But one day in 2006, Niewolny looked out of his office window from a skyscraper with a view of Lake Michigan and said to himself, “There has to be more to life than this.” Despite his success, he felt empty inside. The thought occurred to him: “If I died today, so what?” He realized he wouldn’t leave a legacy that mattered.

During that period, which he calls the season of “smoldering discontent,” Niewolny reevaluated his life, searching for new passions and ways to give back. He used ideas outlined by Bob Buford in his book Halftime: Moving from Success to Significance. Buford founded the Halftime Institute, a nonprofit organization that helps successful men and women create new lives defined by joy, impact, and balance.

As part of his journey to creating a lasting legacy, Niewolny went on a church mission trip to Africa, where he saw people who had very little but were far happier than he was. When he came back, he and his wife decided to sell their boat, plane, several houses, and other luxuries that he thought would bring him joy and happiness but gave him more headaches than anything else.

The couple used some of the proceeds to start an orphanage in South Africa. “So much joy came out of that,” he says. “That was the first time I realized when I took the focus off myself and put the focus on others, I had incredible joy and balance in my life.”

Niewolny says the purpose and passion for the second half of his life is giving back to those in need and making a difference in other people’s lives. At 54, he’s chief executive officer of the Halftime Institute and author of the new book, Trade Up: How to Move from Just Making Money to Making a Difference.

Finding Purpose

Psychologists say many people hit the pause button at some point during their lives to search for a deeper meaning and purpose. Despite the stereotypes about midlife crises, this pause-and-reset can happen at any age, from a person’s early 20s to retirement, and beyond. And it can be a challenging phase to move through.

The good news is that reevaluation often leads to a better life. In fact, studies show that meaningful activities—things that demonstrate and develop your abilities while also making a positive difference to others—can contribute significantly to your overall sense of happiness.

But what role does money play in happiness? Additional research suggests that money correlates with satisfaction only up to a point. Beyond that threshold, the correlation falls apart, and additional income no longer means additional happiness, says Frank Farley, a psychologist with Temple University in Philadelphia and a former president of the American Psychological Association.

“If you’ve been doing the same gig for decades, and you are highly successful, you may want to ask yourself: ‘How many more money mountains are there to climb? How many successes do I need to chalk up?’ It may be time to look for new venues in your life,” Farley says. That’s where generosity comes in.

The G Factor

When reevaluating their life’s purpose, many folks decide they want to give back. “I have been studying human motivation for decades, and I’m often asked what is on the top of the list of great human motives,” says Farley. “I answer generosity, which I call the ‘G factor.’ Generosity—the giving instinct—is so profound.”

Janet Karzmark, a life coach in San Jose, California, echoes Farley’s point. Giving goes hand in hand with compassion, she says, and most people feel a strong sense of compassion for those in need.

Successful people who have been busy striving and accomplishing things for most of their lives may not have had time to explore the compassionate part of their personalities. But if they volunteer for a humanitarian crisis or get involved in other important causes, their lives feel more complete and more purposeful, she says.

“You don’t want to face your death and think, ‘Oh, I missed that part of my life. I never got around to that.’ You don’t want to face that regret,” says Karzmark.

Giving back or serving others doesn’t mean you have to quit your job though. There are plenty of ways to make a difference with only an hour or two a week. For instance, Niewolny says he knew an executive colleague who volunteered to rock newborn babies of drug-addicted parents and found great meaning and joy in that simple act.

Organizations like VolunteerMatch and Charity Navigator make it easier than ever to find volunteer opportunities in your local community.

For many people, using their time and talents in their own sphere of influence is key to finding personal significance. That was the case for Alan Smith, president and chief executive officer of Rockcliff Energy, an oil and gas company in Houston, Texas. For years, Smith says, “I was so busy that I felt like I was drowning.”

To change his trajectory, Smith carved out more time in his life by stepping off several charity and industry boards. He also decided to narrow his focus to helping only a few organizations and a few other people in his network reach their full potential.

Now, Smith is a mentor and serves on the board of directors for the Texas Hearing Institute, a nonprofit pediatric hearing loss organization that provides therapy, education, and support services to children and families affected by hearing loss.

This cause has a special place in his heart because one of his daughters was born deaf. However, after receiving cochlear implants and help from the center, she is now able to hear. “The center had a huge impact on her life,” Smith says. Working on their board is one of the ways he gives back.

For Smith, reevaluating his lifetime legacy meant reprioritizing and staying focused. “You have a finite amount of time on earth, and you’ve been given many gifts and talents,” he says. “It’s a matter of being more intentional and figuring out how you are going to use them.”

How to Restart

There are several ways to begin the journey toward finding your purpose and creating a legacy you are proud of, says Niewolny. First, he says, start with the end in mind.

To do that, Niewolny describes an exercise he calls “the 80th birthday party.” Here’s how it works. Imagine you’re having a big birthday party with all your friends and family in attendance. Using a microphone in the room, the guests will recap your role in their lives. Write down what you hope they’ll say.

Also, write down the answer to these questions:

- What is your pursuit of success costing you?

- What in your life has the greatest value, and what are you doing to protect it?

- If you were to reorder your priorities in life to finish well, what evidence would confirm that you were on the right track?

Another approach is to ask yourself: If you were living a perfect life two years from now, what would that look like? Not what would you be doing, but what would it look like? Describe the scene in vivid detail.

For Niewolny, he wants his wife to flourish and for their marriage to be a priority. He wants his children to have high self-esteem. And he’d like everyone in his family to be in good health.

While it’s common for people to desire change, it’s difficult to shift the course of your legacy all on your own, says Niewolny. Some people benefit from an accountability partner, whether that means a certified life coach, spouse, mentor, friend, neighbor, or colleague. You might also consider multiple coaches.

Tell these people what you want from your life and let them hold you accountable for progress. “There is a reason why the best athletes in the world have coaches even though they may be at the top of their game,” says Niewolny. Coaches provide motivation and support when you need it most.

On a Mission

Figuring out your personal mission in life and acting on it can be life-changing, says Fielding Miller, CAPTRUST co-founder and chief executive officer. He speaks from experience.

During the first half of his life, Miller says he set a hectic pace, trying to raise a family, build a business, stay involved in the community, and maintain an active social life. “My time was overly weighted toward work. I was a complete workaholic,” he says.

Like Niewolny, at age 40, Miller discovered Halftime, which prompted him to reassess his values, aspirations, talents, and relationships. He started thinking about what he wanted for his family—and what he wanted from his own life. One idea from the book especially resonated with him: “What will I do about what I believe?”

The result of that period of introspection was “a total heart change, an epiphany moment,” Miller says. He reevaluated why he was working and reprioritized the things that matter most to him, focusing on his personal endgame—what would matter when his career was over.

It didn’t take long for this new mentality to bear fruit. Gradually, Miller says, he began to look at everything through a new lens. He made decisions and approached relationships differently.

“My personal mission is to live a life that is pleasing to God by being significant in the lives I touch,” Miller says. “I would like to be remembered for fulfilling my mission.”

And it’s never too late, or too early, to decide what that mission will be.

401(k) and 403(b) Fee Cases Continue

The flow of cases alleging fiduciary breaches through the overpayment of fees and the retention of underperforming investments in 401(k) and 403(b) plans continues but without significant new developments. Here are a few updates.

- In the past quarter, at least 20 court decisions were issued on motions to dismiss fees lawsuits.

- A slight majority of cases were dismissed: nine vs. eight, with another three being partially dismissed.

- To avoid dismissal, some courts require a complaint to include facts that plausibly allege a fiduciary breach occurred, while other courts require only allegations that support the possibility a fiduciary breach occurred. Courts applying the plausibility standard are more likely to dismiss cases. Whether cases are dismissed or allowed to proceed seems to depend considerably on where they are filed.

