3(38) Plan Sponsor Pitfalls

Although similarly named, 3(21) investment advisors and 3(38) investment managers under the Employee Retirement Income Security Act of 1974 (ERISA) are quite different. They provide different services and levels of protection and entail different plan sponsor responsibilities.

ERISA defines a fiduciary as a person involved with plan administration, a person with control over plan assets, or a person who gives investment advice regarding plan assets. Plan sponsors often engage investment advisors to assist with their fiduciary responsibilities if they do not possess the required expertise internally.

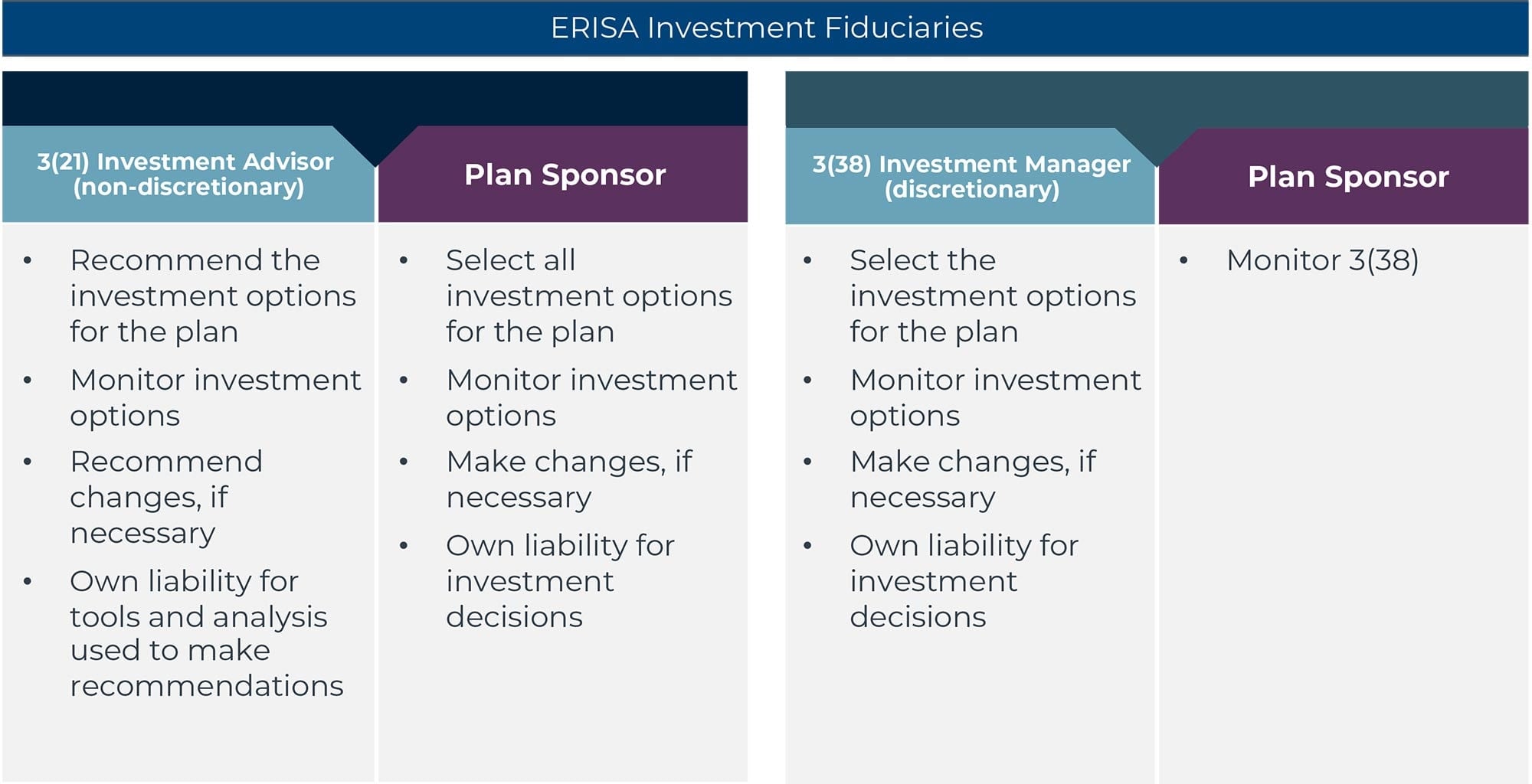

When sponsors engage investment advisors to assist with their fiduciary duties, these arrangements are referred to as 3(21) or co-fiduciary engagements. In a 3(21) relationship, the advisor is responsible for investment recommendations made to the plan sponsor, but ultimately the authority to direct assets and the fiduciary responsibility of those investment decisions falls to the plan sponsor.

