In the realm of finance, alternative investments—also called alts—represent a departure from traditional avenues such as stocks, bonds, and cash equivalents.

The term alternative is a catch-all label. Under it, the universe of alts includes a wide range of assets, many of which have little to nothing in common, except that they don’t fit into conventional investment categories.

Examples of alts include hedge funds, private equity, venture capital, real estate, commodities, infrastructure, natural resources, and collectibles like art and wine. What sets them apart is their potential for higher returns, their unique risks, and their tendencies to behave independently from traditional public markets.

Democratizing Access

Historically, alternative investments have been the domain of large institutional investors. Burdensome regulations once led managers to offer these strategies solely through private partnerships, which limited access mostly to pension plans, endowments, and the ultra-wealthy.

Now, regulatory guidelines have softened, allowing managers to build more investor-friendly vehicles, like mutual funds and exchange-traded funds (ETFs) devoted exclusively to alts. At the same time, individual investors have shown demand for alternative investment strategies, and the financial industry is responding.

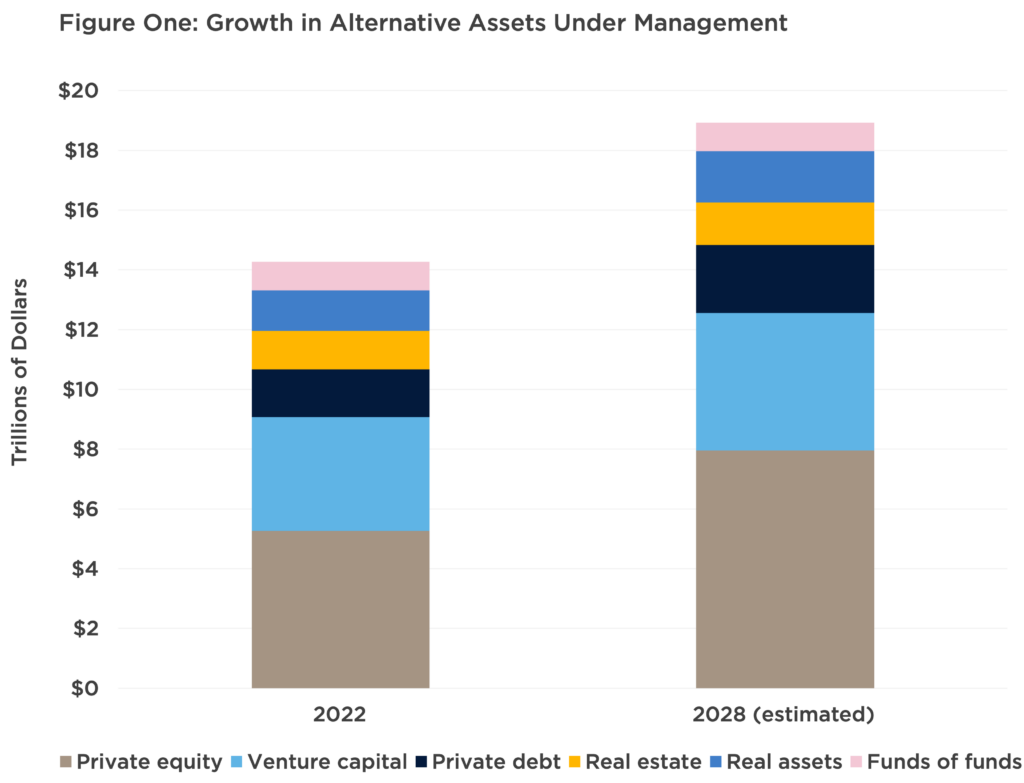

The overall effect has been a democratization of access to alts, and a corresponding explosion of assets under management. According to PitchBook, assets under management in the alts space nearly doubled between 2017 and 2022, rising from $7.4 trillion to $14.7 trillion. The same report forecasts that growth in the alts sector will accelerate exponentially in the next few years, reaching $19.6 trillion by 2028.

What is motivating investors to move their money into alternative investment strategies? Mostly, diversification and the potential for higher long-term returns.

Targets and Managers

Within the alts market, private equity and venture capital generally offer the highest potential long-term returns. Investing in private companies allows ownership access to businesses much earlier in their life cycles, when potential for growth is higher than in more mature publicly traded firms. However, private equity and venture capital typically also have the longest time horizons.

Return targets vary by fund, but in general, private equity funds aim for average annualized returns of 10 to 20 percent over a seven- to 10-year time horizon. Venture capital funds typically seek even higher returns but also involve the higher risk of investing in early-stage companies.

Of the six core categories of alts (private equity, venture capital, private debt, real estate, real assets, and funds of funds), real assets generally have the lowest targets, aiming for 5 to 10 percent net returns.

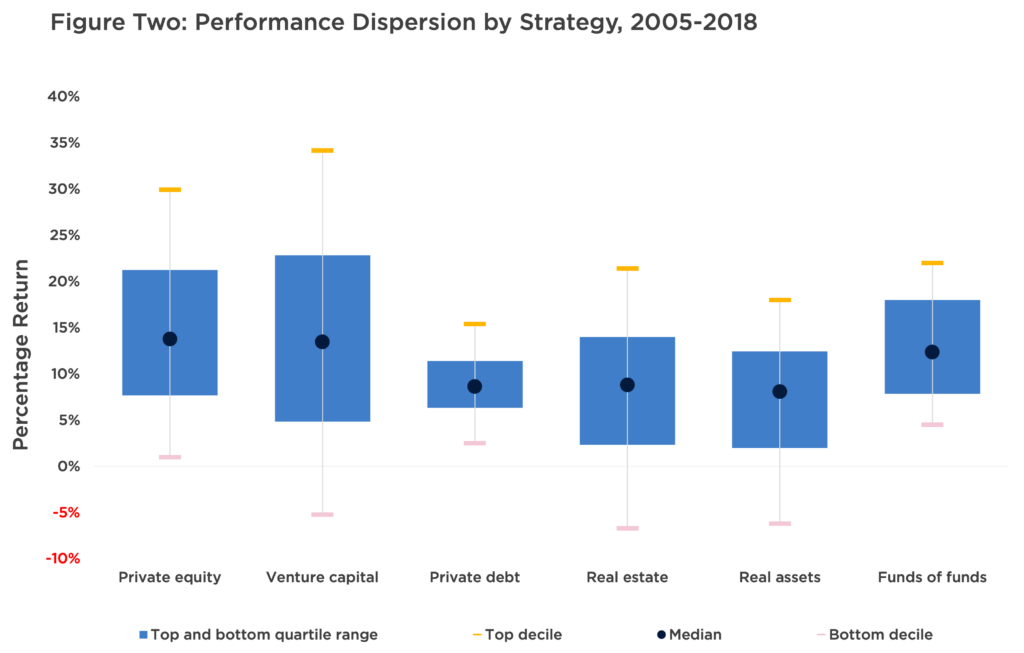

Realized performance varies considerably, based on both the inception year of the fund and the manager’s skill. Manager selection is always important for actively managed investment strategies, but for alts, it’s critical.

