Auto Alone Falls Short

We have all heard the Chinese proverb: Give a man a fish and you feed him for a day; teach a man to fish and you feed him for a lifetime. What if plan sponsors thought of retirement planning for their employees along the same lines?

Don’t get me wrong. The powerhouse trio that makes up the retirement auto-revolution—automatic enrollment, automatic escalation, and the widespread use of target date funds in the qualified default investment alternative (QDIA) slot—has had a positive impact on savings behavior, investment diversification, and potential participant outcomes. But even after the auto-retirement boom, the main concerns affecting defined contribution retirement plans remain largely the same.

In fact, plan sponsors may be lulling their participants into a false sense of security.

“Automated features only go so far if the plan falls short on adequately engaging participants with advice and education,” says Jennifer Doss, director of CAPTRUST’s Institutional Solutions Group. “The next step really does need to be reaching out to them one-on-one, educating them about what they have today, finding out what their goals and objectives are going forward, advising them on the right way to get there, and enacting change as needed.”

A Double-Edged Sword

While substantial progress has been made to help plan participants accumulate retirement savings, challenges remain. Participant inertia, which can work both in favor of and against participants and plan sponsors, continues to dominate as a top headwind for the retirement industry.

It was the 2006 passage of the Pension Protection Act (PPA) that spawned the auto-revolution. And just like that, the majority of defined contribution plan sponsors abandoned their 30-year ongoing battle against human inertia, choosing instead to embrace the powerful bias through the rapid expansion of auto-everything. The employees of these companies were suddenly able to start saving for retirement by simply doing nothing.

As they say, you have to take the good with the bad, and in this case, the downside of automatic features is participants commonly (and mistakenly) assuming their automatic retirement plan is good-to-go, as is, and doesn’t need anything else—no rebalancing, no asset-allocation review, no additional savings increases. The cruise control framework so helpful in overcoming inertia may actually be giving participants a false sense of security and, ironically leading them to pay less attention to their retirement accounts over time. Data bear this out.

According to Vanguard’s “How America Saves,” 92 percent of defined contribution plan participants did not initiate any exchanges within their accounts during 2017, and more than a third of participants surveyed in the report had zero contact with Vanguard during the year. This data tells us that participants are staying the course with their investment strategies—a good thing—but they are also not increasing their deferral rates or actively engaging in their plans—a concerning thing.

“What you see is that participants assume they’re saving and investing like they are supposed to, probably because their enrollment in the plan and their investment selections have been done for them. The setting of a savings rate and selection of an investment option by the plan sponsor creates this interesting endorsement effect with participants. Plan sponsors need to be aware that this perceived endorsement may actually serve to incent even more inertia,” says CAPTRUST’s Defined Contribution Practice Leader Scott Matheson.

Design to Win

“Too many plan sponsors are automatically enrolling employees at rates likely to result in inadequate retirement savings for many workers,” says Matheson.

Based on CAPTRUST independent research, just over half of all defined contribution retirement plans offer automatic enrollment—with 64 percent of those plans also offering the automatic escalation feature.

