are Taxed

John is 55 years old and owns an annuity worth $100,000 that he has not annuitized. He has paid a total of $75,000 in premiums since purchasing the contract, meaning his earnings total $25,000. John would like to withdraw $30,000 from his annuity. How will John’s withdrawal be taxed for federal income tax purposes?

Step by Step:

- John is 55 years old, which is younger than the 59 ½ years old requirement. Therefore, withdrawals will be taxed on a LIFO basis and are subject to a 10 percent early-withdrawal penalty on earnings.

- John wants to withdraw $30,000, and has $25,000 of earnings.

- Because the withdrawal is taxed LIFO, earnings come out first.

- The $25,000 is subject to the 10 percent early-withdrawal penalty, equivalent to $2,500, and taxable at John’s marginal tax rate as ordinary income.

- The remaining $5,000 will come out tax-free as a return of basis.

However, if John decides to take payments through annuitization, 75 percent of John’s annuity ($75,000/$100,000) is basis, so 75 percent of withdrawals will be returned tax free.

Gifting Annuity Contracts

When the owner of an annuity gives their contract to another individual as a gift, special income tax rules apply. The donor, the person who originally owned the contract, is considered to have surrendered the contract. Income tax is due on the difference between the value of the contract, known as the cash surrender value, and the amount invested in the contract, or the basis. Additionally, standard gift tax rules apply.

Using our example from above, if John intends to gift his entire $100,000 non-annuitized annuity (cash surrender value) with a basis of $75,000 to his daughter, Mary, the following would apply:

- John gifts his $100,000 annuity to Mary.

- John pays ordinary income tax on $25,000. This is the $100,000 cash surrender value minus the $75,000 basis.

- Because the gift exceeds the annual gift tax exclusion amount, John is required to file a gift tax return using IRS Form 709. The amount exceeding the exclusion amount counts against John’s federal estate tax (FET) exemption.

- Mary, the recipient of the annuity, has no tax liability.

Aggregation of Annuities

The tax rules for owners of multiple annuities can be nuanced. If someone has multiple annuities meeting specific criteria, they cannot simply withdraw funds from one contract; rather, all contracts are combined, or aggregated, when calculating taxes, and the IRS treats multiple annuity contracts as a single annuity contract.

These criteria are that the annuity owner must:

- Own multiple annuities

- Have purchased these annuities after 1988

- Have had the annuities issued by the same insurer

All three of these criteria must be satisfied for aggregation rules to apply. This is important, because annuities are taxed LIFO, which means earnings on the contract come out first and are subject to ordinary income tax rates.

Beneficiaries and Taxes

The tax treatment of an annuity after the owner’s death depends on whether the contract has been annuitized.

After Annuitization

When the annuitant (annuity owner) dies while receiving benefits under a term-certain annuity payment, meaning the contract specifies a fixed period for payments even if the annuitant dies, the remaining payments of the contract are made to the annuitant’s beneficiary.

In this case, the beneficiary is subject to the same tax rules as the annuitant: The portion of the payment considered return of basis is tax free and the portion considered earnings is taxable at ordinary income tax rates.

Before Annuitization

When the annuitant dies before annuitization, which is commonly referred to as the accumulation phase, there are a range of options available that impact the tax treatment of the annuity, whether the annuity’s beneficiary is the annuitant’s estate or a named beneficiary that is not the annuitant’s estate.

Annuity Proceeds

If the annuity proceeds are retained by the estate of the owner, the estate will owe ordinary income tax on any gain in the contract, and the annuity value will be included in the gross estate of the owner. The estate will be entitled to a tax deduction on the decedent’s final income tax return for the additional estate tax attributable to the annuity value on the decedent’s estate tax return, if any.

If the annuity proceeds are paid to a named beneficiary, any tax on the gain is transferred to the beneficiary. The beneficiary is entitled to a tax deduction for the additional estate tax attributable to the annuity value on the decedent’s estate tax return, if any.

Annuities can serve as useful vehicles for financial planning; however, nuance and complexity associated with them warrant professional guidance. Please contact your CAPTRUST advisor to answer questions specific to your annuity.

Source:

Publication 575 (2024), Pension and Annuity Income | Internal Revenue Service

Resource by the CAPTRUST wealth planning team

Important Disclosure

This content is provided for informational purposes only, and does not constitute an offer, solicitation, or recommendation to sell or an offer to buy securities, investment products, or investment advisory services. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Nothing contained herein constitutes financial, legal, tax, or other advice. Consult your tax and legal professional for details on your situation. Investment advisory services offered by CapFinancial Partners, LLC (“CAPTRUST” or “CAPTRUST Financial Advisors”), an investment advisor registered under The Investment Advisers Act of 1940.