Figure Two shows the dispersion of returns between investment managers in different types of alts from 2005 to 2018. Over that period, the median return for private equity funds was 13.79 percent per year—an incredible bounty for investors. But it’s important to notice the full range of results. Those invested with the bottom 10 percent of managers barely made a dime, while those invested with the top 10 percent produced returns of more than 30 percent.

Source: PitchBook

For venture capital funds, the range of returns was even greater. Those invested with the top decile saw more than 34 percent returns, while those invested with the bottom decile lost money instead. The narrowest dispersion was in private debt, in which top-quartile managers earned an 11.42 percent return, and bottom-quartile managers earned 6.33 percent.

Allocating to alts can be a high-stakes game. To protect your portfolio from major losses, and improve your chances of success, align yourself with a manager who has disciplined investment and due diligence processes. In the alts universe, participating in the sector by simply entrusting your money to a manager, and hoping for the best, could be an exceptionally costly decision.

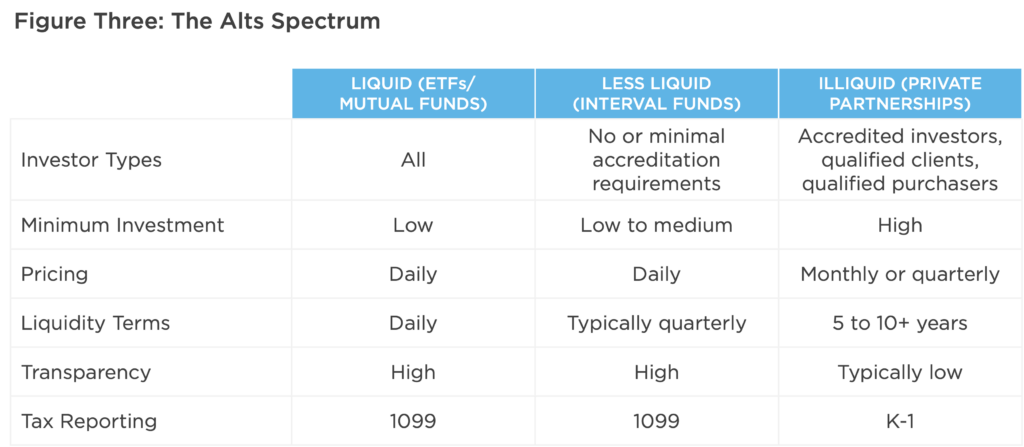

Liquidity Options: Daily to Decades

Liquidity refers to how easily an asset can be bought or sold without affecting its price. Cash is the most liquid asset of all. For other investments, the higher their liquidity, the easier it is to turn those assets back into cash. Less liquid assets require more time to be converted to cash, and the conversion may come at a higher cost.

Within the alternative investment universe, a full spectrum of liquidity options exists, from daily to decades. The most liquid alts are ETFs and mutual funds, which provide access primarily to public market investments. As a result, these alts must limit their holdings to ultra-liquid securities like stocks, bonds, currencies, and commodities, with a few exceptions.

Source: CAPTRUST Research

Private partnerships sit at the other end of the spectrum. Because the managers of private partnerships effectively set their own liquidity terms, they can target investments in illiquid private equity or venture capital companies. These can have investment horizons of multiple decades.

For investors who don’t want to lock away their assets for many years or decades, but still want some of the benefits of alts, a newer form of mutual fund, called an interval fund, provides an interesting compromise between full and zero liquidity. An interval fund is a type of closed-end mutual fund that does not trade on the secondary market. Like other mutual funds, interval funds price daily, have a high degree of transparency, and report taxes on 1099s.

Unlike other mutual funds, interval funds periodically offer to buy back a percentage of outstanding shares from shareholders at net asset value. These are called repurchase offers. Shareholders aren’t required to sell their shares back, but they can choose to participate in repurchase offers during specified intervals. Repurchases are typically done on a pro rata basis, and they allow for a percentage of shares (usually 5 to 25 percent, depending on the fund prospectus) to be repurchased during any given window.

The important piece to understand is that even though interval funds may offer liquidity windows, managers often limit the total amount of outflows available. As a result, an investor may not always be able to withdraw as much as they would like during one of these windows.

Fee Considerations

The pros and cons of specific alts strategies are complicated, and they require research and due diligence. Yet there are common considerations for everyone interested in these types of assets. One is fees.

Alternative investment strategies are actively managed, specialized strategies that often come at a premium price. Fees are usually highest on private partnerships and take the form of an annual management fee—usually 1 to 2 percent of assets—plus additional fees on profits generated by the fund. These are called success fees, carried interest, or incentive fees, and they typically range from 10 to 20 percent of the profits.

Interval fund fees tend to be lower, ranging from a 0.9 to a 1.5 percent management fee. Most interval funds also include a performance hurdle (e.g., 5 percent annually) that the portfolio needs to reach before the manager charges an additional percent of profits.

Mutual fund and ETF fees are the lowest in the alts universe because they are generally prohibited from charging incentive fees. That said, with annual management fees of 0.5 to 2 percent, their fees are still considerably higher than the fees most people are familiar with for public equity and fixed income options.

Critics of alts often point to fees as a reason to avoid them. This argument resonates. When you have a choice between two identical products, it’s smart to choose the one that costs the least.

But when it comes to alternative investments, it’s important to focus on the skill of the manager and expected net-of-fees performance as well. Net-of-fees performance refers to the return on capital reported by an investment strategy after deducting management fees and other expenses.

An allocation to any alternative investment strategy is intentionally designed to deliver a return profile that’s different from public investments like stocks and bonds. Therefore, if the expected net-of-fees performance provides benefits to a portfolio—like higher returns, lower volatility, or increased diversification—the fees may be justified.

A financial advisor can help unravel the net-of-fees performances for different funds. They can also assess the potential risks and returns for different types of alternative investment strategies to help you discern which are worth considering as part of your unique financial picture.