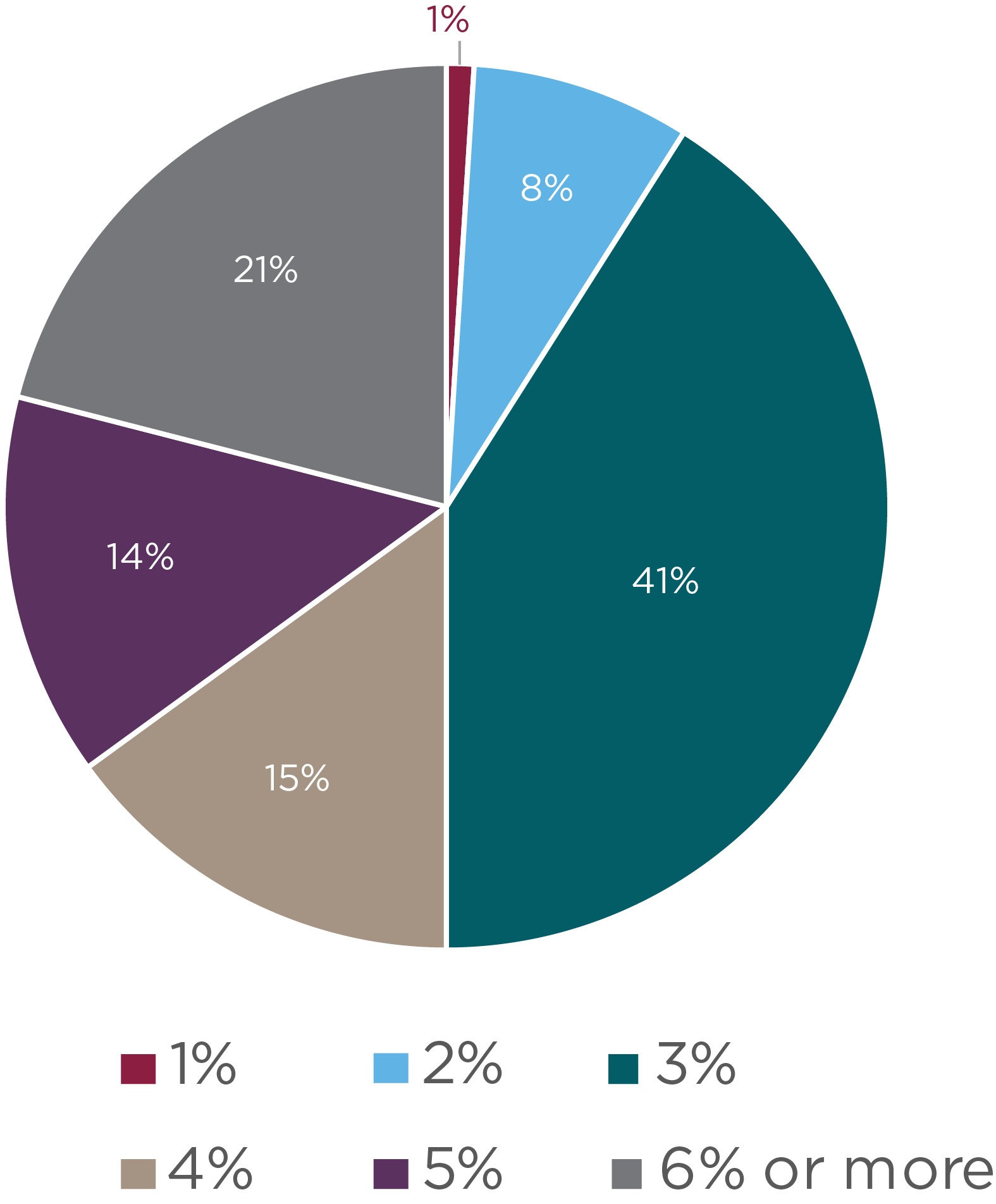

While experts recommend saving 10 to 15 percent of compensation, more than three-fourths of automatically enrolled participants are defaulted at a rate of 5 percent or less, as evidenced below, in Figure One. On average, that means three-fourths of participants in this population are not even saving at a rate of half the amount likely needed to allow them to replace their income in retirement. Further, half of participants surveyed were defaulted at 3 percent or less and only 1 in 5 participants reported a deferral rate of 10 percent or higher.[1]

Figure One: Default Automatic Enrollment Deferral Rates in 2017

“Most people see the initial contribution rate set by their employers as an endorsement of the right savings rate, such that it must be the appropriate amount to save for retirement. So why not harness human inertia and this perception of endorsement for yet another win and start people off at a rate that will more likely result in adequate savings for American workers?” says Matheson.

Studies show that plan sponsors fear upping their default contribution rates from the typical 3 percent because of concerns that it would negatively affect participation. However, the facts tell us this is not necessarily true.

