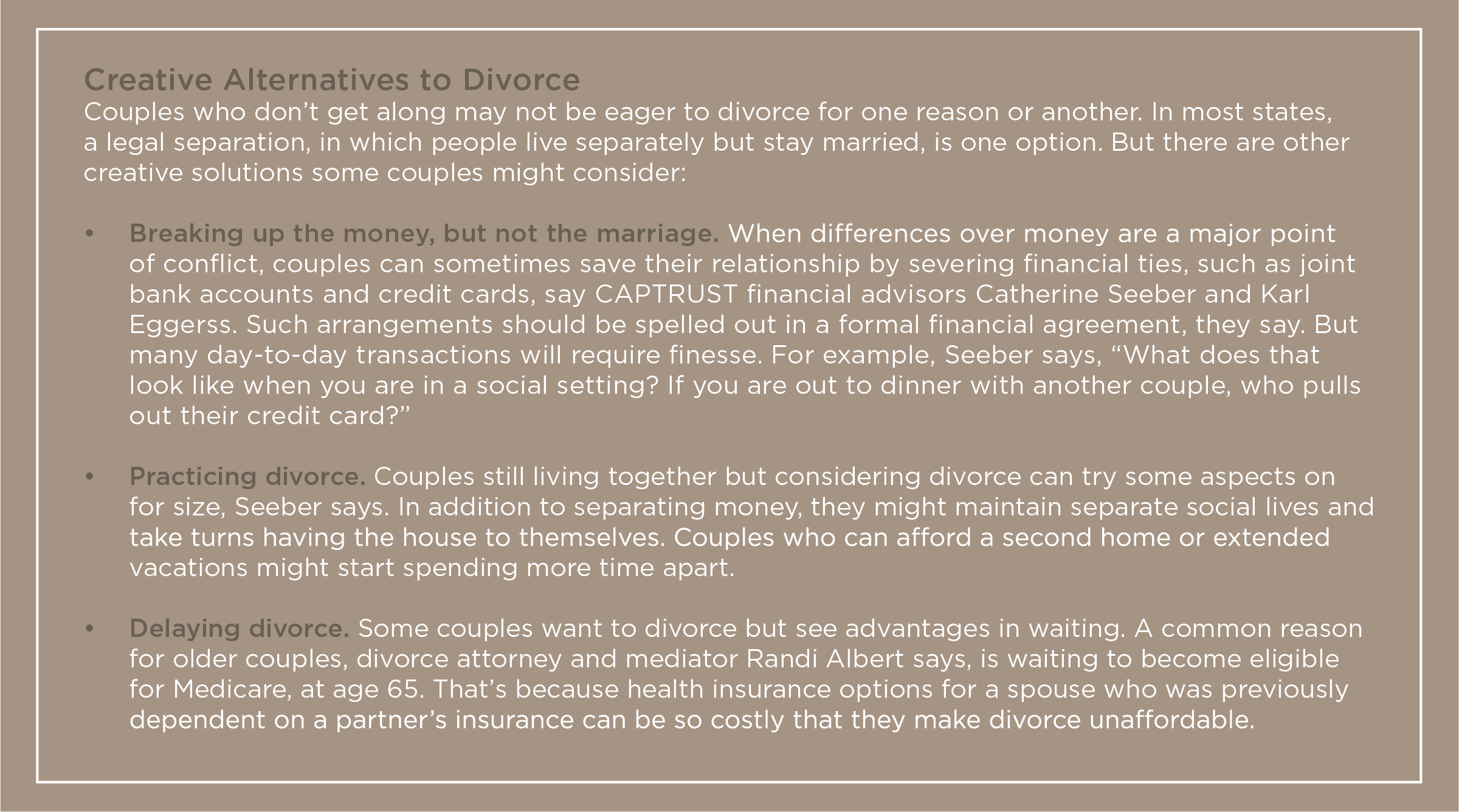

The Gray Divorce Boom

Frank blames herself, she says, for not knowing enough about her finances or divorce law and then rushing to complete the painful and costly process.

“I gave him free rein,” says Frank. “He did nothing wrong.” Frank lives in Hollywood, Florida, and has written two books: Divorced After 56 Years: Why Am I So Happy? and Life Has No Expiration Date: Misadventures of a Single Senior.

Divorce, at any age, comes with emotional costs. But, as Frank learned the hard way, a so-called gray divorce—a marital breakup after age 50—can also cost a lot of money, as years or decades of interrelated finances and acquired assets typically require extensive work to sort out.

“Divorce is definitely a financial hit for almost everyone,” and older couples face some extra challenges, says Randi Albert, an attorney who is a divorce mediator in Scotch Plains, New Jersey. The costs can be especially steep, experts say, for people who go into the process with too little information or planning.

Regardless of marital status, “it’s important to be aware of all your financial ins and outs, whether you are the money person in a relationship or not,” says Karl Eggerss, a CAPTRUST financial advisor in Boerne, Texas.

