Cultivating Confident Humility

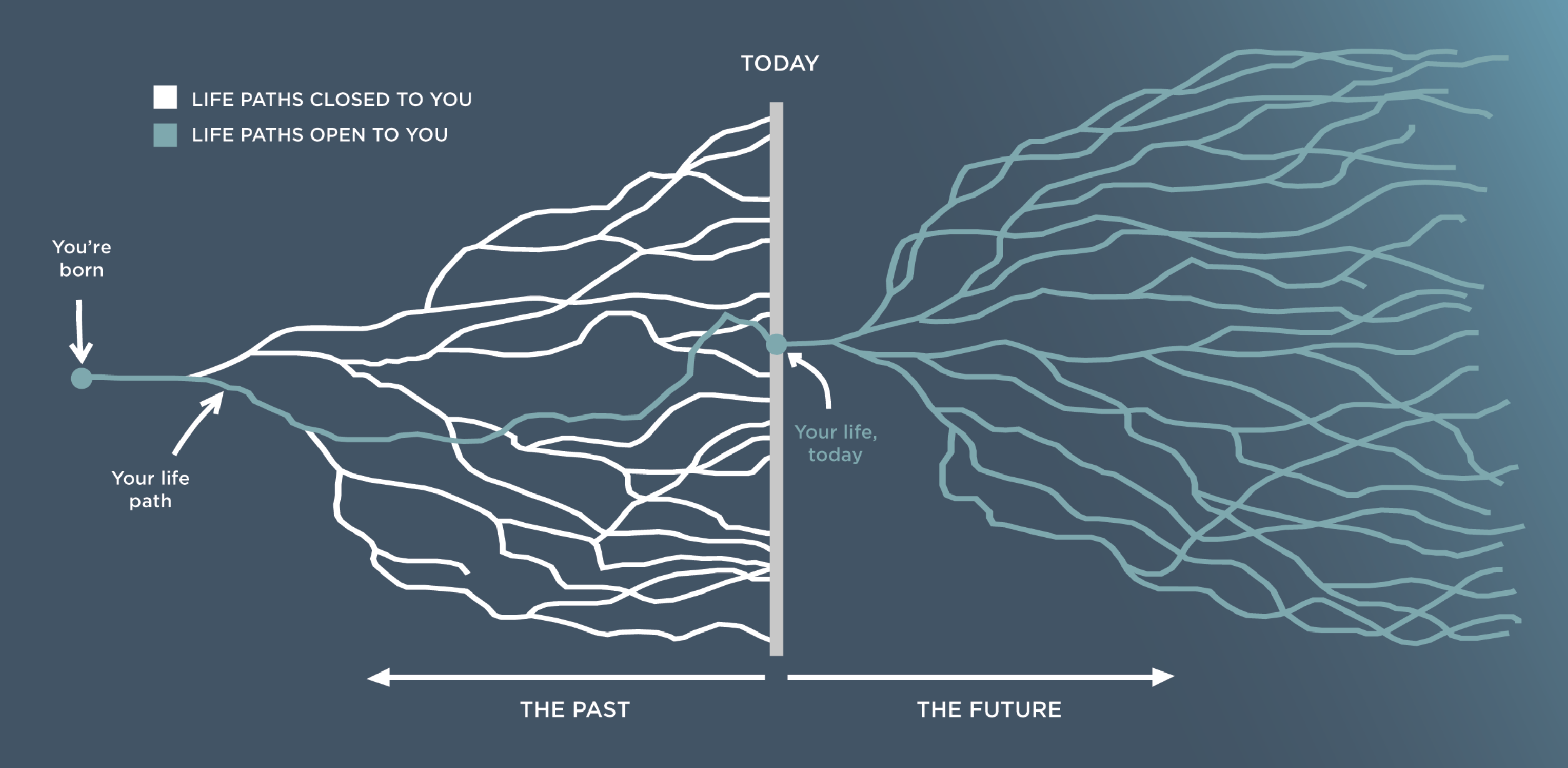

Investing requires making judgments about the future. But from where we stand today, the future consists of a range of possibilities. Elroy Dimson’s popular definition of risk—more things can happen than will happen—encapsulates this idea very well.

To deal with this uncertainty, most investors look backward to plot a forward course, connecting the historical dots to create a forward-looking story. However, we would caution that while this historical knowledge is valuable in making decisions about the future, it likely raises confidence more than predictive abilities.