Research from AARP concluded that higher default rates don’t dissuade participants. In fact, a company studied by AARP automatically enrolled participants at two different rates: 3 percent and 6 percent. The group offered the higher default rate had nearly the same level of plan participation—only a 5 percent difference.[2]

According to the same AARP research, a company surveyed with a 12 percent default contribution rate found that automatically enrolled participants stayed at this rate even though, in some cases, it resulted in savings that were higher than needed! In addition to illustrating the inelasticity of participant engagement to increases in the default savings rate, this type of behavior certainly validates the endorsement effect referred to by Matheson.

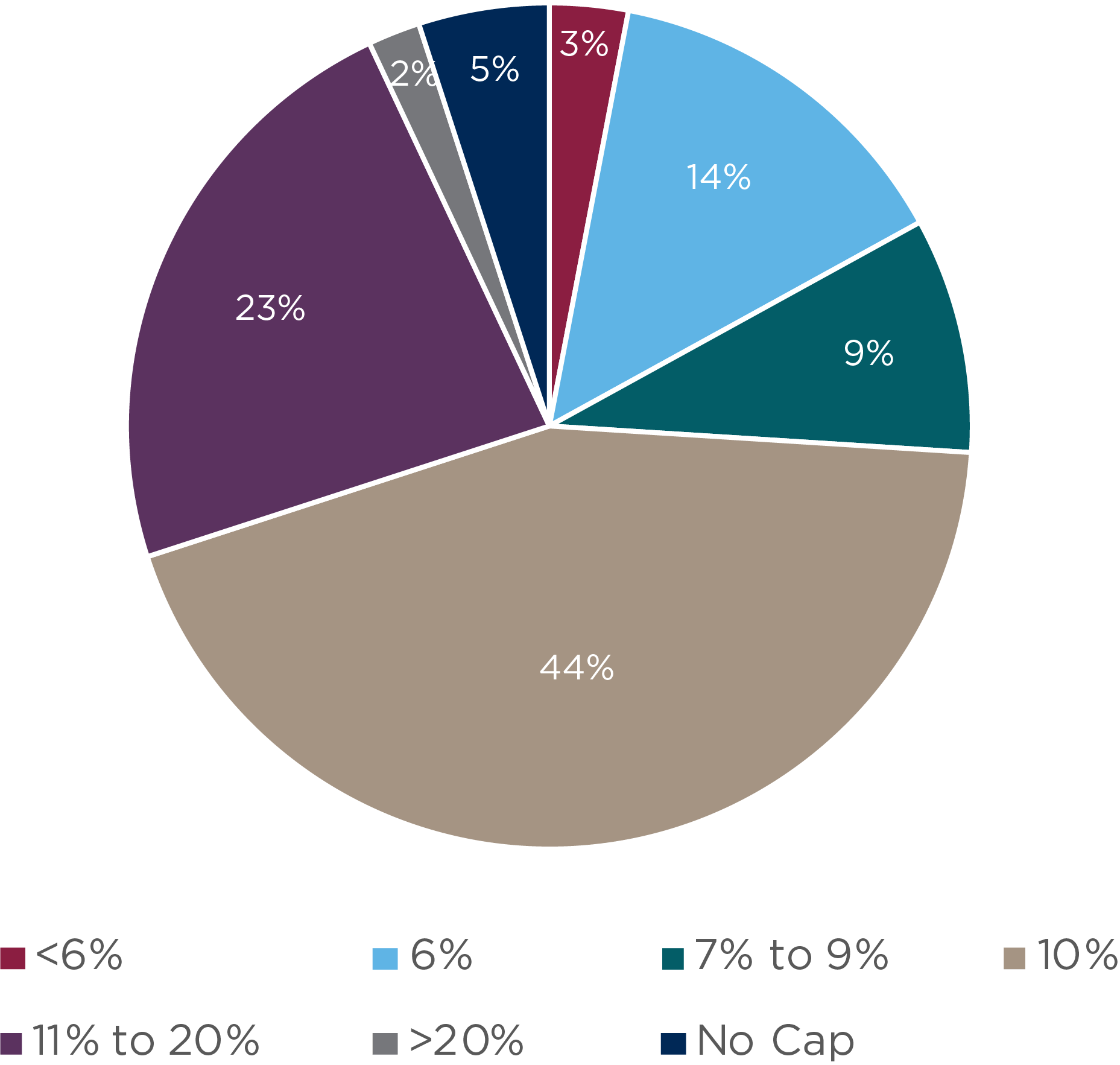

Figure Two provides a summary of default automatic escalation caps. The default escalation cap for defined contribution plans with automatic escalation is predominantly set to max out at the 10 percent IRS limit. Moreover, 26 percent of these plans capped increases at rates below 10 percent—below the recommended savings rate of 10 to 15 percent of pay.[3]

This also works against participants who want to make the smart move of contributing up to the maximum amount allowed under the 402(g) limits. Not so surprisingly, only 13 percent of participants reached the maximum amount of contributions allowable in 2018, which was $18,500 plus, catch-up contributions up to $6,000, for those age 50 or older. This year the Internal Revenue Service has increased the maximum employee 401(k) contribution limit to $19,000 per year, plus $6,000 in catch-up contributions.

Teach a Man to Fish

