Charting a Course for 2023

“A good forecaster is not smarter than anyone else, they merely have their ignorance better organized.”

—Anonymous

As the calendar rolls into a new year, the investment industry returns to its time-honored tradition of forecasting the year ahead. This ceremony is, at best, the application of critical thinking and, at worst, an exercise in futility that can lead to false confidence and abrupt or ill-timed shifts in investment strategy. Even experts can’t predict the future, and any single forecast has a high probability of being wrong.

However, regardless of their individual utility, as investment managers and advisors we consume as many of these forecasts as we can, paying little attention to the specific numbers and focusing more on the competing narratives about how the variety of forces that affect markets could evolve in the coming year. Our goal is to understand the range of possible outcomes and the set of conditions that could create them, then use that understanding to equip resilient investment portfolios.

To do so, we think about what newspaper headlines might say 12 months from now and what type of market environment could accompany such headlines. From this perspective, 2023 appears to be an open map with many different paths to far different destinations.

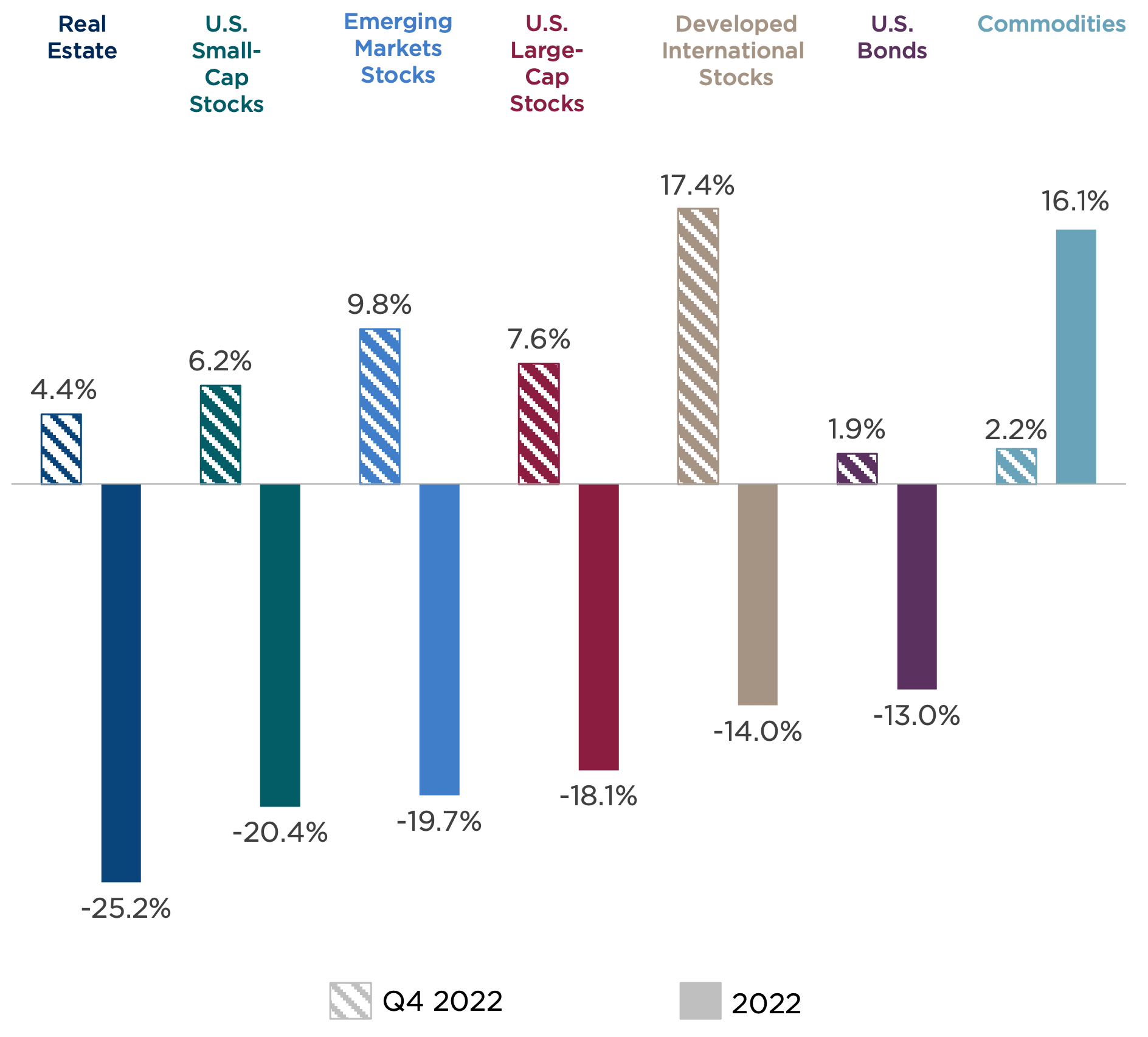

Q4 2022 Recap: A Welcome Reprieve

After a dismal first nine months of 2022, investors grew optimistic during the fourth quarter of the year, in anticipation that the Federal Reserve might be nearing the end of its tightening cycle. However, this excitement faded late in the quarter as Fed Chair Jerome Powell cautioned that conditions would need to remain restrictive for some time.