Getting Started

As distinctions between public and private investments continue to blur, opportunities are expanding for individual investors to participate in alternative investment strategies. And it seems this expansion is just beginning. Yet as this article highlights, understanding what you’re buying is vital, as incorporating alts can influence the fees, liquidity, and performance of your portfolio.

Alternative investments are not appropriate for all investors. But in many circumstances, alts may make a sound addition to a well-diversified investment portfolio. To thrive in this new universe, personal education or aligning yourself with an experienced advisor is critical.

Ruffolo was so passionate about his work that the last thing he wanted for his later years was to spend a lot of free time relaxing. “I don’t really have hobbies,” he says. “I get so much pleasure from work [that] I don’t play golf or tennis. I don’t go out at night or drink and carouse.”

When Ruffolo first started talking about retirement, his wife, Stephany, wondered where he would direct his abundant energy. She needn’t have worried; his retirement lasted only one month. “One, I wasn’t going to sit around and watch television,” he says. “Two, I wanted to have fun.”

Fun, for him, meant advancing the science he loved, so Ruffolo designed his own version of retirement. Let’s call it unretirement.

“I have a lifetime of knowledge about how drugs are discovered and developed,” says Ruffolo. “Companies want me to help them develop these drugs, and I’ll do it as long as my health holds out. It keeps me busy, and I’m having fun, yet without the crushing burden of responsibility that I had when I was working.”

Before retiring, Ruffolo led a 9,000-person team and often worked 12 to 16 hours a day, seven days a week. He rarely slept more than four hours a night, rising at 4:00 a.m. to clear his email inbox before arriving at the office by 5:00 a.m. Now, at 74 years old, Ruffolo sets his own schedule.

“I get up at 1:30 or 2:00 a.m., never later,” he says. “I do an hour on the treadmill, 30 minutes of weights, then start work. People think I’m crazy, but it makes me happy. There’s a good feeling I get when I’m awake before other people.”

These days, Ruffolo is a consultant for several pharmaceutical companies, a board member for multiple biotech startups, and an expert witness on patent infringement lawsuits. He travels frequently to Asia, the Middle East, and Europe.

He teaches, lectures, and—with Stephany—engages in philanthropic endeavors, including renovating a lecture hall at The Ohio State University, his alma mater. It’s a packed and fulfilling life, designed very much to his own specifications.

Unretiring in Retirement

While Ruffolo’s version of work during retirement may seem extreme, the trend of unretirement has gained attention in recent years as a larger share of baby boomers approach this stage of life in innovative ways. These go-getters are creating paths that include some form of intermittent, remote, or scaled-back work. Some are trying a different field altogether.

Nearly one in five adults age 65 or older is employed today—an increase from only 11 percent in 1987, according to the Pew Research Center. Even among those 75 and older, about 9 percent are employed, more than double the share in 1987. College-educated workers are more likely to continue working than those without a college degree.

“There’s a shift in people’s idea of retiring because of how the workforce has changed, especially in the past few years,” says Evan Cumalander, a CAPTRUST financial advisor in Wenatchee, Washington. “As much of the workforce has gone virtual, some individuals who already retired have now been hired back to work remotely or have stayed on in consulting roles.”

On Your Own Terms

One factor contributing to the unretirement trend is that work has become more age-friendly and flexible due to technology tools and new social norms—like flexible hours and virtual meetings—that became more common during the pandemic.

“Before, people were waking up at 7:00 a.m., making coffee, driving to an office, and spending a lot of time away from their families,” says Cumalander. “Now, those who have perfected their craft throughout their careers can be just as effective working reduced hours virtually.”

One of Cumalander’s clients, who worked at a food distribution company, changed her whole approach to retirement when it became possible to do her job remotely. As the main contact for some strategic customer relationships, she negotiated with her employer to continue working after age 65 as a 1099 consultant.

1099 consultants are considered independent contractors, not employees. (The number 1099 refers to the tax form employers must file for each independent contractor.) As such, Cumalander’s client was ineligible for employer-sponsored health insurance, but she was able to get on Medicare.

“She lives an almost-retired lifestyle, with very flexible hours,” Cumalander says. “She’s able to keep one toe in the water, working with people she likes and having something to do, while getting supplemental income so she doesn’t have to withdraw as much from her retirement accounts.”

Cumalander sees a trend of similar trajectories. “With remote work now a common option, people can extend the length of time they work,” he says. “Instead of stopping work completely at age 65, they might start paring back at age 60 and continue working until age 70 or later.”

Connecting and Contributing

Work is often a core part of a person’s identity. And research shows that continuing to work can help people stay sharp, maintain skills, and feel they’re a part of something.

“For someone who has worked 40 to 50 hours a week for their entire life, many of their social and emotional connections may come through their workplace,” says Teri Parker, a CAPTRUST financial advisor in Riverside, California.

Leaving that world behind entirely can create a void, she says. “Suddenly, no one is calling to ask your opinion, or you’re no longer writing a paper on a new approach,” says Parker. “It can be disorienting.”

A renegotiated work-life balance can make all the difference in an enjoyable unretired lifestyle.

For instance, Cumalander points to another client: a veterinarian who sold his practice at age 59 and moved to the coast, a few hours from his former home. The new owner asked if he would support the continuity of the business by phasing out gradually instead of leaving altogether. He happily agreed.

“This client loved his work so much that he would drive for two hours and stay in an apartment at his best friend’s house on Tuesdays, Wednesdays, and Thursdays every week,” says Cumalander. “Then, he would be so excited to drive back to the beach, where every weekend was a long weekend and felt like a vacation.”

Financial Planning Implications

Working after retirement can help defer dipping into your nest egg and add structure to your days, but a paycheck can also cause unexpected repercussions for retirement income and taxes. Your age, the amount you’re earning, and the type of employment you’re engaged in are just a few of the factors to be mindful of.

Before returning to work or negotiating consulting terms, it’s good to check with a financial advisor about potential implications for your Social Security benefits and retirement withdrawal strategies.

If you aren’t yet receiving Social Security benefits, post-retirement work may allow you to delay starting, which will likely mean a higher benefit down the road. For people who are already drawing Social Security and are full retirement age or older, earned income has no impact on benefits.

However, for those younger than full retirement age, complex rules apply. For one thing, when earnings exceed $22,320, the Social Security Administration will withhold $1 from benefits for every $2 earned above that threshold. This money is credited back after full retirement age. A different rule applies the year someone reaches full retirement age.

“There are so many rules for different scenarios,” says Parker. “I would suggest people make an appointment with the Social Security Administration or with their financial advisor to clearly understand the full picture before making the decision to go back to work.”