- Quotes and highlights from recent cases help tell the story:

- The allegation that all recordkeepers offer the same or similar services “defies common sense.” Krutchen v. Ricoh USA Inc. (E.D. PA 2023).

- The court could not conclude that the plan fiduciaries had a sound investment review process in place, so the case will proceed to trial. Jacobs v. Verizon Communications Inc. (S.D. NY 2023).

- Refusing to allow the filing of a new complaint in a case that had already been dismissed because it lacked sufficient grounds to proceed, the court said: “The case appears be a lawsuit in search of a theory. … Plaintiffs identify ways in which plan management could be different, or even improved, but they have not alleged facts to support a plausible inference that the defendants have failed as fiduciaries.” Wilcox v. Georgetown University (D. DC 2023).

- One settlement was approved. The plan had assets of approximately $400 million in 2020, and the suit was settled for $990,000, with $330,000 going to the plaintiffs’ lawyers. This represented approximately $65 per participant. The judge reduced the requested fee of $10,000 per named participant to $7,500. Dover v. Yanfeng United States Auto Interior Sys (E.D. MI 2023).

- We previously reported on Hughes v. Northwestern University, in which the Supreme Court reversed dismissal of a fees case and sent it back to the lower courts. Following the Supreme Court’s guidance, the U.S. Court of Appeals for the Seventh Circuit found that the complaint in that case includes sufficient allegations to avoid dismissal. The Seventh Circuit is one of the jurisdictions that requires allegations supporting a plausible—not just a possible—fiduciary breach. Hughes v. Northwestern University (7th Cir. 2023).

- Last quarter we reported on a Connecticut case permitting a jury trial on some ERISA fiduciary claims. A recent press report indicates that a settlement has been reached in that case. In another decision from the district court in Connecticut, a judge denied a motion to strike a jury demand, apparently permitting a jury trial. Vellali v. Yale University (D. CT 2023). It will be interesting to see if the possibility of a jury trial hastens a settlement in this case.

Use of Participant Account Forfeitures: New IRS Proposed Regulations

Many plans include a provision that if a plan participant terminates employment before being fully vested in their employer contributions, the nonvested portion will be forfeited. Participants are always fully vested in their own deferrals. It has been generally understood that forfeitures could be used to do any of the following:

- Pay permissible, reasonable plan expenses,

- Offset future employer contributions,

- Restore previously forfeited participant accounts, or

- Increase participant accounts.

Under the new proposed regulation:

- All forfeitures must be used no later than 12 months after the end of the plan year in which the forfeitures were incurred.

- As a transition rule, all forfeitures occurring before 2024 will be treated as occurring during the 2024 plan year and so must be used by the end of the 2025 plan year.

The proposed regulation also includes a provision that defined benefit plan forfeitures cannot be used to reduce required employer contributions.

Fiduciaries should receive and review regular annualized reporting on plan forfeitures from their recordkeepers to monitor this issue.

No Good Deed Goes Unpunished: 1947 Pension Trust Creates $38 Million ERISA Liability

In 1947, Mary Chichester du Pont—one of America’s richest matriarchs and part of the DuPont chemical company—created an employee pension trust to support domestic employees and those who provided secretarial, accounting, or other assistance to du Pont family members. The trust was intended to pay an annual pension equal to 60 percent of wages to those with at least 10 years of service. Each family member with covered employees was defined as a qualified employer. The trust was funded with 50 shares of DuPont stock, which had grown to 112,772 shares in 1999, worth about $7.4 million at that time. The trust has current assets of about $2.7 million.

In 2015, two of Ms. du Pont’s grandchildren contended that their domestic employees are entitled to benefits under the trust, and a dispute arose. This brought into clear focus whether the 1947 arrangement falls under ERISA, which was passed in 1974. It does. There is no exception for programs that preexisted ERISA. In the years before the dispute arose, administrators and trustees received conflicting opinions on whether ERISA applied, but they took no action to resolve the issue.

As would be expected, the fallout of the court’s finding that ERISA applies is considerable. A recent decision finds:

- The plan trustee and all du Pont family members with employee-participants in the program are considered plan fiduciaries.

- All plan fiduciaries have breached their duties under ERISA in a variety of ways.

- There are currently 246 known potential plan participants and beneficiaries to whom liabilities are owed—active, terminated, or retired. All employees of all qualified employers are eligible for benefits under the terms of the trust.

- The trust’s liabilities are $37 million to $38 million. Current assets are $2.7 million.

- The plan must be immediately funded under ERISA’s funding requirements.

- All plan fiduciaries are jointly and severally liable for all the plan’s liabilities. That is, each fiduciary is fully liable for the entire amount.

Given the complexities, the judge has appointed a special master—an independent businessperson or lawyer—to hold the defendants’ feet to the fire and report back to the judge. The special master and all providers the special master hires will be paid by the plan fiduciaries, with an initial retainer of $100,000. Wright v. Elton Corporation (D. DE 2023).

This case is a good reminder that benefits provided by employers to employees may be covered by ERISA even if that is not immediately apparent. It is also a reminder that problems do not age well.

Oops! Board Action Alone Did Not Terminate Severance Plan

A company’s employee benefit program included a severance plan. With layoffs pending, the company decided to terminate its severance plan and eliminate those costs. Prior to the implementation of planned layoffs, the company’s board of directors adopted a resolution terminating the severance plan. Disappointed employees who had been laid off sued, claiming they were entitled to severance plan benefits.

The severance plan was set out in full in the company’s employee handbook, and the company clearly retained the right to eliminate benefits. However, the handbook also said that action by the human resources (HR) department was required to modify the handbook. The district court found that the board of directors’ resolution terminated the severance plan as an act of the company and denied benefits to the laid-off employees.

The court of appeals found that the board action alone was not enough to terminate the severance plan. As prescribed in the employee handbook, action by the HR department—in writing—was required. Not requiring HR department action would effectively delete that provision, which the district court was not permitted do. Messer v. Bristol Compressors International LLC (4th Cir. 2023).

DOL Weighs In on Supplemental Life Insurance: Evidence of Insurability

We have previously reported on situations in which employees intended to enroll in supplemental life insurance coverage but did not complete evidence of insurability (EOI) requirements. Then, upon the death of the insured, and to the surprise of survivors, coverage was denied even though premiums for the coverage had been paid. The insurer would typically return these premiums.

Following an investigation, the U.S. Department of Labor (DOL) announced a settlement with Prudential Insurance Company of America on denials of supplemental life insurance coverage due to lack of EOI. The investigation found that even though premiums were collected for extended periods, numerous claims were denied because EOI had not been provided. From 2017 to 2020, more than 200 claims were denied on this basis. The investigation also showed that premiums had been collected back as far as 2004, even though EOI was not in place.

According to the DOL’s settlement news release:

- Prudential will not deny coverage based only on lack of EOI if it has received at least three months of premiums.

- People who are currently insured by Prudential cannot be denied coverage based on EOI more than a year after they started paying premiums or based on evidence that they were no longer insurable after first making premium payments.

- Prudential will reprocess claims back to 2019 and pay benefits that were previously denied based solely on lack of EOI.

- A parallel investigation into other insurers found similar practices. DOL Assistant Secretary for Employee Benefits Security Lisa Gomez said that the DOL will take appropriate action against other insurers who “play a game of gotcha to wrongfully deny benefits based on technicalities.”

- Group policyholders, like employer plan sponsors, who collect premiums may be liable for supplemental life insurance claims by beneficiaries if they failed to notify participants that Prudential had not approved their EOI.

Plan sponsors should work with their insurers or other providers to confirm that appropriate processes are in place to avoid issues like these.

Beneficiary/Slayer Denied Retirement Plan Benefits

Most states have a so-called slayer statute, which prevents murderers from benefiting from their crimes. In a recent Oregon case, a provision of this type was applied—with a twist. Tracy Cloud was convicted by a jury of murdering her husband, Philip Cloud. Although Tracy claimed self-defense, the evidence did not support her case, and there were financial incentives for the murder.