Nobel Prize-winning psychologist Daniel Kahneman explains, “Confidence is a feeling, one determined mostly by the coherence of the story … even when the evidence for the story is sparse and unreliable.”

Because we enjoy the benefit of hindsight, we can weave together a forward-looking story that provides perfect clarity, giving us high conviction. However, that story may be based off a single path, providing a limited or, worse, a misleading picture. This is a very dangerous combination in the world of investing.

So how does CAPTRUST position for the future while acknowledging the ubiquitous disclaimer that past performance may not be indicative of future results? First and foremost, we approach all decisions with a mindset of confident humility. We have views and opinions—often strong opinions—but we acknowledge that we also have biases and limited information. We incorporate these views within a framework of guiding principles that surround how we think, how we act, and how we react.

1. Wisdom over Knowledge

Words are no match for an experience. A child who burns his hand will undoubtedly have a better understanding of the painful consequences of touching a hot stove than a child only warned by a parent. It is impossible to fully learn from others’ experiences because lessons learned from words lack the emotional weight carried by experiences.

The source of wisdom is often pain, and unfortunately, there are scars behind all these principles. Similarly, investing can only be learned by putting capital to work and experiencing the consequences of the decisions you make in an effort to grow capital. There is absolutely no way to simulate this learning. Real confidence—or “true intuitive expertise” as Kahneman describes it—stems from prolonged experience with quality feedback on mistakes. In the investment world, that feedback most frequently comes in the form of financial losses.

The smartest investors are not the most knowledgeable but, rather, the ones who know the limits of their knowledge because the market humbles them every day.

Inexperienced intelligence is a breeding ground for overconfidence because you have not learned what you do not know.

2. Comprehensive over Complicated

Most extreme investment errors occur when investors take simple concepts and add complexity. Financial experts can mathematically prove certain strategies have a high probability of success, but the complexity incorporated into these strategies frequently ends in catastrophe.

Gilbert Keith (G.K.) Chesterton, famed English writer, perfectly captured this fundamental risk in his book Orthodoxy when he stated, “Life is not an illogicality; yet it is a trap for logicians. It looks just a little more mathematical and regular than it is; its exactitude is obvious, but its inexactitude is hidden; its wildness lies in wait.”

A ship that has its center of gravity above the water line can sail smoothly for years but suddenly capsize in rough seas. That’s what complexity and leverage can do to a simple investment strategy.

Do not mistake complexity for comprehensiveness. Portfolios should be constructed utilizing understandable components combined to provide comprehensive exposure to a diversified set of economic return drivers (economic growth, real interest rates, inflation, credit, liquidity, currency, etc.).

3. Predictable over Surprise

Investing is an emotional roller coaster, and no one is spared from the ride. We all have bouts of anxiety and excitement, patience and impatience, and fear and greed. Successful investors find ways to control these emotions by managing their expectations. Psychologists theorize that surprises have a greater emotional impact than expected outcomes, especially negative surprises. This is called decision affect theory.

There is a downside to every investment. Acknowledging and defining this downside is critical in constructing portfolios. Understanding the risk associated can help an investor manage emotions. For your investment advisor, explaining the risk affords the opportunity to provide proactive education. Conversely, reactive explanations should always trigger an immediate review, whether the outcome was better or worse than expected.

Predictable outcomes allow for proactive education, which builds investor confidence. Conversely, surprises require reactive explanations, which can erode confidence.

4. Preparing over Predicting

Few people would ever find a guiding investment principle from the movie Roadhouse, starring Patrick Swayze. However, one line in the movie captures a critical element of how we approach the future. After one of the countless bar fights, Swayze’s character was asked if he ever lost a fight. His response: “A man looking for a fight is not as prepared as a man who is ready for one.”

Being prepared for multiple outcomes is suboptimal because the eventual path will always outperform the aggregate collection of potential paths. So why is positioning so important? Because it protects you from what you do not or cannot see.

In a blog post titled “Risk Is What You Don’t See,” published in January 2020, Morgan Housel noted, “How risky something is depends on whether its target is prepared for it. A big event people have time to prepare for can be handled without much fuss. A smaller one out of the blue can be deadly.”

Portfolio positioning should emphasize out-planning the market by preparing portfolios for the future rather than attempting to outsmart the market with short-term market-timing predictions.

5. Probability over Magnitude

Napoleon Bonaparte once said, “The greatest danger occurs at the moment of victory.” This “danger” is caused by successful outcomes raising confidence and higher confidence resulting in a new definition of “victory.”