Unretiring could also change your strategy for taking retirement distributions. “If you have income, maybe you’ll need to withhold more, or maybe you’ll want to reduce or stop taking an IRA distribution,” says Parker. “If the wages are significant, it’s a good idea to meet with a tax professional.”

When someone is drawing a pension and then returns to work at the same company, there’s a big difference between going back as a 1099 contractor and going back as a regular employee. “If you’re a consultant, you might not qualify as an employee, so you might be able to keep drawing on the pension,” says Parker. “However, returning to the company as a regular employee could create a problem. Before making any decision, talk to a pension expert in human resources to ask about constraints.”

Life expectancies today extend long past traditional retirement age, so it’s likely the unretirement lifestyle will continue to evolve. “That’s a long time to have nothing to do,” says Ruffolo. “For retirement, you should do what makes you happy. For me, it’s about staying active and giving what I have to offer.”

Article by Jeanne Lee

It’s something Thomson would never have imagined he’d be doing for a living: leading small-group photographic safaris.

On this last trip, a mother leopard called her two cubs to come out of hiding and reunite with her, high up in a jackalberry tree. Jan Shealy, who traveled with her husband, Tommy, was blown away. “I don’t even know where to begin,” she says. “What an adventure!” It was Shealy’s first safari.

Thomson’s own first safari was in 2015. Recently retired from the recruiting business he owned and operated for almost two decades, Thomson is now in his fifth year of taking clients and friends to places like Zimbabwe’s Victoria Falls and Kenya’s Maasai Mara National Reserve through his company, Boone Safaris.

2024 is the first year in which his passion for wildlife will be his full-time occupation.

Going Pro

The dream hatched from a simple hobby. When his kids were growing up, Thomson took pictures of them for fun. “I even became the sports photographer at their high school,” he says. When one of his sons advanced to college football, Thomson happily focused his camera on the field and became the official photographer for Yale University’s football team during his son’s first year of school.

Once his kids graduated, space opened in Thomson’s life, so he started aiming his lens at landscapes and wildlife instead. He especially loved photographing the larger fauna at Grand Teton National Park in Wyoming.

Thomson studied the work of professional photographers and followed them on social media. One day, he happened upon a GoFundMe campaign for a renowned wildlife photographer. In exchange for a donation, the photographer would join him on a safari to watch the Great Migration in the Maasai Mara.

The trip turned out to be the most exhilarating of his life. “I vividly remember the first time I saw a lion in the wild,” Thomson says. “There were no fences. It was just a lion out there lying down, sleeping. I probably cried. Seeing a leopard in real life, a cheetah, massive herds of wildebeest, and zebra as far as the eye could see, it was a spiritual experience.”

Thomson’s pastime evolved into a calling. He traveled and studied with California-based photographer Roy Toft. “I went with him to a workshop in Costa Rica, then to Brazil to photograph jaguars, then to Botswana, and then to Patagonia to photograph pumas,” Thomson says. “I thought he had the coolest job in the world.”

Soon, Thomson’s safari habit became too costly to keep up, and he got the idea to start Boone Safaris. He has been sharing his passion for African wildlife ever since.

By Land, Air, or Water

Thomson’s photographs brim with emotion. Some feel like portraits, capturing an animal’s personality and mood. A muscular hippo tilts its head, looking back over its massive round shoulder as if asking a question. A delicate bird with a pointy beak passes a winged insect to its mate. A cheetah cub, mid-leap, looks as playful as a preschooler.

One of Thomson’s goals is to become certified as an African field guide. To that end, he’s spent hundreds of hours studying African species and their behaviors. A benefit of his deep knowledge is that it gives him an advantage in setting up shots and sharpening his photography.

“When a lion comes into the pride, the first thing it does is make contact with the other lions,” he says. “They rub their heads together.” Because he can anticipate this behavior, Thomson can make sure he’s in position to capture the best shot.

At Boone Safaris, guests choose from different types of game drives and viewing. “The most common one is a specialized Land Cruiser that gets you very close to the animals,” he says.

“If you’re still and quiet, the elephants will come right up to you.” Another option is a hot air balloon, drifting above big herds of animals as they cross the reserves.

“We also do walking game drives in a private conservancy in Kenya,” Thomson says. “We go out with a Maasai warrior who knows the land.”

On his most recent trip, Thomson led a game drive by small boat on the Chobe River. “You’re down low in the water, pulling up next to hippos, and the elephants are swimming across,” he says.

Thomson notes that hippos may react when humans get close. “Hippos can charge. They’re fast in the water, and they’re powerful, but they don’t swim. They run on the bottom. If they charge, our boat driver will speed away, and the boats are custom designed so that they won’t tip over.”

Close Encounters

Getting close to large animals is a thrill. For Gardner Lee, of Birmingham, Alabama, traveling with Boone Safaris in 2022 was also a precious opportunity to bond with his daughter, Anna. In Kenya, a male lion approached their vehicle. “What we didn’t notice was a female lion slipping up along the side,” he says.

“With my daughter’s camera focused on the male, the female jumped from a creek bed toward the truck and came within five feet of Anna,” says Lee. “The entire vehicle let go of one big gasp.”

They also watched a pride of female lions track down a herd of wildebeests and pick out the weakest. “Seeing these animals in the wild as they have existed for millennia makes you feel like you are a part of the past,” Lee says. “It gives you a new appreciation for our ancestors. It awakens you to your basic instincts as a human being.” He left with a lasting desire to help preserve the animals’ ways of life, away from civilization.

To Love and Protect

For Thomson, Boone Safaris means much more than simply turning a profit. He wants to raise awareness of conservation efforts. Visitors to Africa often focus on seeing big game animals, but Thomson loves to introduce them to lesser-known species as well, like his favorite, the painted dog.

These big-eared, mottled canines are among the most endangered animals in Africa. Thomson became fascinated with them after befriending a researcher who had studied them for decades. Painted dogs are sociable; they hunt in groups. They have only four toes on each foot, an adaptation that makes them extremely agile. “Their intelligence and cooperation make them the most successful hunters in the animal kingdom,” Thomson says.

Once considered problem animals, painted dogs were frequently killed on sight by ranchers. There are only 6,600 living today. “Europeans gave them the name wild dog, and that name really stuck, but it sounds like a feral domestic dog that deserves to be shot,” Thomson says. “At Boone Safaris, we give 1 percent of our revenue to the Painted Dog Research Trust [PDRT].”