Philip was an employee of Intel Corporation and participated in Intel’s retirement plans. Tracy was his beneficiary. Soon after Tracy was convicted, the executor of Philip’s estate filed a suit to prevent Tracy from receiving the benefits from Philip’s plan accounts, and rather to disburse those funds to the estate.

Tracy objected on the grounds that an appeal of her murder conviction is pending. The district court acknowledged that disposition of Philip’s retirement plan benefits would depend on the outcome of Tracy’s appeal and stayed, or suspended, the case until the appeal is decided. Munger v. Intel Corporation (D. OR 2023).

Bill Hoover, chief financial officer at Hillcrest Convalescent Center in Durham, North Carolina, has always had an open-door policy. Twelve years ago, when he started at the company, that policy helped him get to know his colleagues and respond to their concerns. But as Hillcrest grew to nearly 500 employees, Hoover found it challenging to keep on top of all of his many responsibilities while maintaining the open-door policy that was so important to him.

Among the many responsibilities competing for Hoover’s time and attention was his responsibility to monitor the company’s 401(k). Although he never missed a meeting with his plan advisor, scheduling became increasingly difficult, and he found himself consistently agreeing with his advisor’s every recommendation. This made him wonder if there wasn’t a better way.

Hoover recognized how important it was for his team to lean on experts for guidance. He also wanted to win back some of his own time to focus on other aspects of the business. With those two things in mind, he decided to transition Hillcrest to a 3(38) investment management arrangement.

A 3(38) arrangement gets its name from the relevant Employee Retirement Income Security Act of 1974 (ERISA) section that defines it. In brief, a 3(38) arrangement is a way of outsourcing the burden of investment decision-making—and risk—to a qualified expert. 3(38) investment managers are a distinct breed of fiduciaries legally required to act in their clients’ best interests when it comes to choosing funds and managing assets. Their job is to select, monitor, and benchmark retirement plan investments on a discretionary basis. And they’re experts at doing so.

Smart Outsourcing

Investment advisors registered under the Investment Advisers Act of 1940 have long assumed this role for defined benefit pension plans. But increasingly, 3(38) relationships are being extended to defined contribution plans too, primarily 401(k)s and 403(b)s.

There is good reasoning behind this choice, says Jennifer Doss, senior director of CAPTRUST’s defined contribution practice. Doss says an uptick in litigation regarding defined contribution plans has led to increased industry demand for 3(38) relationships.

“A 3(38) arrangement represents the highest level of investment liability transfer possible under ERISA today,” says Doss. “It’s pretty easy to see why there’s demand in the industry for this kind of fiduciary.”

Benefits attorney Mark Grushkin agrees. He has seen many defined contribution plan committees receive materials for approval right before a meeting and then rubber stamp whatever they get from their investment advisor.

That’s partly because very few people have the requisite expertise to confidently make these investment decisions. “There may be one person—maybe the CEO—with some financial acumen,” Grushkin says. “But that doesn’t make them an expert in investing. And for those folks, I think [using a 3(38) is] really important.” With the “virtual explosion of ERISA litigation,” he’s noticed, “Why not offload as much fiduciary responsibility as possible?”

There’s also the appeal of unburdening overworked executives by having someone else manage plan investments. “If you’re a smaller partnership or mid-size enterprise, one of the things you value most is time,” says Scott Matheson, managing director of the institutional group at CAPTRUST. For example, the business officer at a school is not only making sure everyone’s benefits are in order but also running the line for carpool. “Reducing the amount of time spent on retirement plan meetings and follow-ups is a real, tangible benefit.” says Matheson.

The time savings was a big draw for Bill Hoover at Hillcrest. “We were a smaller company, and we liked to have control and have our hands in everything,” he says. “But as we started to grow, we realized we needed to focus on growth and put investment decisions in the hands of experts.”

Faster Changes, Better Outcomes

Smaller companies are happy to reclaim time, and larger companies are often glad to unload some of the risks that aren’t core to their businesses. But any size company is pleased when its investments achieve better outcomes.

“Committee members wear lots of hats, so getting all the decisionmakers in the same room can be difficult,” says John Leissner, CAPTRUST head of institutional client service and operations. “Considering the time needed to adequately discuss fund changes, the timeliness of these changes can pretty easily be negatively impacted.”

With a 3(38) arrangement, fund changes can happen more quickly. They no longer require companies to spend time scheduling and holding committee meetings or researching and debating proposed changes. And with quicker fund changes come compounding returns and better retirement results for employees, explains Leissner.

Reducing the expenses and logistics of plan committee meetings are additional benefits. Financial advisors at CAPTRUST have witnessed plan sponsors in a 3(38) capacity lowering company expenses by having fewer meetings. These meetings can quickly become expensive when accounting for travel costs, lost billable hours, and expert fees. One advisor reported that a plan sponsor was able to reduce its committee size from eight to two and switch from quarterly to semiannual meetings, thereby reducing costs significantly.

For many plan sponsors, committee meetings—previously filled with discussions about managing investments and selecting funds—have shifted. Now, they’re more focused on participant engagement, plan design, optimization of retirement plan vendor offerings, and the fiduciary process. Advisors have also witnessed plan sponsors with a 3(38) relationship being able to spend more time on participant financial wellness, retirement readiness, and overall plan satisfaction.

“The committee spends much less time talking about the individual investment options, freeing up time for more meaningful discussions about helping their employees build a solid retirement plan,” says one CAPTRUST advisor.

The Phew Factor

What’s the biggest motivator for plan sponsors to engage in a 3(38) arrangement? At first glance, it may seem like plan sponsors would want to reduce fiduciary risk. But surprisingly, many sponsors report that relief from worry was their major incentive.

“While we felt that plan sponsors would be relieved about taking on less risk as fiduciaries upon hiring a 3(38), we didn’t realize that this typically results in committee members experiencing less worry and stress related to plan decisions,” says Leissner. “We realized committee members actually felt emotionally relieved to not have to make these decisions.”

For Hoover, switching to 3(38) had just that effect. “The financial world is a crazy world out there, and unless you’re in it every day and know what you’re looking at, it can be overwhelming,” he says. “It takes a lot of weight off my shoulders and my business partners’ shoulders to know we can focus on our employees, on our business, on our growth, and know that experts are handling our 401(k).”

He’s certainly not alone. Doss says that some plan sponsors may not have fully understood the liability they were accepting in their prior 3(21) advisory arrangement—a relationship that allows a fiduciary to advise the committee but not execute decisions on its behalf. After working under a 3(21) arrangement for a period of time, a 3(38) arrangement felt much more appealing.

“A lot of committee members are very happy to relieve themselves of that responsibility, understanding they do not really have the requisite knowledge base,” Hoover says. Or as one CAPTRUST advisor explains it, the feeling his clients experience as part of a 3(38) arrangement could be called the phew factor: a sense of safety and relief.

Letting Go of the Reins

One of the primary reasons why companies might choose not to pursue a 3(38) arrangement: fear of giving up control. Often, plan sponsors say they’re comfortable where they are, often with a 3(21) relationship. Or they don’t feel comfortable handing over the reins to someone else. “Some folks want to stay involved in the decision-making process and don’t want to feel out of the loop or caught off guard by changes being made to the plan,” explains Doss.

Certainly, a 3(38) arrangement is not the right choice for every plan sponsor. For Grushkin, the benefits attorney, it comes down to the aptitude and availability of committee members. For CAPTRUST’s Matheson, it’s about culture. “If you’re an organization that likes to be involved in all the gory details, then don’t turn over the keys,” he says.

But surprisingly, even plan sponsors who were once hesitant to give up control said moving to a 3(38) arrangement did not leave them craving their old responsibilities. “They are not burdened with making difficult decisions, they have time for more dialogue about participant outcomes and plan competitiveness compared to peers in industry, and the fund change process is streamlined with minimal involvement,” says Leissner.