Alternatively, in a 3(38) engagement, the plan sponsor delegates the decision-making authority regarding investments to the 3(38) investment manager. An appropriately structured 3(38) engagement frees the plan sponsor from the time involved in the selection and monitoring of plan investments and from the liability of those decisions. In a 3(38) arrangement, the plan sponsor’s singular investment-related fiduciary responsibility is the selection and monitoring of the 3(38) investment manager.

Sounds complicated, right? It’s not. Take a look at Figure One, which breaks down 3(21) investment advisor and 3(38) investment manager roles at a high level.

Figure One: Understanding 3(21) Investment Advisors and 3(38) Investment Managers

3(38): Simple and Effective

Many retirement plan sponsors are looking to spend less time on plan investments so they can focus on other aspects of plan management, such as providing participants with the resources they need to help them get in the plan and saving more. One way to do this is by outsourcing investment decision making to a qualified 3(38) investment manager.

But, while hiring a 3(38) investment manager is a simple and effective way to help reduce fiduciary risk, it doesn’t mean all fiduciary duties are eliminated. The process of selecting and engaging a 3(38) investment manager itself is a fiduciary responsibility and comes with some ongoing work. For example, plan sponsors are expected to monitor 3(38) investment managers as they would any other service provider.

“But the thing you monitor is not [the same as] second-guessing their decisions,” says Jenny Eller, chair of Groom Law Group’s Retirement Services Practice Group and Fiduciary Practice. “You monitor their process: Do they continue to have qualified people involved in the process? Do they continue to have the resources they need to engage in their own kind of prudent process?” You don’t get to pick a 3(38) investment manager and set it and forget it, Eller says. “You have to continue to monitor them.”

Unfortunately, it’s not unusual for things to fall through the cracks, even for the most meticulous plan sponsors. But those missteps are avoidable. From understanding what is going to be in or out of scope to making the most of the labor savings plan sponsors hope to recover—in this article, CAPTRUST leans on industry experts to expose some of the most common pitfalls when selecting or working with a 3(38) investment manager and how to avoid them.

Pitfall #1: No Ongoing Formal Monitoring Process

“The law provides a very special benefit for [plan sponsors] who hire a 3(38) investment manager,” Eller says. As long as the plan sponsor has a solid process for selecting and monitoring the 3(38) investment manager, the plan sponsor will not be liable for losses that the 3(38) investment manager causes the plan, she says. Here are a few ways plan sponsors can approach the fiduciary duty of monitoring a 3(38) investment manager’s process.

Keep tabs. “We’re starting to see lawsuits pop up where participants are saying plan sponsors were not paying attention—that a 3(38) investment manager was hired, but the plan sponsor was not asking any questions, or monitoring their process,” Jennifer Doss, senior director of CAPTRUST’s defined contribution practice, says. Maintain a record of your ongoing monitoring process. Take notes. “Because if it’s not documented somewhere, it never happened,” she says. Look for 3(38) investment managers that can provide good documentation for your files.

Ask some hard questions. Plan sponsors should periodically perform due diligence on their 3(38) investment manager. Employers and plan sponsors may want to do a regular request for information (RFI) or questionnaire. This plan sponsor due diligence is intended to verify that there haven’t been any changes to the organization that could affect its ability to fulfill its duties as 3(38) investment manager. This might include changes to its leadership team or ownership and if the firm has, or has not, been subject to a lawsuit or judgement.

Think about the questionnaire as an opportunity to get insight on the firm. Make a point to connect with your 3(38) investment manager on any changes to the investment philosophy of the firm or personnel changes of those making the 3(38) investment decisions for your plan. Experts say plan sponsors may also look to Form ADV for answers—and we’ll get into those details in just a bit. First, let’s talk about the plan sponsors role when contracting with a 3(38) investment manager.

Pitfall #2: Contracting with a 3(38) Investment Manager but Acting in a 3(21) Investment Advisor Capacity

When a plan sponsor engages a 3(38) investment manager, they give up control of the plan’s investment decision-making process. In a defined contribution plan, this means the 3(38) investment manager has full discretion to select, monitor, remove, and replace investment options offered to plan participants. But it’s important that plan committees who utilize a 3(38) investment manager maximize that benefit, Eller says.

Make the most of it. Get the labor savings you intended to get. A 3(38) investment manager is legally required to act in its clients’ best interests when it comes to choosing funds and managing assets. So go do other things! Having someone else manage plan investments allows plan sponsors time to focus on participant engagement, plan design, optimization of other plan vendors—like employee education and financial wellness providers—and overall participant satisfaction or retirement readiness. Don’t squander it.