Thomson had the chance to stay at the PDRT compound for five days during his recent trip. He slept in a small hut and observed the work being done by Zimbabwean university students. The students were viewing recent camera trap images and identifying individual pack members. Thomson says he was taken aback to see the name of one of the dogs. It was Boone.

Startled for a moment, he then remembered that his daughter had the privilege of naming a new dog two years ago when she worked at PDRT. She had named this one after her father.

Some of Thomson’s clients have been so moved by their experiences in Africa that they have allocated a portion of their charitable giving to causes like the painted dog and the Maasai community. “You’re probably not going to do that if you haven’t been here,” Thomson says.

As the Senegalese conservationist Baba Dioum put it, “In the end, we will conserve only what we love; we will love only what we understand; and we will understand only what we are taught.”

For Thomson, love and conservation are entwined. “I don’t want to have a company just to make money and build a big business,” he says. “I want to take people on safari so they’ll appreciate these animals and want to protect them.”

Article by Jeanne Lee. Photographs by Boone Thomson.

The patient would insist their hearing was fine. It was just that other people were mumbling, says Ashby-Scabis, senior director of audiology practices at the American Speech-Language-Hearing Association (ASHA). Most times, she says, the test would show hearing loss.

If you’ve noticed other people talking too softly, found yourself annoyed by people speaking to you from other rooms, or found that your usual television or radio volume is creeping steadily upward, you might have hearing loss too. And if you do, you’re in good company.

According to the National Institutes of Health (NIH), 15 percent of all adults have trouble hearing—a number that increases to 33 percent for people between ages 65 and 74 and nearly 50 percent for people over 75.

Hearing experts say it isn’t surprising that most people don’t know they’re having trouble hearing, since hearing loss usually happens gradually over time. But missing or ignoring the signs can have profound consequences for your relationships, work, health, and safety.

How and Why Hearing Loss Happens

Age-related hearing loss is largely a matter of wear and tear on the inner ear and the nerves between our ears and brains, says Ashby-Scabis.

Your genes, and health conditions like diabetes and high blood pressure, can raise your risk of hearing loss, says Patricia Gaffney, a professor at Nova Southeastern University in Fort Lauderdale, Florida, and president-elect of the American Academy of Audiology.

Noise exposure also matters. Too many loud concerts or a noisy job without ear protection can damage your hearing over time. “But most people don’t really notice the damage on a day-to-day basis because it’s such a gradual change,” says Gaffney.

“The first thing people might notice is that, when they enter a noisy environment, it’s much harder to have a conversation,” she says. “They may also start to find other people’s speech less clear, especially the voices of women and children, because hearing at higher pitches declines fastest.” When people start to lose their ability to hear high pitches, they’ll hear mostly low pitches instead. These sound like mumbling, hence the common complaint.

Turning up the TV and asking others to speak up won’t fix the problem, says Gaffney. “If you have a faulty inner ear, no matter how loud we make it, it’s still not going to make things any clearer.”

Other warning signs, according to the NIH, include trouble understanding people over the phone, often asking people to repeat themselves, and struggling to understand a conversation when two or more people are talking. Tinnitus, or ringing in the ears, is another possible sign.

How Hearing Loss Impacts Your Life

ASHA reports that adults who know they have hearing loss are unlikely to do anything about it unless it gets severe. It’s not unusual for people to wait 10 years or longer to consider hearing aids, the primary form of treatment. “Over those years, you’re missing out on so much,” says Gaffney.

Studies have linked untreated hearing loss to depression, anxiety, and social isolation, says Laura Coco, an assistant professor of audiology at San Diego State University. “As communication gets harder, people just slowly drop out from their communities and their families.”

Working adults can lose confidence in their ability to do good work, she says. Untreated hearing loss is linked with lost income and a higher rate of unemployment, according to the nonprofit Hearing Health Foundation.

It’s even linked to a higher risk of falling, perhaps because poor hearing creates a “sense of disorientation,” says Ashby-Scabis.

In the past few years, researchers have also found an increasingly strong connection between hearing loss and cognitive decline. First, researchers at Johns Hopkins University found that people with mild hearing loss were twice as likely to develop dementia as those with normal hearing and that those with moderate to severe hearing loss were at even higher risk.

More recently, the same researchers found that getting hearing aids led to a 50 percent drop in the rate of cognitive decline in older adults who had both hearing loss and an elevated risk for dementia.

It is important to note that the studies don’t prove that hearing loss leads to dementia because correlation is not causation. “One thought is that there’s a common cause that leads to both dementia and hearing loss,” says Coco.

If untreated hearing loss does increase the risk, isolation could be the link, she says. We’re social creatures, and when we lose connection, our brains suffer.

Another consideration is that untreated hearing loss can make someone seem like they have memory problems when they don’t. “When you don’t hear what people are saying, you can’t remember it,” says Ashby-Scabis. “That’s another reason to get answers and get help.”

Article by Kim Painter

It’s easy to believe that wealthy people don’t have to worry about their finances. But the reality is that they often face their own unhealthy consumer habits, fueled by access to money, societal pressures, and a culture that encourages consumption.

Unhealthy Habits

“We all know Americans struggle with their day-to-day finances,” says Chris Whitlow, head of CAPTRUST at Work. “But it isn’t only lower- and middle-income people who face challenges.”

According to a recent “Mind over Money” survey from Capital One and The Decision Lab, two-thirds of Americans feel anxious about their financial situations, and more than half have difficulty controlling their money-related worries. They’re most worried about their financial futures, including not having enough money to retire, keeping up with the cost of living, and managing debt.

“Having wealth solves some of your money issues, but it doesn’t make you immune to financial stress,” says Whitlow. “Wealthy people just suffer from a different set of worries.” Often, these worries are related to spending behaviors.

Problems of Abundance

While some of these issues might rightly be called high-class problems—or problems of abundance—they are, nonetheless, problems, and they can leave a significant mark on a family’s finances. Some spending behaviors can have negative financial consequences.

- Impulse purchases. The ability to afford more can lead to buying impulsively, bypassing discussion, budgeting, or consideration of actual need. “This can be especially tempting with luxury items or high-end experiences,” says CAPTRUST Financial Advisor Jeremy Altfeder.

- Conspicuous consumption. When money isn’t a major concern, it can be more difficult to resist the allure of having the latest and greatest of everything. People fall into this trap when they feel pressure to maintain a certain lifestyle or appearance, even when it strains their finances.

- Lifestyle creep. This occurs when your expenses unintentionally increase along with your income. “After getting a big raise, you may, for example, shop and go out to eat more, or add a long weekend trip to your annual vacation agenda,” says Altfeder. If you do, that raise won’t translate into more money in the bank.