Even so, gains early in the quarter were more than enough to cushion December declines, leading to positive quarterly results across nearly all asset classes.

Asset class returns are represented by the following indexes: Bloomberg U.S. Aggregate Bond Index (U.S. bonds), S&P 500 Index (U.S. large-cap stocks), Russell 2000® (U.S. small-cap stocks), MSCI EAFE Index (international developed market stocks), MSCI Emerging Market Index (emerging market stocks), Dow Jones U.S. Real Estate Index (real estate), and Bloomberg Commodity Index (commodities).

U.S. stock market gains were broad based. The energy sector remained at the top of the charts, posting a 25 percent quarterly return. On the flip side, the mega-cap growth darlings of the last decade lagged. Internationally, investors benefited from both rising stock prices and the weakening U.S. dollar.

Bond yields were volatile, seesawing based on every Fed whisper. Despite these swings, longer-term Treasury yields ended the quarter little changed, enabling bond markets to post a modest return for the quarter. Even with a year-end rally, public real estate lost approximately one-quarter of its value in 2022. Commodities were the sole bright spot for the year, despite rising recession concerns.

What Might Happen

From here, there seem to be many sources of financial and economic uncertainty for 2023. Some, such as Federal Reserve policy, are particularly unpleasant for the markets due to their unpredictability. Others, like the trajectory of inflation in a post-pandemic world or the impact of quantitative tightening, are simply unprecedented or untested.