Figure Two: Default Automatic Escalation Caps in 2017

Whether participants go it alone or get the help of a financial advisor, taking time to slow down and focus on goals and make a plan is the first and most important step for plan participants.

Yet oftentimes, people are just overwhelmed. According to Allianz Life Insurance, more than 64 percent of Gen Xers—those between the ages of 35 and 48—say the lingering cloud of uncertainty that accompanies retirement planning keeps them from taking any action to help secure their financial futures.[4]

“Engagement is the key to success. But sometimes it’s partly about waiting for participants to reach a point, or experience an event, that makes them realize they need to start taking an active role in their financial future,” says Doss.

A recent analysis of 401(k) participants found that engaging in planning, either with a representative or using online tools, helped people identify opportunities to improve their plans and take action. And, roughly 40 percent of the people who took the time to look at their plans decided to make changes to their saving or investing strategies.[5]

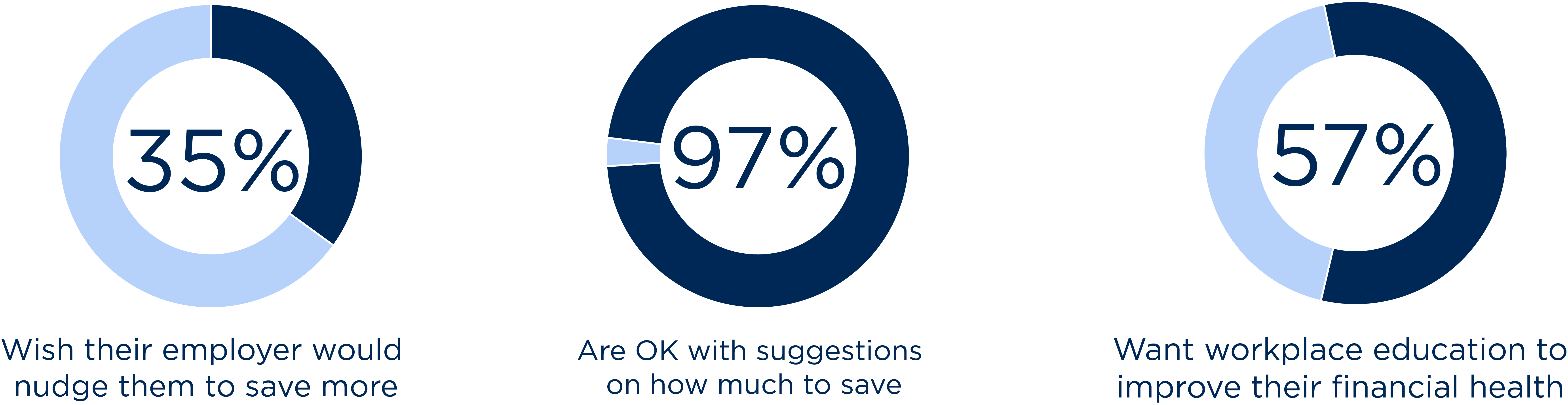

Plan sponsors may still be underplaying their role, however. The vast majority of retirement savers want to receive suggestions from their employer or plan sponsor on how much they should be putting away for retirement. According to recent research from Principal, shown in Figure Three, plan participant demand for workplace advice and education is high. More than half of employees would like workplace education that will help them improve their financial well-being, and 35 percent would welcome their employer to push them to save more.