Annuities were developed by life insurance companies to provide individuals with income during their retirement. However, they date back to the Roman Empire. The name is derived from the Latin word annua, meaning stipend. While annuities existed in America in some form even before the formation of the United States, the product gained widespread popularity during the Great Depression of the 1930s, when pension plans viewed insurance companies as more stable than other financial institutions.

Qualified vs. Nonqualified Annuities

Annuities can be either qualified or nonqualified.

Qualified annuities provide tax-advantaged, tax-deferred benefits similar to those offered by traditional 401(k) plans, 403(b) plans, or IRAs. As such, the contribution, withdrawal, and tax rules that apply to other tax-advantaged retirement plans also apply to qualified annuities. Earnings in a qualified annuity are tax-deferred until payments from the issuer are received. This tax deferral is one of the product’s most attractive features. Over time, investments in a qualified annuity can grow substantially larger than if the same funds were invested in a taxable investment. However, withdrawals before the age of 59 1/2 incur a 10 percent penalty on the taxable portion, and all distributions are taxed at ordinary income rates.

Nonqualified annuities differ in that contributions are not tax deductible. Taxes are paid only on earnings when they are distributed, while the return of basis remains tax free.

The Four Parties in an Annuity Contract

An annuity contract involves four parties: the issuer, the owner, the annuitant, and the beneficiary.

- Issuer: The company that writes the annuity contract, typically an insurance company.

- Owner: The individual or entity that purchases the contract from the issuer.

- Annuitant: The individual whose life determines the timing and amount of distributable benefits.

- Beneficiary: The person who receives a death benefit if the annuitant dies.

Two Distinct Phases of an Annuity

An annuity has two distinct phases: the accumulation (investment) phase and the distribution phase.

During the accumulation phase, the owner contributes money to the annuity. Choosing this option means the annuity is deferred, as opposed to an immediate annuity where distributions start immediately. Annuities can be funded with a lump sum, known as a single-premium annuity, or through periodic investments over time.

During the distribution phase, the owner receives payments as outlined in the contract. There are two options for receiving distributions:

- Lump sum withdrawal: The owner withdraws some or all the money in the contract at once.

- Guaranteed income (annuitization): The owner elects to receive a guaranteed income stream for either the annuitant’s entire lifetime or a specified period. These guarantees depend on the claims-paying ability of the issuing insurance company, making the insurer’s financial position an important consideration.

The election for distribution typically occurs several years after purchasing a deferred annuity. Additionally, payments can be structured to cover both the annuitant’s life and the lifetime of another person—a structure known as a joint and survivor annuity.

How Are Annuity Payments Determined?

The amount the owner receives for each annuity payment depends on several factors and is ultimately determined by the issuer. Key considerations include:

- Account value—How much money is in the annuity

- Credit method—Whether earnings are credited on a fixed or variable basis

- Age at annuitization—The older the annuitant at the start of distributions, the higher the payment amount

- Distribution period—The length of time over which payments will be made

When is an Annuity Appropriate?

Annuities can be excellent tools when used properly, but they are not right for everyone.

Because contributions to nonqualified annuities are not tax-deductible, it is typically advisable to fund other tax-advantaged retirement plans first. However, a nonqualified annuity can be a strong option if you have already maximized your contributions to available retirement plans. There is no limit on how much can be invested in a nonqualified annuity, and funds within the contract grow tax-deferred until distribution.

Annuities are long-term investment vehicles. Withdrawals before age 59 1/2 typically incur early withdrawal penalties, and distributions within the first few years may also be subject to surrender charges imposed by the issuer. If you are confident you will not need the funds until at least age 59 1/2, an annuity may be worth considering as part of a disciplined retirement savings strategy. If your needs are shorter term, other options may be more suitable.

Sources:

Publication 575 (2024), Pension and Annuity Income | Internal Revenue Service

Resource by the CAPTRUST wealth planning team

Important Disclosure

This content is provided for informational purposes only, and does not constitute an offer, solicitation, or recommendation to sell or an offer to buy securities, investment products, or investment advisory services. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Nothing contained herein constitutes financial, legal, tax, or other advice. Consult your tax and legal professional for details on your situation. Investment advisory services offered by CapFinancial Partners, LLC (“CAPTRUST” or “CAPTRUST Financial Advisors”), an investment advisor registered under The Investment Advisers Act of 1940.