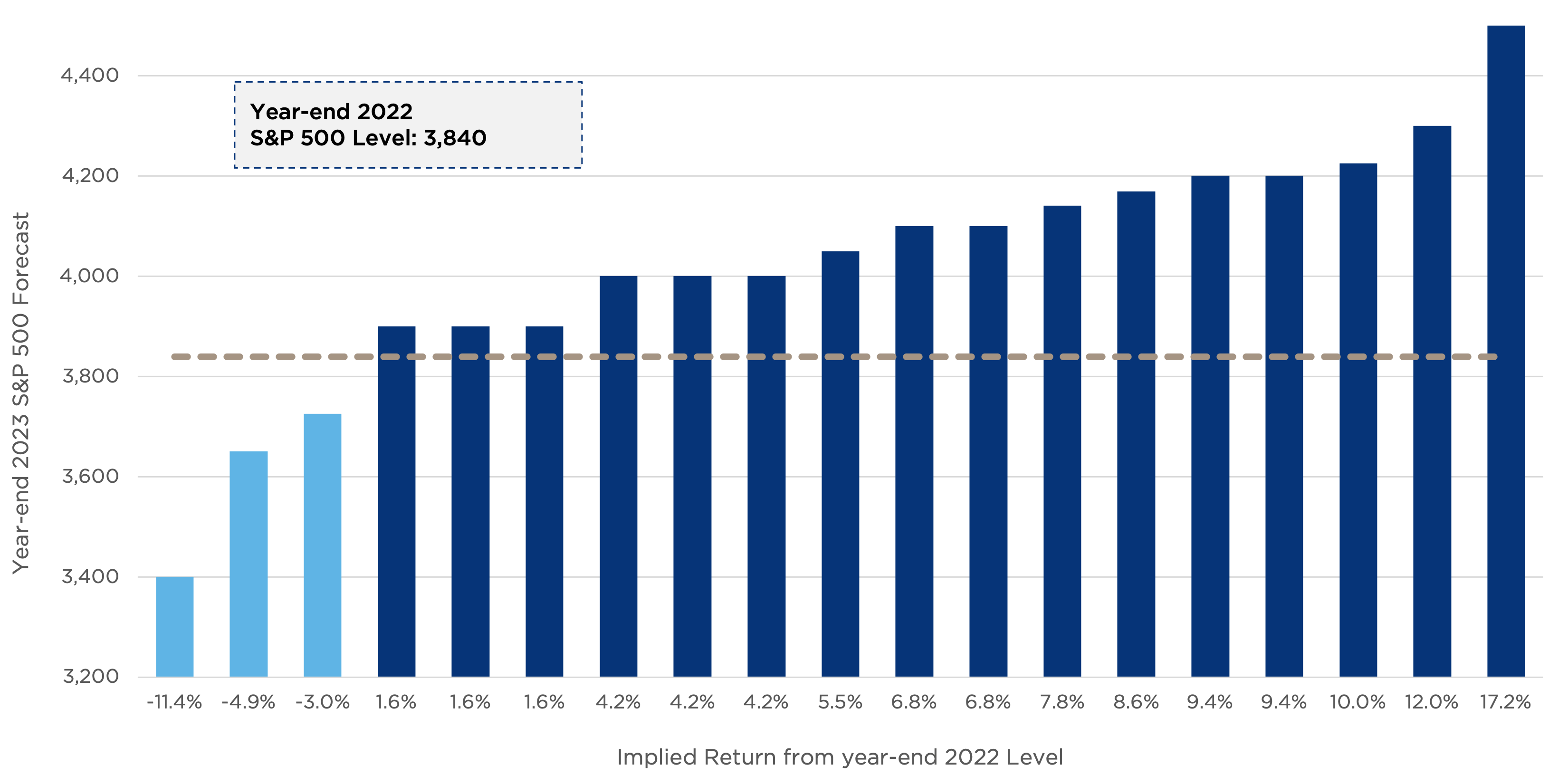

It’s no wonder that even professional forecasters have difficulty reaching consensus. As shown in Figure One, the range of 2023 forecasts for the year-end value of the S&P 500 Index from 19 professional forecasters ranges from 3,400 to 4,500. From year-end index levels, this implies a range of returns from negative 11 percent to positive 17 percent, a 28 percentage-point spectrum of expected returns.

Figure One: Investment Strategists’ Forecasts for the S&P 500 Index in 2023

Source: Bloomberg, CAPTRUST Research

The level of the S&P 500 index is just one of many elements included in such forecasts. A sample of other data points collected by CAPTRUST reflects similar disagreements, such as a year-end price of a barrel of oil from $80 to $125 and U.S. GDP growth rates between negative 2 percent and positive 1 percent.

The reality is that, even in a typical year, the consensus forecast often misses the mark by a considerable margin. This leads a reasonable person to question the usefulness of any one-year market forecast, regardless of its source.

Four Scenarios

In lieu of such specific forecasts, in late 2022 the CAPTRUST Investment Group set out to create a set of scenarios we feel encompasses the most likely range of outcomes for the coming year. As always, we approach this work with great humility knowing that what happens in reality may—and most likely will—fall outside of these scenarios. Still, the process of developing them allows us to think through portfolio implications and planning considerations that we hope will improve portfolio outcomes.

Note that while the scenarios below are primarily U.S. focused, they likely have spillover effects on the trajectory of global markets due to the size and interconnectedness of the U.S. economy.

Scenario One: Soft Landing and Mission Accomplished

After a painful campaign of rapid-fire interest rate hikes in 2022, the Fed is successful in tightening financial conditions. Combined with healing supply chains, resumption of global trade, and resolution of production bottlenecks, the tide of inflation begins to reverse by slowing the economy without stalling into recession. By mid-year, the Fed has concluded its tightening cycle.

Corporations adeptly manage through cooling economic conditions by managing costs, thus restoring balance to labor markets without a significant impact on unemployment levels. This allows corporate earnings to stabilize. A new secular bull market for equities begins as price-to-earnings valuations recover from their recession-anticipation malaise.

Investment Considerations: This goldilocks scenario may offer equity investors returns that range from modest single-digit losses to mid- or high-single-digit positive returns, depending on the timing of the Fed’s pivot and the degree that recession avoidance has already been priced in to markets. In an environment where growth is constrained, dividends and other types of yield will likely make up an important source of total return.

Scenario 2: Inflation Tamed via Mild Recession

Despite falling price pressures in goods and services categories distorted by the pandemic, inflation proves to be sticky. Meanwhile, demographic shifts, early retirements, and low levels of immigration keep the labor market tight. The combination of high input prices and labor costs forces the Fed to raise rates higher and keep them higher for longer, forcing the economy into a mild recession.

Many U.S. corporations navigate the slowing environment without significant strain. This is especially true for companies that are able to take advantage of the exceptionally low post-pandemic interest rate environment to restructure debt and those that can pass along price increases to consumers. However, weaker companies with higher financing costs suffer, creating a wide dispersion between winners and losers.