Even those who are happily married need to understand their personal finances to make good financial decisions. Yet Eggerss says he often sees couples rely on one person for financial management while the other partner remains disengaged.

CAPTRUST Financial Advisor Catherine Seeber, from Lewes, Delaware, agrees: “It’s common for one person to make all the financial decisions. I strongly encourage anyone who’s going through or considering divorce to talk to a financial advisor and understand all the things they need to gather to educate themselves. Otherwise, it can turn into a very emotional and reactive situation. Remember, a lot of irrevocable decisions are going to be made during this time.”

The Gray Divorce Trend

Gray divorce is much more common than it once was. Even as the overall U.S. divorce rate fell, the rate of divorce at age 50 and over doubled between 1990 and 2010, according to researchers at Bowling Green State University (BGSU). Since 2010, divorce rates over age 65 have continued to rise. Someone over age 65 was three times more likely to get a divorce in 2019 than in 1990.

More than one-third of all U.S. divorces now occur among people over age 50, researchers say. What’s causing all this later-life divorce?

Conventional wisdom says such divorces happen when a suddenly empty nest, a retirement, or a health crisis puts a rocky marriage to a test it simply can’t pass. But a recent study found no link between those transitions and post-50 divorce, says I-Fen Lin, a professor of sociology at BGSU.

Instead, Lin says, the trend is driven by generational shifts. Because baby boomers—now ages 58 to 76—entered adulthood just as divorce gained wide acceptance, they’ve remained more likely to divorce than generations before or after them. This is a generation that believes “it’s better to be alone than to be in an unhappy marriage,” she says. There’s also a snowball effect because remarriages are two and a half times more likely to end in divorce than first marriages. So remarried baby boomers often end up divorcing again. Today’s aging couples also live longer, giving them more time to divorce.

Another factor may be financial. According to Lin’s research, the odds of gray divorce are 38 percent lower for those with more than $250,000 in assets than those with $50,000 or less.

Lin and her colleague, Susan Brown, looked at the financial fallout of gray divorce and found a sobering picture, especially for women. Divorced women over age 50 see an average 45 percent drop in their standards of living after divorce, and men see a 21 percent drop. Men and women each lose about half of their wealth, including real estate, investments, savings, and other property, most likely as a direct result of divorce settlements.

If they remarry within a decade, most women regain their living standards and some of their wealth. But three-quarters stay single, Lin says. Remarriage does not help men regain their living standards or wealth. And because of their ages, gray divorcees have limited time to rebuild wealth in the future.

Do Your Homework

Fortunately, experts say, there are things you can do to soften such financial blows.

Eggerss says his first piece of advice is to take it slow unless there are strong reasons for haste. He likens the period around a marital breakup to the period around a death, when it’s wise to delay major life changes. “When people are under stress, they’re going to make really bad financial decisions,” he says.

That doesn’t mean you shouldn’t think about money. On the contrary, it’s crucial to do your homework on what assets, debts, income, and expenses you and your spouse have—and how a divorce might affect your bottom line, Eggerss and other experts say.

“I think a lot of people are putting finances on the back burner,” Eggerss says, “and then make this decision before they have really thought through whether they can afford to do it.”