Given all those positives, and the draw on resources they had with previous arrangements, “It makes sense to us that the plan sponsor’s emotional ties to the process are something that they can let go of a little more quickly than they had anticipated,” he says.

Hoover was not disappointed when he switched to a 3(38) arrangement. The time saved, the risk transferred, and the improved outcomes all left him satisfied with his decision to make the change. In fact, Hoover says Hillcrest’s competitive 401(k) is a big selling point in the recruitment process, and one that gets used to attract top talent.

Hoover says the switch to a 3(38) relationship has been successful because it is something he doesn’t have to think about.

And, surprisingly for him, using a 3(38) has allowed him to focus his scarce time and attention on other pressing matters, like helping Hillcrest employees get in the plan and save enough for a comfortable retirement. “The fact that we have an advisor picking the funds for them, not only does it help me sleep better, but it takes away a negative,” he says. “There are much more important things for me to focus on.”

With confidence bolstered by a tight labor market and strong consumer spending, throughout the first quarter of 2023, the U.S. Federal Reserve continued to communicate a steadfast commitment to bring down inflation. This signaled to markets that interest rates are likely to move higher and stay high for longer, thereby increasing the risk of a policy-induced recession.

Meanwhile, fractures emerged within the U.S. banking system due, in part, to the speed and magnitude of rate hikes so far. These events hold the potential to dampen future growth if they lead to tighter lending conditions.

Nevertheless, equity investors seemed to shrug off these concerns in the first quarter. Stock markets have been surprisingly calm. The S&P 500 Index enjoyed its best January since 2019, while the tech-heavy Nasdaq Index posted its best start to the year since 2001. Despite the dramatic rise in interest rates and the banking scare, the S&P 500 is still trading at more than 18 times earnings.

But all is not quite so calm in the bond markets, where a significant disconnect has appeared. The Fed is still in tightening mode, worrying over persistent inflation, while the bond market is signaling concerns about economic slowdown and the risks of recession. This ongoing clash will likely be the key story throughout 2023, with consequences for both the markets and the economy.

Figure One: First Quarter Recap—A Glimmer of Good News

Asset class returns are represented by the following indexes: Bloomberg U.S. Aggregate Bond Index (U.S. bonds), S&P 500 Index (U.S. large-cap stocks), Russell 2000® (U.S. small-cap stocks), MSCI EAFE Index (international developed market stocks), MSCI Emerging Market Index (emerging market stocks), Dow Jones U.S. Real Estate Index (real estate), and Bloomberg Commodity Index (commodities).

In stark contrast to last year’s losses, most major asset classes delivered positive returns for the quarter, led by international market stocks with high single-digit returns, aided by the weakening dollar. Within the U.S., the financial sector faced stiff headwinds and investors reacted to banking stress by rotating back to the comfort of mega-cap technology companies with fortress balance sheets and strong cash flows.

U.S. bonds also rebounded from last year’s painful losses, with a total return of 3 percent.

The standout performer of 2022, commodities were the only major asset class to experience negative returns, driven by declining energy prices fueled by fears that a slowing economy would reduce oil demand. The OPEC+ organization of oil-producing countries reacted by cutting production targets to raise prices. With U.S. shale production lagging due to higher financing costs and an uncertain regulatory environment, and with the Strategic Petroleum Reserve at its lowest level since the 1980s, the U.S. will now have fewer tools in its arsenal to rein in higher energy prices, which could contribute to lingering inflation.

Growth Conditions Persist

Global growth remained strong during the first quarter, providing bullish investors ample evidence of the potential for an economic soft landing. Consumers benefitted from a tight labor market and lower energy prices, while the pandemic reopening of China strengthened global growth conditions through higher domestic demand for goods and commodities. The rebound in U.S. and European purchasing managers’ index (PMI) survey data during the quarter also reflects improved global growth conditions.

Consumer purchasing power has also improved, as the prices of key items such as groceries and gasoline receded from their 2022 peaks. As shown in Figure Two, consumer sentiment—a key driver of consumer spending behavior—has also rebounded significantly from its all-time low in June 2022 as food and energy prices eased.

Figure Two: Consumer Sentiment and Food and Energy Prices (2022-2023)

Source: Federal Reserve Bank of St. Louis

While savings rates have declined and credit card balances have grown, economists estimate that consumers still hold approximately $1 trillion of excess savings accumulated during the pandemic that can continue to fuel consumer spending. According to Federal Reserve data, overall household financial obligations, including debt, leases, property taxes, and rents, also remain low relative to levels of disposable personal income.

By driving wages higher, the robust labor market has also contributed to consumer confidence and spending. Although tight labor conditions may be a thorn in the Fed’s side as it seeks to control inflation, these conditions continue to support economic activity. Even so, workers have struggled to keep pace with rising prices. March 2023 was the 23rd consecutive month when wage growth failed to keep pace with inflation, a sign of weaker bargaining power among the workforce that may suggest less risk of a wage-price inflation spiral.

Mixed Progress on Inflation

The strength of the labor market provides room for the Fed to continue its aggressive inflation-fighting campaign. Since 1970, there has not been a recession with the unemployment rate at its current level of 3.5 percent. The Fed views price stability as a prerequisite for an economy that works for everyone, and over the past year, it has acted forcefully to attain this objective, raising the fed funds rate nine times from 0 to 4.75 percent.

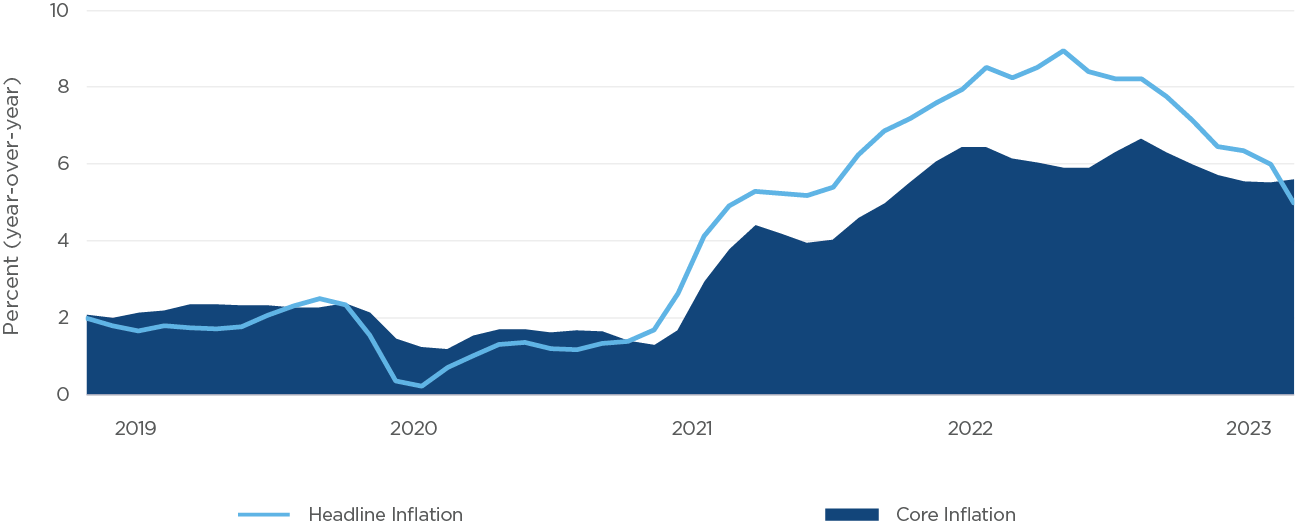

The March Consumer Price Index (CPI) showed mixed results toward this objective. The combination of higher interest rates, tighter lending standards from banks, and consumer spending behavior brought headline inflation down to a year-over-year level of 5 percent. While this is still far above the Fed’s 2-percent target, it shows significant progress relative to the 9 percent level seen last summer.