Investment Considerations:It is difficult to expect corporate earnings to grow in this scenario. Also, a souring risk appetite among investors could pull valuations lower from the modestly elevated levels of year-end 2022 toward the longer-term average. This could imply equity returns ranging from effectively flat to mid- or high-single-digit losses, with higher volatility along the way. The widening gap between winners and losers could also place a premium on investment managers with the ability to assess the specific conditions facing different sectors of the economy and the companies operating in those sectors.

Scenario 3: Policy Error Means Overshooting the Target

Ever since the stimulative jolt of slashed interest rates and aggressive quantitative easing during the early months of the pandemic, we have expressed concerns about the growing risk of a Fed policy error. Even in normal economic cycles, monetary policy acts with a lag that is unpredictable and often undetectable until it is too late.

This risk is amplified by the unique nature of current conditions and the extreme pace of Fed tightening. In this scenario, inflation recedes faster than expected as the pace and magnitude of Fed action proves too much for the economy to bear. But even as the Fed recognizes its error, it is unwilling to reverse course quickly due to fears of repeating past errors by taking its foot off the brakes too soon.

Investment Considerations: In this scenario, corporate profits come under pressure as demand wanes, leading to widespread job cuts and rising unemployment. Investors, confused by the mixed signals of tame inflation but souring conditions, finally reach the breaking point, sending markets lower as the Fed’s error becomes evident.

The combination of weaker corporate earnings and risk-off investor sentiment could lead to another year of volatile prices and double-digit losses for equities at some point in the year, while rising credit and liquidity risks make the bond market difficult to navigate.

Scenario 4: Stagflation Crisis

The direst of our four scenarios is driven by the possibility that the Fed’s toolkit is simply incapable of addressing the specific type of supply-driven inflation pressures the country is experiencing. In this scenario, inflation remains elevated, even as the Fed continues to take aggressive action, placing significant financial stress on both the U.S. and global economies.

Meanwhile, household debt levels rise as pandemic-era savings are depleted and debt service costs spike with rising rates. The housing market remains largely frozen, and the negative effect of declining home prices weighs heavily on consumer spending. As demand declines, corporations are forced to slash jobs. Due to ongoing inflation pressures, the Fed remains unable to pivot to a more accommodative stance. Stocks remain under enormous pressure as the length and severity of the recession is debated.

Investment Considerations: In this scenario—which is not what we expect—it would not be surprising to see corporate earnings decline by as much as 20 percent, leading to a commensurate decline in equity prices, if not more. Safe-haven assets, such as Treasury bonds and the dollar, would likely see higher demand as global investors seek safe harbors.

Fed Up

If we could somehow ignore the inflation story and the Fed’s aggressive attempts to combat it, the economic picture today would appear quite sturdy. Consumer spending remains healthy, and jobs are plentiful. Energy prices are down, providing a boost to consumer sentiment. Although the housing market has cooled, homeowners maintain a high degree of home equity, and the banking system is strong. Corporate earnings have been resilient.

In other words, it would be hard to look at this data and square it with the consensus view that the U.S. will enter recession sometime in mid-2023 to early 2024.

Nevertheless, the risk is there, and it happens to be the very type of risk that markets dislike the most. It is no surprise that the central character in each of these four scenarios is the U.S Federal Reserve.

But perhaps the most important change in the investment environment as we enter 2023 is the end of the ultra-low interest rate policy that has existed since the global financial crisis. This represents a sea change. The availability of zero-cost money distorted markets, amplified risk-taking behavior (witness cryptocurrencies and speculative growth stocks), boosted corporate profits, reduced the prevalence of defaults and bankruptcies, and diminished expected returns from bonds. Excesses like these must eventually be flushed out.

As interest rates rise, the fear of missing out is replaced by a more tangible form of fear: fear of loss.

Charting a Course for 2023

We believe the best-case scenario for this year would coincide with fewer surprises, more stability, and fewer large-print economic headlines that complicate the Fed’s ability to thread the needle with its policy decisions. Thankfully, as investment advisors, our task is not to predict the correct outcome. Rather, it is to understand the range of potential outcomes that are possible, how they could affect different asset classes, where risks and opportunities could emerge, and how to position portfolios for resiliency.

Regardless of the path the economy takes, whether described in one these scenarios or some other outcome we can’t envision today, investors should remain anchored to their financial plans. For long-term investors, this means staying invested. History shows that some of the most explosive daily returns occur during bear markets, and timing them is impossible. For investors with shorter time horizons, an emphasis on reliable sources of liquidity and income remains at the fore.

As always, we encourage you to contact your financial advisor to discuss your situation, what may have changed, and how your plan should adapt.