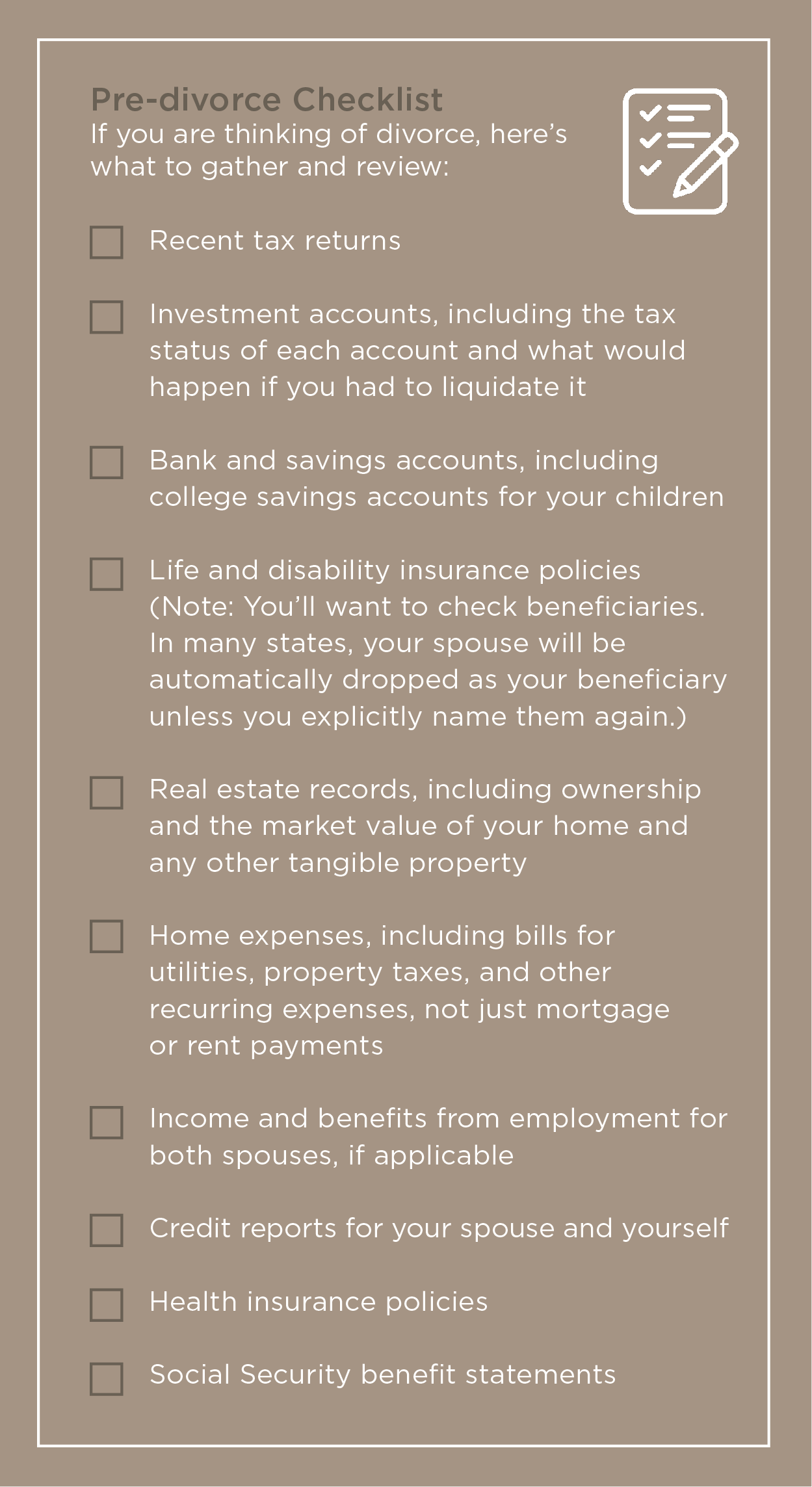

If you haven’t paid close attention to family finances in the past, it’s especially crucial to get up to speed. Start by gathering account passwords, Seeber says: “Ensure you have online access to anything and everything financial.” You will want to see everything from your spouse’s credit report to their Social Security statements.

Keeping communication open and civil will make information exchanges easier, Eggerss says. Whatever you do, he says, don’t try dirty financial tricks, like funneling money into new accounts you hope to hide from your spouse. Such maneuvers are likely to be uncovered, he says: “You are not going to get away with it.”

Negotiate a Settlement

If you decide to move forward with a divorce, you and your spouse might hire separate divorce lawyers and battle over details or hire a mediator and work together on an agreement. Randi Albert, the New Jersey mediator, says some couples litigate part of their settlement and use a mediator to work through less contentious issues.

Also important to know: Nine states—Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin— have community property laws that dictate an even split of all assets and debts built up during the marriage. Other states call for a fair and equitable split that considers factors like each spouse’s earning potential and contributions, such as child-rearing. Those rules apply if a couple hasn’t worked out their own property agreement before getting to court.

“People are more likely to follow an agreement that they’ve developed on their own, as opposed to one that was foisted upon them by the court,” Albert says. “So if you have the kind of relationship dynamic that allows you to work together, it’s definitely the way to go.”

Fairly dividing assets isn’t easy though. “It’s really not advisable to just put numbers on paper,” Seeber says, and decide, for example, that one spouse will take a house valued at $1 million and another will take investments valued at $1 million. You need to consider home maintenance costs and the tax hit you might take after an eventual sale, she says. If your money is tied up in a home, will you have cash available when you need it? Will you have enough credit to borrow in the future? If you are receiving an investment account, are proceeds taxable, or not? “You have to run the long-term projection to be able to say that, in 10 years, you really still are equal,” Seeber says.

Albert and her partner, family therapist Michele Weinberg, say they encourage divorcing spouses to run draft property agreements past separate financial advisors as well as separate attorneys.

Weinberg cautions that some gray divorcees will need to work years longer or go back to work after retirement to pay alimony or cover new living costs. “Sometimes, people who have never worked or have worked in a limited way now have to find a full-time job,” she says.

Couples who own a business together will face additional challenges. Will the business be sold, bought out by one spouse, or reorganized with two ex-spouse owners? The last is a fraught situation most people reject, Weinberg notes.

Divorce typically also means reconsidering everything from wills to plans for long-term care. Someone who expected a spouse to care for them in their later years will now need other options. That might mean moving in with a friend or jump- starting a move to an over-55 or assisted living community, says Eggerss.

Frank, the Florida divorcee and author, says she’s been able to stay happily single in her own apartment. She’s doing just fine now, she says. But she does share this advice for anyone going through a late-life divorce: “A second pair of eyes and ears, even from a trusted friend, can save you time, money, and grief. Don’t sign or agree to anything without having someone else review it.”