Headline inflation encapsulates a wide range of goods and services, and its return to levels not seen in nearly two years is good news. However, as shown in Figure Three, another closely watched measure called core inflation increased slightly in March. By excluding some of the most volatile categories, such as energy and food, core inflation is considered by many as a more reliable indicator for predicting future inflation trends than headline inflation. If its downward progress stalls or levels out, this could be a sign of inflation that risks becoming entrenched.

Figure Three: Core vs. Headline Inflation (Mid-2019 to Present)

Source: U.S. Bureau of Labor Statistics

A Banking Tremor (Not a Crisis)

In light of this combination—a strong labor market and sticky inflation—the Fed continues to signal that additional rate hikes lay ahead. Notes from its March meeting suggest that virtually all committee members expect the fed funds rate to rise to at least 5.1 percent, which would suggest at least one more rate hike at its May meeting, after which rates would likely remain steady through year-end. The Fed is reluctant to reverse course too soon, which could allow inflation to regain its footing.

It is often said that, when trying to fight inflation, the Fed raises rates until something breaks. Yet, in addition to managing inflation, the Fed is also charged with maintaining financial stability. The challenge of balancing these two objectives came into clear view throughout March, after a bank run led to the second largest bank failure in U.S. history. This was followed by a second collapse soon after.

The root cause of these isolated collapses goes back to the pandemic, when households were flush with cash and interest rates were extraordinarily low. Bank deposits swelled, so banks did what they always do: They looked for ways to earn money on those deposits. To earn a greater net interest margin—the difference between deposit rates and what the bank can earn on its securities and loan portfolio—they loaded up on bonds.

But, as interest rates rapidly rose, those bonds declined in value. At the same time, rising interest rates made alternatives to bank deposits, such as money market funds or Treasury bills, more attractive to bank clients. As depositors withdrew funds from banks to take advantage of higher yields, banks were forced to sell securities at a loss, negatively impacting bank capital levels and liquidity.

To keep these isolated cases from causing stress on the larger financial system, the Fed stepped in, providing liquidity to banks through a new program called the Bank Term Funding Program. In effect, the Fed was helping to address the very problem it created—acting as both the arsonist and the firefighter.

These bank failures were isolated and idiosyncratic, but stresses within the banking system represent a form of tightening financial conditions that will either make the Fed’s job easier or risk pushing the economy into recession. In the week following these regional bank failures, consumers withdrew more than $180 billion from small banks—the largest weekly deposit decline of the last 20 years. Declines in deposit balances could leave small and midsize banks vulnerable, leading to tighter lending conditions particularly for real estate and small business loans.

Earnings Pressures

Historically, recessions have always coincided with a decline in corporate earnings. According to FactSet, earnings for the S&P 500 companies fell by nearly 5 percent in the fourth quarter of 2022 and are expected to have fallen by another 6.8 percent in the first quarter of 2023. If FactSet’s estimate proves to be true, this would mark the largest decline in earnings since early 2020.

Corporate profit margins are under pressure on several fronts. Companies face rising labor and input costs, greater scrutiny of supply chains, rising inventories as pandemic-driven demand slows, and importantly, rising financing costs. For companies and industries calibrated to the extraordinarily low interest rates of the past decade, moving to more historically normal interest rate levels will be a difficult transition.

Debt Ceiling Drama

An important deadline looms in mid- to late summer: the need for Congress to raise the U.S. debt limit. The U.S. debt ceiling represents the cap on the amount of money that the Treasury can owe before it risks a default on its debt. Congress has raised the debt ceiling 78 times since 1960, typically without fanfare.

Not raising the debt limit and defaulting on U.S. obligations would have devastating economic implications. As Treasury Secretary Janet Yellen recently told lawmakers, global confidence in the U.S. government to reliably pay its bills is the cornerstone of what makes the U.S. economy the soundest and best in the world.

With such serious consequences, the debt ceiling problem is likely to be solved. However, given the high degree of political polarization and the tight margins between political parties in Congress, reaching an agreement could be difficult and holds the potential to inject volatility into markets. Outside the U.S., the geopolitical landscape also remains challenging, with no end in sight for the war in Ukraine, escalating tensions between the U.S. and China, and more recently, the leak of top-secret Pentagon documents that reveal intelligence on adversaries, competitors, and key partners.

The Fog of Data

As the Federal Reserve ponders the forward path of interest rates, it has reiterated its dependence on data to guide its course. In this especially unpredictable environment, investors cling to every piece of new data, examining each detail through the lens of the Fed to determine if it’s good or bad news.

For much of 2022, the market’s expectations and the Fed’s own projections were tightly aligned. However, the two began to diverge late in the year. The Fed continued to emphasize its higher-for-longer stance, while markets envisioned a faster pivot, sending rate expectations lower. This difference of opinion will likely be a key driver of market behavior for the remainder of 2023.

For investors, there are several key points to remember in this type of environment. First, don’t be lulled into complacency by the orderly returns we saw in the first quarter. While prices and valuations suggest that calm has been restored to markets, powerful forces are still at work, promising a suspenseful and eventful remainder of the year.

Also, in choppy, directionless markets, income from dividends or coupons becomes an even more important source of total return. For long-term investors, this is a reminder that being aware of the environment does not mean reacting to every headline that crosses the screen.

Plan sponsors have long understood that not all participants have the same needs when it comes to retirement planning. For example, a 28-year-old who earns $60,000 a year and is paying off student loan debt may be looking for different features than a 58-year-old who earns four times that amount and is preparing to retire. Yet only recently have plan sponsors gained access to tools that can help them personalize their offerings in ways that account for demographic differences beyond age and income. If thoughtfully and intentionally designed, it’s possible that employer-sponsored plans can narrow the gaps in financial wellness and retirement readiness across diverse populations.

Women and people of color, for instance, face multiple challenges in building retirement wealth, primarily because of income inequality. On average, women are paid 83 percent of what men are paid, hold only 32 percent of the wealth that men have accumulated, and receive 70 percent of what men receive in retirement income, according to the American Association of University Women.The data regarding Black and Latino workers is even more striking. In 2020, the New York Times reported that Black men are paid only 51 percent of what White men are paid, and the median savings for Black and Latino families is less than a third of what their White, non-Hispanic colleagues have saved. These numbers show little progress toward pay equality since the 1950s. Over time, pay disparities—along with higher debt, shorter job tenure, and less financial acumen—take a serious toll on retirement outcomes.

But this isn’t the only reason plan sponsors are reacting. Combined data from the Bureau of Labor Statistics shows that women and people of color now comprise more than 63 percent of the American workforce.The country is on track to have a majority minority population by 2044, meaning that most Americans will identify as racial and ethnic minorities or as more than one race.

Whether motivated by demographic changes or moral imperative, plan sponsors are starting to explore which plan design elements and employee benefits may be most helpful in shrinking retirement disparities. Updating plan designs to support diverse employees is one way employers can stay competitive.

Personalizing Plan Design

Reshaping retirement plans to account for diversity is part of the larger trend toward personalized retirement benefits. Employers are no longer solving for the average. They are customizing their retirement offerings to account for a wide range of individual differences. To get a grasp on what participants want, sponsors first need to understand their unique employee demographics and ask about individual participants’ financial needs.

“The first step is often a data-finding mission,” says Scott Matheson, head of the institutional business at CAPTRUST. Via surveys and listening sessions, employers can look for trends to understand “which demographic groups benefit most from current plan design, who is not participating, and why.”

“The next step is to explore whether there are plan design elements that may support higher participation and savings rates across diverse demographics,” says Matheson. If there are, it can help to put changes in order of importance, moving those with the greatest potential impact to the front of the line.