Figure Three: Not Only Do Employees Need Help—They Want It and Are Asking for It

Source: “Is your retirement plan working?,” Principal, 2018

Boosting Financial Wellness

It isn’t only plan participants who lose out when they are not adequately engaged in their plans. Employers also feel the strain of a workforce burdened by financial stressors and uncertainty around retirement planning.

Gallup estimates the cost of America’s disengagement crisis at a staggering $300 billion in lost productivity annually. When people don’t care about their jobs or their employers, they don’t show up consistently, they produce less, or their work quality suffers.[6]

So, it should come as no surprise that an ever-growing number of plan sponsors are investing in ways to boost employee engagement. They are doing this through company-wide courses, lunch-and-learns, workshops, contests, and, most importantly, one-on-one advice.

Currently, 17 percent of large companies offer financial-wellness programs that incorporate online tools and 42 percent offer one-on-one consultations, up from 9.2 percent and 35.7 percent, respectively, in 2015, according to a recent benefit consulting firm study.[7]

It’s important for plan sponsors to understand that participants need and want to be nudged and reminded to engage in their plan.

“In my experience, the one thing that drives results the most is the one-on-one meetings because they’re completely customized,” says Doss. “I can’t overstate how important the interaction is with advice given specifically for that participant, specifically for where they are at in their life.”

Employers can ensure their workers are getting individualized information they can trust by partnering with third-party advisors, according to CAPTRUST Wealth Solutions Senior Manager Nick DeCenso, who says, “offering that kind of benefit sends a clear message to employees.”

“Working with a recordkeeper or an outside firm is one way for plan sponsors to show their employees that they take a serious interest in this,” says DeCenso. “Because most companies are not in the business of providing financial wellness advice to their employees, they’re in the business of something else.”

Keep On Nudging

Different channels of engagement, such as print communications, online tools, one-on-one meetings, or workshops can impact employees to varying degrees, and plan sponsors should strive to measure each method to determine effectiveness and make necessary changes.

A high-touch communication strategy built around milestones makes for a good way to get your participants attention, according to Matheson. “Consider sending targeted communications engaging participants to take an action. For example, a reminder to increase deferrals, timed to coincide with annual pay increases. The right message at the right time will drive positive participant behavior.”

Plan sponsors can stack the odds of success in the favor of participants by implementing automatic plan design features combined with comprehensive engagement-focused participant campaigns. This, along with technology enhancements, will move the dial forward, making it easier for plan sponsors to help participants mindfully reach their destinations.

Lastly, I’m not sure if just anyone can create a proverb, but I am going to try. Here goes. Enroll an employee at 3 percent and give them something that’s better than nothing; enroll an employee at 15 percent with immediate, engaging advice and education, and give them a dignified retirement.

[1] “How America Saves,” Vanguard, 2018

[2] John, David C., Shiflett, William R. “Higher Initial Contribution Levels in Automatic Enrollment Plans May Result in Greater Retirement Savings: A Review of the Evidence,” AARP Public Policy Institute, 2017

[3] “How America Saves,” Vanguard, 2018

[4] “Why Generation X Isn’t Planning for Their Retirement,” TheStreet, 2018

[5] “6 habits of successful investors,” Fidelity, 2019

[6] Amabile, Teresa, Kramer, Steven “Do Happier People Work Harder?,” The New York Times, 2011

[7] Tergesen, Anne, “401(k) or ATM? Automated Retirement Savings Prove Easy to Pluck Prematurely,” The Wall Street Journal, 2018