Investors are notorious for constantly changing their definitions of success. When outcomes are better than expected, they rarely dial risk back and increase the probability of success. Rather, they move the victory bar higher and overconfidently continue down their paths, focused on what can go right without stopping to question what can go wrong. However, as mentioned previously, investing is an emotional roller coaster, and like a roller coaster, the slow grind higher can often be followed by a sudden terrifying freefall.

It is critical for investors to clearly define what success looks like in their portfolios. It is even more critical for investors to stop the game and celebrate if they are fortunate to be able to declare victory. Though, being content with your definition of success while watching others run the score up often requires a herculean effort.

Every decision should have a clear definition of success, and the focus should be on maximizing the probability of success, not the magnitude of success.

6. Net over Gross

Every investment decision contains multiple layers of costs. While the direct financial costs are most obvious, the emotional costs are often the most expensive. The financial cost of investing in stocks depends on the approach, but every equity investor pays the emotional price: volatility.

Portfolios typically represent historical sacrifices—trips not taken, cars not purchased, experiences not experienced—in the hope of a better future that includes retirement, a child’s education, or support of charitable causes. Consequently, witnessing those portfolios decline in value has a high emotional price. Unfortunately, it is impossible to know whether this emotional price is too high until after you’ve paid it. The cost associated with turning a potentially temporary decline into a permanent loss because the emotional price was too high can be exponentially higher than a management fee, but they are all costs.

Investment success can only be measured over time, net of all costs, including direct costs (e.g., transaction and management fees), indirect or frictional costs (e.g., timing and taxes), and often most impactful, emotional costs.

7. Portfolio over Pieces

The 2006 USA Basketball roster included numerous NBA All- Stars—LeBron James, Dwyane Wade, Chris Paul, etc.—and was led by legendary coach Mike Krzyzewski. This collection of the best of the best was the overwhelming favorite to bring home the championship. Despite the dramatic talent advantage, the U.S. lost to Greece, a team with no NBA players, in the semifinal. Countless examples exist in which teams with dramatic talent advantages are defeated by less-skilled players who play as a team rather than a collection of individuals.

Portfolios are similar. Far too often, investors focus on the individual pieces, trying to populate every portfolio position with the absolute best investment option in a certain asset class. However, like in sports, in which the better team has a collection of complementary players, portfolios should be constructed with complementary pieces to ensure appropriate diversification. Some pieces are for offense; other pieces are for defense. At times, a specialist may be needed to capture a specific opportunity.

When it comes to investing, it’s difficult to make definitive statements because the landscape is always evolving. However, there is one phenomenon that we are confident will always prevail: cycles. If everything in a portfolio is performing well at the same time, my greatest concern is how that portfolio will perform as the cycle turns.

An optimal portfolio is not necessarily a collection of the best individual pieces. Rather, it’s a collection of the right individual pieces.

8. Committee over Individual

We believe that CAPTRUST has a unique but extremely powerful competitive advantage. Over the course of our history, we have folded in more than four dozen successful firms. While we all share a common culture, each firm took a different path to success. As a result, we all have our unique scars of wisdom.

CAPTRUST is not a firm of firms. Rather, we are one unified practice. Under the CAPTRUST umbrella, we benefit greatly from this diversification of wisdom, increasing the confidence in our collective decisions.

None of us are better than all of us.

These nine guiding principles help shape how we think, how we act, and how we react. However, the most important piece to the success equation must also be factored in. That piece is time.

9. Time Horizon over Everything Else

Leo Tolstoy famously said, “The two most powerful warriors are patience and time.” From an investment perspective, the importance of time cannot be overstated. Time can be an investor’s biggest risk and biggest risk reducer. Too much time can provide financial challenges; too little time can and has been a major source of permanent value destruction. Time is not diversifiable, and what you do with it often defines investment success.

A physician friend of mine once told me that a doctor’s primary job is often to buy enough time to let the body heal itself. The application to investing is obvious. Appropriately diversified portfolios may experience bouts of weakness, but with sufficient time, our confidence is high they will recover.

Understanding how time impacts the risk profile of an investment decision ensures proper alignment between investment and portfolio time horizons.

There are no silver bullets, magic formulas, or crystal balls that can eliminate uncertainty about the future. All we can do is create a context for thinking, establish a framework for acting, be disciplined with our reactions, and allow time to heal any short-term wounds.