For instance, plan sponsors might conduct a pay equity analysis. In general, plan participation increases with income. Because women and people of color are paid less than their White male counterparts, they are also less likely to participate when offered a retirement plan. What’s key is understanding why. When asked, both Black and women professionals cite three primary reasons: lower pay, higher debt, and competing financial duties.6 A pay equity analysis can help employers gain a clearer picture of their internal income disparities and start to understand how these differences may be contributing to plan participation and savings rates.

Auto Features and Eligibility

Although the industry is still learning which specific plan design features are most helpful, a few have already proven to boost financial outcomes for diverse workers. The first is employer matching—a powerful motivator for participation across nearly all demographics. CAPTRUST Financial Advisor Steve Wilt names two more: “If you want to increase participation, adding automatic features and lowering eligibility requirements can make a difference.”

The data regarding automatic features is especially strong. According to a recent Vanguard study, automatic enrollment can increase participation by 30 percent or more. And, when they are automatically enrolled, nearly 75 percent of participants remain invested in the default fund three years later.Wilt points out that “auto-enrollment may be particularly important for low-income Black and Hispanic workers.” With voluntary enrollment, these individuals participate in a defined contribution plan at 35 and 36 percent respectively. However, Wilt says, “With auto-enrollment in place, participation jumps to 93 and 94 percent respectively. That’s an astounding increase that may make auto-enrollment more attractive.”

But automatic enrollment does not necessarily reduce disparities in savings rates. While White and Asian employees are more likely to override default deferral rates and choose a higher one, Black and Latino populations do not generally respond the same way. As Mattheson says, “The employer’s default enrollment rate has a significant impact here. When employees are enrolled at low rates—like 3 percent—they may assume that 3 percent is sanctioned by the company as a sufficient savings rate. This can lead to lower savings rates and less total savings over time.”

This is where automatic escalation can make a positive difference, raising deferral rates across the board. Automatic escalation means increasing each participant’s contribution rate by a small percentage every year until the employee reaches a specified maximum rate. Under the SECURE 2.0 Act, auto-enrollment and auto-escalation are required for most new retirement plans, but existing plans may also want to consider adding these features. Those who do should carefully consider their default enrollment rate and rate of increase.

Plan sponsors might also consider lowering eligibility requirements. “Exactly how to lower eligibility will be different for every sponsor,” Wilt says. “Some may choose to allow part-time and seasonal workers to participate, while others may shift to immediate eligibility or shorter vesting periods.” SECURE 2.0 makes a change here too, specifying that long-term, part-time employees are eligible for plan participation if they have worked for the company at least 500 hours in two consecutive years.

Financial Wellness Programs

Another way plan sponsors are supporting diversity and inclusion is by investing in financial wellness programs. Studies show that diverse professionals face higher hurdles in achieving financial wellness due to differences in financial acumen and opportunity. Debra Gates, a CAPTRUST manager of financial wellness and advice, says financial wellness programs help people make more prudent decisions. “So many people have never learned the basics of financial literacy or personal finance,” she says.

Also, in some cultures, talking about money can be taboo. Nevertheless, individuals must make financial decisions every day. “Having to make decisions with limited knowledge can cause anxiety and stress, especially when those decisions are directly connected to a person’s financial future, such as whether to put money away in an employer-sponsored retirement plan, start an emergency fund, or create a budget,” says Gates.

A financial wellness program that targets a diverse demographic can not only expand employees’ knowledge but also instill confidence. Done well, financial wellness programs teach employees how to employ critical thinking skills to weigh outcomes, or at least be comfortable enough to discuss their financial goals with a trusted advisor.

But customized content needs to be thoughtful and intentional, which will help plan sponsors avoid stereotypical and tone-deaf mistakes. “Otherwise, you risk alienating the same people you are trying to include by making uninformed and potentially offensive assumptions,” says Gates. One way to do this is to include diverse perspectives in the content creation process. For instance, tap Spanish-speaking employees to help not only translate but also interpret English content into authentic Spanish-language materials.

“Start by having a conversation,” says Gates. “Find out who is not participating in the plan, and then take the time to ask them why. The barrier might be as simple as ‘I don’t understand how to sign up,’ or ‘I don’t know what this jargon means.’ It is easy to assume that some employees are not interested in participating, but by digging little deeper, plans sponsors can really understand the underlying issues and do something about them.” To understand which financial topics employees want to learn about, plan sponsors might consider sending a survey that lists potential topics, including debt management, credit management, market basics, investment strategy, education savings, and combining 401(k)s from multiple former employers.

As a best practice, sponsors should be prepared to use multiple forms of communication to promote wellness services and events, like short videos, emails, in-person or virtual meetings, and webinars. Wellness and enrollment materials should be accessible in multiple languages and, when possible, delivered on-demand for employees to watch, read, or listen to on their own schedules. It is also a good idea to tie educational content to specific participant actions, like deferral changes and investment advice.

Gates attributes the recent increase in financial wellness programs to the shifting relationship between employer and employee. “Employees expect and believe that it is the responsibility of their employer to provide solutions for financial, physical, and mental well-being. The expectation of the employer’s responsibility goes so far beyond where it used to be pre-COVID-19,” she says. “People do want to be paid well, but they also want to know that they are valued and respected.”

In sum, although DEI as an institutional practice is ever evolving, and DEI trends may shift in response to changing social or institutional circumstances, it seems that the principles of diversity, equity, and inclusion are here to stay. Employers who were early adopters of DEI strategies are now learning how to align their retirement plans and employee benefit packages to their DEI missions. Specifically, they’re doing so via plan design features and financial wellness.

Those who started a bit later can learn from these peers to create more robust, effective, and efficient retirement plans—plans that not only meet the needs of the modern workforce but also work to improve disparities and narrow existing gaps in retirement outcomes. Along the way, they’re also learning how to listen and respond to employees. They’re demonstrating a long-term commitment to employee wellness and creating trust that will carry them into the future.

Perhaps not surprisingly, the most significant trends in endowment management relate to fundraising, asset allocation, and spending. Specifically, endowment managers are showing increased interest in unrestricted gifts, alternative investments, the repositioning of fixed income portfolios, and conditional spending policies that account for inflation or market volatility. At the same time, endowment committees are grappling with questions related to environmental, social, and governance (ESG) investing and diversity, equity, and inclusion (DEI).

Although there are broad differences in strategy and tactics between smaller and larger endowments, as investment committees and institution leaders consider the best ways to move forward, it can be helpful to understand national trends in endowment management and the reasoning behind them. Tapping into peer thought processes can help endowment managers make more informed financial decisions.

Fundraising via Donor Education

In 2022, as pandemic concerns waned, many organizations returned to in-person fundraising events and increased their donor education efforts. This uptick in education efforts may be a response to market volatility and the financial challenges it has created or may be a sign that endowments are entering a new phase of donor relations.

Donors are no longer seen as one-time supporters but as active and engaged advocates for the institution. As CAPTRUST Principal and Financial Advisor Elliot Greenberg explains, “Maybe more than ever before, endowments and their donors are working together as partners for the long-term benefit of the organization.”

Endowment teams have gotten smarter about understanding what is attractive to donors, then teaching them the most efficient ways to donate for mutual benefit. Greenberg says, “Many endowments are actively reaching out to donors to say, ‘Your assets have appreciated, and that may cause a tax burden for you. If you’re philanthropically inclined, here are a few ways you might be able to lessen your tax burden and help our organization at the same time.’” Some endowments are even giving step-by-step instructions to help donors decide whether to donate cash vs. stock or donate at regular intervals vs. giving one big gift.

Endowments have also gotten better at explaining why the school itself is in the best position to decide how gifts should be spent. Over time, this may lead to a corresponding increase in unrestricted gifts. When donors understand that a gift will be prudently managed—and perhaps even grow—they feel better about making unrestricted donations.