Non-Liquid Diversification Strategies

- Private Real Assets: Investing in private real assets, such as real estate, expands your portfolio beyond your business. Real assets can offer steady income, potential tax advantages, a hedge against market volatility, and capital appreciation. A well-rounded real estate strategy should balance core, value-add, and opportunistic investments to align with your goals.

- Private Debt: Private debt offers a wide range of opportunities, including direct and enhanced lending. Direct lending means loans primarily to private-equity-backed companies, often featuring floating rates, rate floors, covenants, and first lien or unitranche structures. Enhanced lending refers to less correlated strategies, typically backed by non-corporate assets, such as asset-based lending, royalty streams, structured credit, infrastructure debt, real estate debt, and venture debt. Choosing the right mix of these options can help ensure alignment with your portfolio’s objectives.

- Private Equity: Private equity investments should reflect your risk tolerance and goals. Three options for private equity investments include buyout opportunities, venture or growth opportunities, and opportunistic strategies, which include diversification through secondaries, distressed-for-control deals, sports investing, or GP stakes.

Liquidity Events

Events such as IPOs, mergers, or acquisitions offer opportunities to liquidate holdings and diversify. Conducting thorough due diligence and scenario modeling can show how each option may impact your long-term financial plan.

Enhancing Diversification Through Tax and Charitable Strategies

Managing the tax impact of diversification is critical. Coordinating with all professional advisors will help ensure tax efficiencies are fully identified and captured. Potential strategies include:

- Spreading the sale of private shares over several years;

- Using tax-advantaged accounts; and

- Leveraging private placement life insurance.

Another option for diversification is to donate private company shares to a charitable trust or foundation. This can diversify holdings while providing tax benefits and supporting causes that are important to you.

Structures such as donor-advised funds, charitable remainder trusts, and charitable lead trusts may be appropriate. We recommend working closely with advisors who specialize in charitable planning to select the right approach.

Five Key Tenets of a Private Investment Program

- Vintage-Year Diversification: Committing a set amount annually helps mitigate risks tied to any one investment cycle.

- Strategy Diversification: Complementary strategies enhance risk-adjusted returns. Flexibility is key to capitalizing on opportunities.

- Robust Manager Due Diligence: Thorough investment, organizational, and operational due diligence is critical due to the illiquidity of private assets.

- Global Asset Allocation: Incorporate your business, real estate, and alternative investments into a unified global portfolio view.

- Long-Term Focus: Building a mature private investment program typically takes five to seven years. Patience is essential.

Remember, diversification isn’t just a financial tactic—it’s a foundation for wealth preservation and growth. By spreading investments across different asset classes, industries, and geographies, private company owners can reduce risk and unlock opportunities for long-term prosperity.

In today’s evolving markets, diversification is a powerful strategy to protect and grow your wealth, ensuring your legacy endures for generations.

Partnering with a trusted financial advisor can help tailor these strategies to your unique financial circumstances.

The information provided is for educational purposes only and does not constitute an offer, solicitation, or recommendation to sell, or an offer to buy, securities, investment products, or investment advisory services. Nothing contained herein constitutes financial, legal, tax, or other advice. Consult your tax and legal professional for details on your situation. Investing involves risk, including the risk of loss. Investment advisory services are offered by CapFinancial Partners, LLC (“CAPTRUST” or “CAPTRUST Financial Advisors”), an investment advisor registered with the SEC under The Investment Advisers Act of 1940.

A: Generally, it’s better to consolidate investments into fewer accounts and, ideally, with one advisor or investment manager.

There is a common misconception in financial management that diversification means having several investment accounts at different institutions or with multiple financial advisors. In truth, diversification refers to the variety of investments in your portfolio, not where you hold them. For instance, maintaining multiple 401(k)s with different providers is not diversification, but balancing the quantity of stocks and bonds within your 401(k) is.

Asset consolidation has four main benefits:

- Optimized planning. With investments in one place, it’s easier to see your full financial picture. This helps you make better financial planning decisions.

- User-friendly implementation. Consolidation also makes it easier to implement portfolio changes like buying and selling investments. It can also reduce account administration fees.

- Simplified recordkeeping. Working with fewer institutions means fewer monthly statements and tax documents.

- Reduced fees. Generally, the more assets you hold with one provider, the more opportunities you may have for reducing or eliminating account fees, transaction costs, and other expenses.

For cash accounts, different rules apply, and it can sometimes be a good idea to spread deposits across multiple banks to keep each account balance below $250,000. This is the maximum amount insured by the Federal Deposit Insurance Corporation (FDIC).

Before you make any moves, talk to a financial professional to discuss the best strategy. Asset consolidation will look different for each investor.