- Keeping up with the Joneses. There isn’t a single clinical term for “keeping up with the Joneses,” but it appears to be related to several concepts. Social comparison is a normal human tendency; in the context of keeping up with the Joneses, it becomes excessive and focused on material possessions or social status. Fear of missing out (FOMO) may also play a part. FOMO creates anxiety about missing out on experiences or possessions others have, and it can fuel the desire to keep up.

As wealth increases, so does the ability to spend, and the impact of these behaviors can be significant. Combine a couple impulse purchases, a dash of lifestyle creep, and a touch of keeping up with the Joneses, and you may find you’re not making any real progress toward your long-term financial goals.

A Few Helpful Tips

“We live in a consumer-driven society,” says Altfeder. “We’re bombarded by commercials telling us we should spend our money on cars, trips, and things for our homes. And, of course, these ads are targeted at people with the means to buy. It’s no wonder so many Americans suffer from overspending and too much debt.”

There’s nothing inherently bad about spending, and it’s normal to spend more as income and wealth rise. What’s important is that you make intentional choices about your spending rather than falling prey to ad messaging and dysfunctional spending behaviors. Here’s how.

Make a not-a-budget budget. “While you may not need a detailed monthly budget, doing a little math to understand what you’re spending can be revealing,” says Altfeder. Even small purchases add up over time, and that once-in-a-while splurge that happens a little too often can take a toll.

Get the full picture. Often, the cost of luxury purchases extends beyond the initial outlay. For example, buying a vintage car, a second home, or a plane include significant maintenance and upkeep costs that may generate financial stress. Creating a full estimate of those expenses can inform the decision-making process and reduce the likelihood of surprises down the road.

Don’t neglect long-term planning. Focusing on the here and now can lead to neglecting retirement savings, estate planning, and other long-term financial goals. A good financial plan will get you excited about the future and may cause you to rethink your current spending. Further, just because things are comfortable today doesn’t mean they’ll stay that way forever. A plan will help identify likely outcomes and biggest risks.

Avoid bad debt. Easy access to credit and the ability to afford the payments on it can lead to accept more than a healthy amount of debt. “Good debt like mortgages, student loans, and business loans can help enable long-term goals,” says Whitlow. “Bad debt—like credit cards and any loan used to buy a depreciating asset—steers you away from your goals. Moderation is key, and even good debt, when overused, can turn bad.”

Acknowledge the impulse. It can be difficult to notice when you’re falling into the trap of FOMO or an impulsive purchase. That’s why these behaviors are so problematic. But it’s possible to cultivate mindfulness about spending in order to dampen the impulse.

A few simple rules may also help. For example, implement a timeout rule that requires you to sleep on spending decisions more than a certain amount, or delay that new car, boat, guitar, or cruise purchase by 30 days and see if you still need it. You may find you do not, and over time, you’ll become more engaged when big spending decisions arise.

Spending with Intention

While wealthier Americans may not suffer from the make-or-break financial issues and stresses that average Americans face, they do experience their own breed of money-related stress. The allure of consumerism is strong and carries real financial consequences. But it doesn’t have to be that way. With a more intentional approach to managing spending, wealthy Americans can enjoy the fruits of their wealth while also attaining their long-term financial goals with less stress and worry.

“I have these conversations with clients—not all the time, but often—and they’re always surprised by how much they spend and what they spend on,” says Altfeder. “A lot of the time, they don’t see a lot of value in what they’re paying for, which makes it easy for them to dial back. They feel like they’re making a positive difference in their finances and are more in control of their lives in general.”

Article by John Curry

A: The Department of Labor (DOL) recently issued the Retirement Security Rule, also known as the fiduciary rule. This rule defines the term investment advice fiduciary for purposes of the Employee Retirement Income Security Act. The new rule is the culmination of a long process, through which the DOL has attempted to better clarify what a fiduciary is and what constitutes fiduciary advice for retirement accounts like 401(k)s and individual retirement accounts. This may be one of the reasons you’ve heard the term a lot lately, but the concept of the fiduciary is not new. In fact, it dates to ancient Roman law.

In the context of personal finance and investments, registered investment advisors (RIAs) must adhere to a fiduciary standard of care. In other words, RIAs are legally bound to always act in your best interest.

This means that the investment advisor must always put your interest ahead of their own and must disclose any real or potential conflicts of interest. In other words, RIAs are required to provide advice and recommendations that are best for you, even if it means earning less for themselves or their firms. The fiduciary standard is the highest ethical standard in the financial services industry.

Another thing to know is that, in recent years, the U.S. Securities & Exchange Commission issued a separate rule called regulation best interest, which raised the standard applying to stockbrokers.

However, the primary difference between RIAs and brokerage firms still exists. Brokerage firms sell securities in exchange for commissions. This is a transaction-based business model. RIAs render investment advice in exchange for a fee that is not contingent on transactions. In general, investment advice from an RIA is rendered on an ongoing basis, so that the RIA’s fiduciary obligation does not end after a transaction takes place.

While regulation best interest imposed a new standard on brokerage firms, the incentive still exists for brokers to recommend products that generate higher commissions.

While these distinctions may seem subtle, understanding the difference can help you make better-informed decisions when seeking financial advice. When working with a financial professional, it’s crucial to understand the standard under which they operate for the specific services you’re seeking.

CAPTRUST is a fiduciary, first and foremost. We believe in the value of investment guidance delivered solely in the best interests of our clients. The company has gone to great lengths to eliminate the kinds of conflicts of interest that are common in other parts of the financial services industry.

After all, no one knows how long they’re going to live. So how do they know they won’t run out of money?

“We recommend people do their financial planning with the assumption that they’re going to live a long time because of better preventive medicine and better treatments,” says Gray, who’s based in Raleigh, North Carolina.

Many retirees today need sufficient liquid investments to last 20 to 40 years. Otherwise, they face a longevity risk, which means they might survive longer than expected and outlive their resources.

“You may not live to 100,” says Gray. “But what if you live to 97, and you only planned for your money to last until you were 90? Then you’ll spend the last seven years broke. You don’t want to be down to your last nickel.”

That’s a scary thought, but it can happen, says Gray. “I’m currently working with a client whose mother is 93 and has had dementia for seven years. She has survived COVID-19 three times. Now she’s living in an expensive long-term-care facility, and he’s watching her burn through her assets.”

His client doesn’t want to be in the same situation.