Shifting Asset Allocations

Asset allocations are also evolving as endowment managers periodically reevaluate the best ways to protect perpetuity while supporting operational needs. Two key trends are an increased interest in alternative investments and a renewed focus on fixed income. Committee members are also starting to have more conversations about international equity.

As CAPTRUST Principal and Financial Advisor Chris Krakowski says, the interest in international equity has two likely drivers. “One is that stock valuations outside of the U.S. are currently on the lower end. The other is that the value of the dollar has begun to decline, which is a tailwind for international equities,” he says. Endowment managers don’t seem to be shifting their asset allocations outside of U.S. equities yet, but they are watching the trend and staying attuned to predictions.

However, many are making changes when it comes to alternative investments. In recent years, the nonprofit sector has gained easier direct access to private equity and private real estate and witnessed a corresponding uptick in allocation to those areas. Even smaller organizations are now educating their teams to understand the pros and cons of these investments. Fewer endowments are using a fund-of-fund structure, which often entails an added layer of fees, and more are working to identify what’s truly best in class.

“A lot of institutions lived through the pain of building up their private investment programs when public equity markets were the top-performing asset class,” says Krakowski. Now, investors are seeing some rewards for that pain, especially in the last year, when private investments outperformed most publicly traded assets. For some endowments, investing in alternatives has added to diversification and lowered the volatility of returns.

Endowments of all sizes are also taking a fresh look at fixed income and considering repositioning their portfolios. Since the 2008 financial crisis, the near-zero percent interest rate on bond investments has felt more like a parking lot than a long-term strategy for many endowment managers. Now, Greenberg says, “With increased inflation, higher education institutions still aren’t seeing significant real returns on their fixed income investments. But if inflation comes down, we may see fixed income get particularly interesting for endowments.” In the meantime, endowment managers are initiating the conversation with financial advisors and watching to see what happens with their returns.

Spending Policy Scenarios

Another area of evolution for higher education endowments is in spending policy design. To balance short-term goals with the need for intergenerational equity, most endowments spend between 4 and 5 percent of their total assets each year. Recently, however, endowment managers have been wrestling with the impact of inflation as rising costs and market volatility erode the value of their assets. As a result, many higher education institutions are taking a fresh look at their spending policies.

One strategy that is gaining traction is the creation of conditional spending policies, some of which tie endowment spending to specific metrics, such as inflation or the Consumer Price Index. By aligning spending needs with economic indicators, a policy that accounts for economic conditions can help an endowment support its institution in times of increased need. For instance, when inflation is higher, institutions may need to increase staff and teacher salaries and scholarship amounts. With a premeditated conditional policy in hand, the school may have more flexibility to tap endowment assets to meet those needs.

At the same time, these policies can create a disconnect between spending and institutional assets. “A policy that accounts for inflation can lead endowments to increase spending while the value of their assets is down,” says Krakowski. Depending on the institution’s needs, goals, and vulnerabilities, that can be a benefit or a boon.

“There is no right or wrong answer to conditional spending policy design,” Krakowski says. “What’s key is understanding and balancing the organization’s current operating needs with the traditional goal of ensuring perpetuity.”

Regardless, after the challenges of the past three years, this may be a good time for organizations to reconsider or reaffirm their current spending policies. Krakowski’s advice: Take the time to model different scenarios and work to understand the short- and long-term impacts of potential changes.

Navigating ESG Criteria

Another notable trend in endowment management is the rise of ESG investing. As CAPTRUST’s 2022 Endowment and Foundation Survey revealed, 57 percent of endowments and foundations believe ESG investments will increase in the next five years. Only 11 percent believe the trend will recede. Yet, in 2022, only 37 percent reported currently utilizing an ESG, impact, or mission-aligned investment strategy.

The difference is likely tied to uncertainty around ESG metrics. As Greenberg explains, “Investment committees want to be sure that ESG investing does not conflict with their fiduciary responsibilities. And if it doesn’t, the next question is: Does ESG stand to create equal or greater benefits than a traditional investment strategy?”

For committee members charged with ensuring perpetuity, these are good questions to ask. But answers are complex and multifaceted. ESG strategy success can be difficult to measure, and available data is often difficult to decipher. As Greenberg says, “Deciding which companies fit into an ESG strategy is sometimes easier said than done, especially considering the lack of standardized reporting. The same company may do well in terms of impact but have a poor rating when it comes to ESG.”

This can cause unwanted outcomes for an endowment, as the universe of securities that an ESG strategy would be selecting from is often dependent on screenings by these rating agencies. For example, consider an oil company that is the best in the industry when it comes to DEI practices, or a waste management company that is converting its fleet to natural gas. These companies may be changing rapidly, but the oil company is still drilling for fossil fuels and the waste management company is still contributing to CO2 emissions. Depending on the reporting outlet, each one could have a vastly different rating.

For organizations that decide to adopt an ESG strategy, it can be helpful to start by defining an intended focus area and how much flexibility the committee will accept regarding impact and improvement. Progress is easier to find than perfection.

Perhaps to narrow their focus or to avoid these screening issues, some endowments are choosing impact investing over ESG. An impact strategy focuses on making targeted improvements in select issue areas. It means seeking companies that are making a measurable societal or environmental impact alongside a financial return. Generally, these types of companies are in their early stages, focus on innovation, and are best accessed via alternative investments.

DEI Disconnect

DEI is another growing area of focus for higher education endowments. According to CAPTRUST survey data, in 2022, 68 percent of nonprofits prioritized DEI and 62 percent of nonprofit boards engaged in formal discussions about DEI practices. Among higher education endowments, DEI implementation ranges from increasing the diversity of endowment management teams to incorporating DEI considerations into investment decisions. Endowments are also paying more attention to demographic diversity among service providers. However, progress so far has been slow.

As Krakowski says, “Higher education is at the forefront of many DEI conversations. They’re putting in the work and planting seeds for the future, even if those efforts aren’t visible in their committees or suppliers yet.” As committee and board turnover happens, Krakowski says, DEI is top of mind for many endowment managers.

Most higher education institutions have already engaged in data-finding initiatives to establish DEI benchmarks. Greenberg and Krakowski say they’re now seeing institutions expand their definition of diversity beyond demographics to include things like profession, skill set, and diversity of thought. “The idea that diverse thinking creates better outcomes also applies to portfolio management,” says Krakowski. “If everyone on an investment committee is a financial professional, or everyone is an alumnus of the same institution, you are likely going to miss out on diverse perspectives.”

To create diversity of thought in investment decisions, endowment committee members are starting to look outside existing networks of colleagues and alumni to recruit a wider range of board members, committee members, and service providers. They are building pipelines now to increase impact later.

But DEI is only one part of preparing for an uncertain future. As higher education endowment managers continue to balance operating expenses with short-term goals and the need for long-term stability, fundraising, spending, and asset allocation must consistently be revisited. Economic and market conditions certainly impact these discussions, as do legislation, services available from providers, and the current social and environmental landscape.

Change is constant but not usually predictable. Navigating the endless stream of adjustments and transformations in endowment management means simultaneously focusing on the present and gazing out at the long-term future. It means being informed of trends and best practices to remain prepared but still adaptable. Armed with what they learn, endowment managers can make better financial decisions and potentially create better outcomes for both the endowment and the institution it supports.

Technology innovation and an unrelenting push toward a more digital world open us up to a range of cybersecurity risks. For retirement plan sponsors, it’s the risk of sharing financial and personal identifiable information across platforms and third-party service providers. With participant assets and retirement security on the line, these risks weigh heavily on many plan sponsors’ minds.

In April 2022, the Department of Labor released an article to assist plan sponsors in meeting their fiduciary obligations regarding cybersecurity. To fulfill these duties, plan sponsors are following some simple steps that help protect against potential breaches. One place to start is establishing a well-documented cybersecurity program that includes several critical elements, including the four pillars below.