Don’t forfeit fiduciary protection. Plan sponsor influence over investment decisions comes with potential liability when dealing with ERISA investment management and oversight. “If you hire a 3(38) [investment manager] and then push them out of the way and make the decisions anyway, you have lost all benefits of appointing [the 3(38) investment manager],” Eller says. For example, if the 3(38) investment manager allows the plan sponsor to remain heavily involved in the investment decisions for the plan—whether that is suggesting or influencing the funds in the plan lineup—there is a risk that the plan sponsor loses the fiduciary protection that hiring the 3(38) investment manager is meant to provide.

“It can be difficult for some plan sponsors to pass the reins,” Doss says. Some want to retain the ultimate decision about which funds should be offered, which isn’t possible in a true 3(38) relationship.

Pitfall #3: Allowing Room for Guesswork or Interpretation

The details of a 3(38) investment manager relationship are not something to leave to chance, so do your homework.

Ask about any potential conflicts of interest. One best practice is to make sure your 3(38) investment manager discloses all sources of revenue related to the relationship, says Martha Tejera, founder of Tejera & Associates, a consulting firm helping employers meet their fiduciary responsibility in the selection of their retirement plan providers and advisors.

Integrity is also important, Tejera says. “An issue I just recently came across is fund managers paying for [or] providing training for registered investment advisors.” Providing completely clear, client‑focused advice to clients is paramount for 3(38) investment managers, Tejera says. For example, find out if the 3(38) investment manager receives gifts of any kind from the vendors and companies they do business with. This includes pay-to-play arrangements, sponsorships of company events, lunches and dinners, or trips from vendors the 3(38) investment manager does business with.

Obtain and investigate disclosure of any litigation. Tejera says one of the most important documents to check is Form ADV. This free disclosure document reveals everything from an advisor’s fee structure and firm history to its management style and any misconduct. You can get a copy of Form ADV through the 3(38) investment manager’s website or on the Investment Adviser Public Disclosure website at adviserinfo.sec.gov. You can also check state regulator websites where the advisor operates.

Get the details in writing. If you are engaging a 3(38) investment manager, they must acknowledge their fiduciary status in writing to you. A written contract between a plan sponsor and a 3(38) investment manager with a defined set of services is a way to ensure the agreed-to terms of the relationship are upheld and that the right parties are receiving proper fiduciary protection. Written documents can also serve as legal evidence in court, if necessary.

Pitfall #4: Assuming All 3(38) Investment Manager Services Are Equal

3(38) investment manager services can vary widely from one service provider to another, and it’s the plan sponsor’s responsibility to get into the weeds to understand what is in scope and what is not in scope, Doss says.

Get specific. “If plan sponsors just assume, ‘I’m asking for 3(38) investment manager services and I’m going to get the same package with different 3(38) investment managers,’ they’re wrong,” Doss says. Plan sponsors should review the definitions of actual services offered and “Get the details in writing about what the 3(38) investment manager is going to take discretion over and what functions remain a plan sponsor responsibility,” she says.

Drill into the details with the provider: Find out how they are going to make the most out of your time as a plan sponsor. For example, does the 3(38) investment manager tailor investment recommendations to fit each plan, or does the plan have to transition to a defined menu of investments? If the 3(38) investment manager offers custom or proprietary funds, will they be included in the lineup?

Most 3(38) investment managers will assume full responsibility for selecting and monitoring plan investments, including your qualified default investment alternative (QDIA). Find out if this work will be in scope. Which party will define asset classes used for the plan’s investment menu? Which party will define what type of share classes or investment vehicles are used? Moreover, does the plan have self-directed brokerage accounts or company stock, and how will those be handled? Think about all the individual components of your plan. You’ll want to know what is in scope and what is out of scope.

Look at potential changes. While some 3(38) investment managers take discretion over current plan lineups, others will opt for a complete revamp of the plan’s current fund menu, Doss says. Keep in mind that any changes made to the plan will need to be communicated to plan participants, so consider the time, effort, coordination, printing, and postage costs involved with that.

“Implementation could mean a complete lineup overhaul—or it could mean absolutely nothing, but it’s important to understand exactly how much change is required and what will need to be managed by the plan sponsor,” Doss says.

Plan sponsors can take simple steps that can lead to a happy and healthy retirement savings plan if they avoid the common pitfalls described above. A well-structured 3(38) investment manager agreement can facilitate fiduciary risk transfer and create labor savings that will allow employers to focus on more meaningful things for their participants. While it requires some homework up front and a little management along the way, the payoff in hiring a 3(38) investment manager can definitely be worth it.