Recent surveys reinforce the wisdom of long-term financial planning. In America, the average retirement age is 62 to 65 years old. A 65-year-old man can expect to live to age 82.5 (about 17.5 years in retirement), and a 65-year-old woman can expect to live to age 85 (about 20 years in retirement), according to the Centers for Disease Control and Prevention.

Although a small percentage of people currently make it to 100, a 2024 report from the Pew Research Center says there will be many more centenarians in the coming decades.

Calculating Expenses

Several factors go into fiscal planning for a century-long life, from expenses and asset allocation to inflation and market volatility. As a financial planner, Nick DeCenso, CAPTRUST senior director of wealth solutions, says estimating how much retirees will spend is the hardest part of developing a plan.

“We know our clients’ assets,” says DeCenso. “We know what their income looks like. We know their Social Security benefits. We know their liabilities. But anticipating spending is tough.”

“For the first three to five years of retirement, we often see a spike in spending,” he says. “A lot of folks are taking trips they’ve put off, leaning into their lifelong hobbies, or buying big-ticket items they’ve always wanted. They tend to spend less later in retirement.”

Figuring out expenses is important, says Briana Smith, a CAPTRUST financial advisor in Raleigh, North Carolina. Smith helps clients develop plans for a life expectancy of 95.

“We want to get as accurate a number as possible,” she says. “For instance, we need to know if you’re spending $15,000 a year on groceries and $30,000 a year on travel.”

What might seem like a small difference on paper can have a significant impact when you grow these expenses with inflation over long periods. Smith says some people like to create a detailed budget. Others just want a general understanding of how much they spend.

Adding Costly Items

Beyond regular living expenses, each person’s long-term financial plan needs to incorporate occasional large expenditures, such as buying a second home or helping adult children purchase property, paying for weddings or grandchildren’s educations, or some combination of those things.

These expenses are important because they have big potential to move the needle, jeopardizing the chance you’ll achieve your financial goals. “You may end up paying for a wedding that’s so expensive it impacts your retirement lifestyle,” Gray says.

Today, more clients are making big gifts to their children, grandchildren, and charities during their lifetimes, says DeCenso. “If I live to 100, for example, that means my two daughters are going to be 70 before they get an inheritance. If I’m able to give them financial gifts while I’m still alive, then I get to see some of the fruits of those gifts.”

Some parents opt to give each child or grandchild the maximum annual amount that you can give without reporting it to the Internal Revenue Service. In 2024, that amount is $18,000 from one parent or $36,000 from both. “That’s fine as long as it doesn’t put the parents’ retirement plan in jeopardy,” Smith says.

Gray suggests taking care of yourself first. “Make sure you’re comfortable with your resources and planning so you can have the lifestyle you want and eliminate—or at least mitigate—your risk of creating a financial shortfall.”

Models and Scenarios

Advisors use financial planning software to give clients a reasonably reliable look into the future.

The software considers factors such as age, assets, living expenses, charitable donations, automobile expenses, education costs, and gifting to family. Once all your expenses and sources of income are in the system, it can calculate different long-term financial scenarios, adjusting for inflation, market volatility, increased healthcare costs, and other factors.

The goal is to model multiple versions of the future so you can prepare accordingly. “From there, we can determine how growth-focused each client needs to be, how much money they’ll need available at key moments in their life, and how much of their total portfolio should be allocated to different types of investments,” Gray says.

For a lot of people, modeling creates peace of mind.

“We’ve worked with people who were absolutely petrified about the future, and after using these software tools, they were comfortable living a lifestyle that was considerably nicer than they thought they could ever afford,” says Gray.

Customizing Investments

Despite what many online calculators might say, when it comes to investments during retirement, there is no one-size-fits-all strategy. “The best mix depends on each person’s unique assets and liabilities,” says DeCenso. “Now more than ever, people are retiring with multiple assets beyond their homes and employer-sponsored retirement accounts.”

Besides Social Security and, in some cases, pensions, retirees might have other income streams, such as rental properties, business partnerships, or severance from a company. They might also be consulting or working full or part time.

“All of this factors into how we decide on the right mix of equities and fixed income in investments,” says DeCenso.

Sometimes, retirees go too far in one direction. “I see folks who are at each of the extremes,” he says. “They think, I’m retired, so I’m going to be as conservative as possible with my investments.”

“Other folks are too aggressive,” he says. “They keep too high of a percentage of their assets in equities after retirement, which can create substantial risk.”

There’s a lot to consider when making investment decisions. Someone who’s getting Social Security and has a pension and other sources of income might need to withdraw less from their portfolio. This person can afford to take more risks. But a retiree who receives smaller Social Security benefits and has no pension can’t afford to take as much risk.

Dividing Investments into Buckets

Smith suggests thinking about investments as buckets:

The Cash-Flow Bucket: Keep one to three years of your retirement withdrawal needs in cash or cash-equivalent accounts, such as a money market fund or—in today’s interest rate environment—an exchange-traded fund (ETF) that tracks a three-month Treasury bill. “This can help retirees avoid selling stocks if there’s a dip in the market,” Smith says.

The Income Bucket: This is money for the intermediate term. “We recommend having roughly seven years’ worth of withdrawal needs in a more income-focused bucket, something that includes a balanced asset allocation with a mix of stocks and bonds,” she says. “It could even include some private credit alternatives to boost yield.” This asset allocation is dependent on the retiree’s risk tolerance. “You have a nice waterfall effect with dividends and interest flowing from the income bucket to the cash-flow bucket,” Smith says.

The Growth Bucket: The first two buckets should fund the first 10 years of retirement. “This creates peace of mind and allows clients to be more growth oriented with their longer-term assets in the third bucket,”

she says.

Avoiding a Financial Shortfall

The 4 percent rule is a guideline that says if retirees withdraw 4 percent annually from their portfolios, they won’t exhaust their savings. “In general, this is a good budgeting strategy,” Gray says. “However, it’s prudent to check your withdrawal percentage regularly. If your rate starts to creep up, then 4 percent might not be sustainable.”

In some cases, clients aren’t worried about running out of money. They’re more concerned with preserving investments to pass on to their heirs or favorite charities.

Smith suggests clients might want to live off dividends and interest to preserve the current buying power of their portfolio. She says financial advisors often coordinate with a client’s estate planning attorney.

“Sometimes, we need to help strategize the most tax-efficient estate plan,” Smith says. “This could include setting up and funding certain types of trusts or simply considering which assets should be directed toward heirs versus charities.”

In some cases, people choose to leave homes to their children. Other retirees downsize during their golden years and use some home equity to cover expenses.