Review and Monitor Service Providers

Careful review of service-provider agreements and contract terms is an important first step. It is also a good idea for plan sponsors to make sure they understand service-provider security practices and cybersecurity standards. Plan sponsors will want to explore past security incidents, legal proceedings related to the vendor’s services, and the provider’s response. Plan sponsors should also verify service providers’ insurance policies for cybersecurity and identity theft breaches.

Protect Plan Data

While recordkeepers and other service providers have an obligation to keep private information private, plan sponsors sometimes volunteer more information than is required. For example, oversharing Social Security numbers can open the door to potential misuse. While it is necessary to provide participant information for certain purposes, generally, less is more.

Insure Against Breaches

Two types of insurance address cyberbreaches: cybersecurity insurance and fiduciary liability insurance. Most employers have a cybersecurity insurance policy that covers the organization, but plan sponsors should make sure the policy specifically covers its retirement plan or plans.

Fiduciary liability insurance protects against claims of a breach, but employers and plan sponsors should ensure that the policy also covers claims of fiduciary breach due to cybertheft. This specific coverage may require a rider or separate policy.

An indemnification provision in service provider agreements is an added layer of protection. It requires the service provider to make a participant whole in the event of a data breach or dollars breach on the provider’s end. This type of provision ensures the organization is not held financially responsible, nor is an insurance claim needed. Keep in mind: If a contract contains this provision, the plan sponsor must take certain steps to prevent data breaches on their end.

Focus on Participants

Recordkeepers maintain safeguards to ensure the security of participant accounts, but individuals who have never logged in remain vulnerable. In fact, participants who rarely log in are less likely to change their passwords or notice any unusual account activity. Meanwhile, participants who have never logged in fail to establish user identification, passwords, and authentication methods to verify identity.

Plan sponsors and recordkeepers should communicate the benefits of logging in on a regular basis. This practice is not important only to ensure cybersecurity but also to help participants better understand their path to retirement security. The DOL suggests participants close or delete all unused accounts, use caution when accessing unsecured Wi-Fi networks, and be wary of phishing messages that ask for personal information.

Maintaining current contact information for each participant is another way to protect against cyberthreats. However, if contact information is out of date, this safeguard fails. With an ever-increasing digital environment and heightened focus on the safety of participants’ assets, cybersecurity in retirement plans will remain a DOL focus. Prudent plan sponsors will take appropriate actions now to protect their retirement plan participants and organizations.

If you sponsor a retirement plan, you likely know there is no uniform set of fiduciary rules that apply to all plan sponsors. Instead, fiduciary responsibilities for each institution depend on the type of organization and the state in which it operates. Since state laws vary, fiduciary responsibilities can range from nonexistent to comprehensive, or fall somewhere in between. With so much variation, it makes sense that plan sponsors may feel confused or overwhelmed by their legal duties.

Those who sponsor 403(b), 401(a), or 457(b) plans have additional reason to be puzzled: some of these plans are covered by the Employee Retirement Income Security Act of 1974, also known as ERISA, and others are not. ERISA is a federal tax and labor law, governed by the Department of Labor (DOL), that sets minimum standards for retirement plans and health plans in the private sector. The law does not cover retirement plans set up and administered by churches or government entities, such as tax-exempt healthcare organizations, local governments, or public school systems.

This means organizations that sponsor non-ERISA retirement plans are not subject to the law’s fiduciary standards. “But following ERISA best practices is generally still a good idea,” says Mike Webb, senior financial advisor at CAPTRUST. After all, Webb says, it’s not only the DOL that governs retirement plans; the Internal Revenue Service (IRS) and Security and Exchange Commission (SEC) also have jurisdiction. “The IRS does not have any fiduciary rules, but the SEC has many,” says Webb. In other words, organizations that sponsor non-ERISA plans are not governed by the DOL but are still subject to SEC regulations for fiduciary behavior.

As an example, Webb points to the SEC’s regulation best interest (BI) rule, which requires that financial professionals act in the best interest of their clients—similar to ERISA’s exclusive benefit rule, which says fiduciaries must act solely in the interest of participants and their beneficiaries. To comply with varied regulations from this patchwork of governing entities, many organizations opt to adhere to ERISA standards to ensure they are following best practices.

Why Follow ERISA Standards?

For organizations that are not subject to ERISA but choose to follow its standards, risk management is typically one part of the decision. Organizations can mitigate the risk of litigation by implementing due diligence processes in accordance with a written investment policy statement (IPS).

But another, perhaps bigger part of that decision is that ERISA best practices are designed to help create optimal outcomes for employees, says CAPTRUST Financial Advisor Michael Sanders. Nonprofit organizations, like many private sector organizations, feel a moral and ethical responsibility to be good stewards. They want to do the right thing for plan participants, and ERISA standards help them define what the right things are.

“ERISA standards are just good, healthy practices,” says Sanders. “Think about things like benchmarking your plan and not leaving investments in the plan that are no longer relevant or are underperforming. If these things are done right—if these best practices are followed—they’re going to lead to better results for your employees, whether you’re in the public sector or the private sector.”

ERISA standards help plan sponsors focus on their unique employee populations and work backwards to understand what participants will need to retire successfully. “First responders are a good example,” says Sanders. “People who work in police forces or in fire departments tend to retire about 10 years earlier than the average American because those are such physically demanding jobs. If you sponsor a retirement plan for first responders, you need to be set up to provide the best outcomes for this unique group, knowing they may need to retire long before the usual retirement age.”

Do ERISA standards help organizations protect themselves from legal risk? “They can,” says Sanders, “but that isn’t really the point. The point is to create the best possible outcomes for the people in your plan. Whether or not you are legally defined as a fiduciary, you are still responsible for and accountable to participants.”

Best Practices to Consider

Webb and Sanders offer six best practices for non-ERISA retirement plan sponsors to consider. These practices can help optimize outcomes for plan participants while also improving operational efficiency.

- Enroll in regular fiduciary training. “Look for ongoing training that is similar to ERISA training but also accounts for your state’s unique rules and regulations,” says Webb.

- Have written policies in place. This includes an IPS, a summary plan document, and an investment committee charter. A written charter gives your investment committee the power to make decisions about plan investments, service providers, and more.

- Implement regular investment committee meetings. Typically, this means once per quarter. Take minutes to document all decisions and the reasoning behind them.

- Commit to annual fee benchmarking. “You want to make sure that people are paying the right amount of money for each plan service,” says Sanders. “Reviewing fees on an annual basis will help you be sure that things aren’t drifting away from what’s reasonable and fair.”

- Do your investment due diligence. “Plan committees should be monitoring investments against certain benchmarks,” says Webb. For instance, you may choose to measure large-cap stock fund performance against the S&P 500 Index and core bond fund performance against the Bloomberg U.S. Aggregate Bond Index, two widely followed and representative indexes.

- Communicate and educate. “Participants should be notified any time you make changes to the plan, whether that means swapping out an investment or changing your processes to account for evolving rules and regulations,” says Sanders. “Remember that you are a trustee of participants’ assets, so it’s always a good idea to make sure they know what’s going on.”

Consolidation of recordkeepers is also a good idea, although some state laws require nonprofits to have more than one recordkeeper in place. “One recordkeeper is the best practice,” says Sanders. “Having two will often lead to additional work and can complicate plan administration and communication. And to the best of my knowledge, there is no data that says having more than one recordkeeper creates better results.” If your financial advisor is performing regular fee benchmarking, one recordkeeper is all you need.

However, Webb cautions, you’ll want to be aware of any applicable state laws that mandate additional service providers. For instance, “California and a few other states have any willing provider laws that say 403(b) plan sponsors have to enter into contracts with all qualified providers that are willing to accept their plan’s terms and rates.”

Depending on the state in which your institution operates, you may be required to adopt state laws that seem to contradict fiduciary best practices, including those listed here. Webb’s advice: “Wherever state law allows, follow the ERISA standard.”