“My mother-in-law is retired and conscious about her spending,” says DeCenso. “She lives in a 3,000-square-foot house that is worth $1 million and is almost paid off. If she needs more money, she has a lot of equity to work with.”

Regular Check-ins

Retirement planning is not a one-time exercise. “That would be nice, but it’s not realistic,” says DeCenso. “Nothing will go precisely as planned. The markets won’t move in a straight line and may do better or worse than everyone thought. Also, your spending will fluctuate and evolve. There will be times when you spend more or less than expected.”

Smith says she tells clients to revisit their plans annually or any time they have a major life change, such as moving to another state, having more grandkids, getting divorced, or having a death in the family.

DeCenso says some have a clear mental picture of the portfolio amount they’re determined to stay at or stay above. “They think: If I dip below my peak savings amount, it feels like I’m trending toward zero,” he says. Sometimes, this type of thinking can cause more harm than good, causing people to underspend and worry unnecessarily.

“You saved for your retirement, so enjoy it,” he says. “This is what those long years of saving were meant for.”

Article by Nanci Hellmich

A: Investing in gold may provide some benefits as a portfolio diversifier and potentially as a hedge against inflation, but there are several issues to consider when contemplating an investment in this or other precious metals. Here are a few:

- Store of value. Gold has traditionally been viewed as a store of value and a safe-haven asset during times of economic uncertainty and high inflation. As currencies tend to lose purchasing power due to inflation, gold may be viewed as a way to preserve wealth during these periods.

- Limited supply. The supply of gold is relatively limited and cannot be easily increased. This scarcity can make gold more attractive at times when the supply of money is increasing.

- Portfolio diversification. Adding gold to an investment portfolio can help hedge against the potential negative effects of inflation on other asset classes, such as stocks and bonds. In addition, gold has historically shown a low correlation to stocks and bonds, providing a diversification benefit.

- Timing. While gold is often considered an inflation hedge, its price can be volatile and does not always move in tandem with inflation in the short term. Also, timing the purchase and sale of gold can be challenging, so it’s essential to have a long-term investment horizon.

- Trade-off. While gold may help preserve wealth during inflationary periods, it does not generate income or dividends like other assets, such as bonds or stocks.

Investors should also be mindful of the additional costs of investing in physical gold, including storage, insurance, and transaction fees, which can erode potential gains. Exchange-traded funds (ETFs) that include gold may be a cost-effective alternative but do not offer the same features as investing in physical gold.

If you do choose to invest in gold, it should be as part of a well-diversified investment strategy and should not be considered a stand-alone solution to combat inflation. As always, consult with your financial advisor to determine what makes sense for you based on your investment goals, risk tolerance, and overall financial situation. interest that are common in other parts of the financial services industry.

A: While it’s true that elections can drive market volatility and shifts in investor sentiment in the short term, history shows that, over the long run, fundamentals like economic growth and corporate earnings tend to be far more important drivers of stock returns.

That said, there are some interesting historical trends around stock market performance during election years, especially years when an incumbent president is running for reelection.

According to our analysis, for the last 10 election years in which an incumbent was running, the S&P 500 Index has ended the year in positive territory, with an average return of 17.4 percent. That’s well above the average annual return of around 10 percent for all years.

Why might markets tend to perform better in incumbent reelection years? A big part of the answer likely comes down to the incentives for incumbents to take pro-growth policy actions to boost their reelection prospects. Fiscal and monetary policy may become more stimulative in these years, as incumbent administrations work to keep an economic expansion going.

We’ve already seen some of this dynamic play out, with large fiscal packages like the Creating Helpful Incentives to Produce Semiconductors (CHIPS) Act, the Inflation Reduction Act, and the resumption of tax credits like the Employee Retention Credit injecting billions of dollars into the U.S. economy. Despite being an election year, the Federal Reserve has signaled that it will base its rate decisions solely on economic data rather than political calculations.

However, it’s important not to overstate the impact of elections on markets based on these data points alone. Underlying economic fundamentals like consumer spending, the labor market, earnings growth, and productivity gains tend to be more powerful drivers of stock returns over time. The rollout of artificial intelligence tools and their potential productivity benefits could be a strong tailwind for markets this year, regardless of the presidential election’s outcome.

Moreover, markets can certainly climb or sell off sharply in election years for reasons wholly separate from elections. For instance, the 2008 financial crisis triggered a major sell-off late in that election year, while the extraordinary stimulus response to the COVID-19 pandemic sent stocks soaring into year-end 2020 after the November election.

While elections tend to garner outsize attention, they are just one of many inputs for markets. Investors would be wise to look past the political noise and partisan narratives and remain focused on the fundamentals that drive long-term returns. Diversification, discipline, and sticking to your plan should be top priorities, regardless of who occupies the White House.

Q: Some economists are predicting a recession, and I’m in my early 60s. How could this impact my retirement?

The decision to retire is complex and personal, and even more so when the stock market is volatile and the economic climate is so uncertain. But all the planning you’ve done over the years, such as analyzing various scenarios with your financial advisor, will come to good use in these final years of your career.

Even if gloomy forecasts are making you feel anxious, one of the cardinal rules of investing is to stay invested. Remember: Market timing is a fool’s errand. You’d need to have access to a magic crystal ball—not just once, but twice—to be able to know just when to get out of the stock market and when to get back in.

Instead of doing anything drastic, consider taking these financial steps to best position your retirement plan in case of a recession.

Take stock of your financial plan. Revisiting and updating your projected household expenses is paramount. That way, you’ll have a thorough understanding of the income needs from your portfolio.

You should also work with your financial planner to test the resilience of your nest egg against market fluctuations by rerunning projections and layering on several different what-if scenarios.

Calculate your cash cushion. The amount you need is based on personal preference. Building your portfolio buckets may help you become comfortable with the amount of cash you should hold. We recommend keeping about a year’s worth of expenses in cash as an emergency reserve. As you approach retirement, it can make sense to increase this amount, depending on your other sources of retirement income.

Recessions normally don’t last longer than a year. Having a cushion will insulate you from being forced to sell equities in a falling market.

Use tax-loss harvesting. With taxable accounts, it’s always prudent tax planning to be proactive about realizing any capital losses. They can be used to reduce your tax bill by offsetting previously realized gains. Anything you can do to give yourself an edge will help in the long run.

As always, you should speak with your financial and tax advisors about your personal financial situation before you make any decisions. If you don’t have a thorough financial plan that addresses your retirement under various market and economic conditions, now is a good time to consider one.