Investment Feature: Risk is Part of the Plan

By Eshani Gupte

What is the maximum decline you can withstand across your investment accounts before you seek a more conservative strategy? How flexible are your financial goals if your investments fall short of expectations?

These are two of the many questions a financial advisor may ask their client at the start of an advisory relationship. Although thinking about declines and shortfalls can be uncomfortable, the answers to these questions are critical in evaluating each client’s individual risk profile.

From an investor’s perspective, the goal is straightforward: earn sufficient returns to meet future financial needs.

From an advisor’s perspective, things are more nuanced. Advisors seek to deliver returns that meet a client’s unique financial goals on specific time horizons, while also carefully managing performance to the client’s unique risk tolerance and risk capacity.

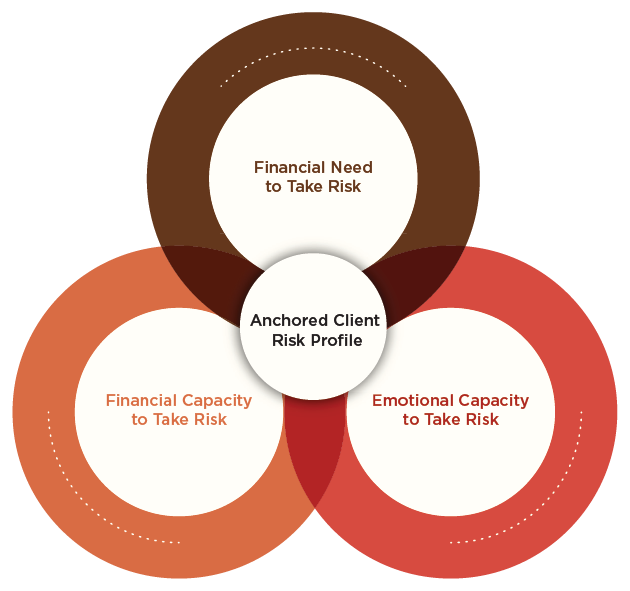

To do this, the advisor must combine a client’s risk profile (their financial and emotional capacity to endure certain investment outcomes) with risk-management practices, constructing a portfolio that is efficient, diversified, and consistent with the intended investment experience.

That’s one of the reasons investment professionals spend so much time thinking about risk: how to define it, how to explain it, and how to prudently manage it. For professional investors, the journey toward a client’s time horizon is just as important as the destination.

This article examines risk through two lenses: the client’s and the advisor’s.

How Individual Investors Define Risk

In its most basic form, risk is defined as exposure to danger and harm, or the possibility of loss. But this definition is overly simplistic because it implies that risk is unusual or avoidable, when in fact, it is both common and inevitable.

We face risk every single day—in small, almost unnoticeable ways, like sipping hot coffee while driving, and in more extreme ways, like jumping out of an airplane.

Degrees of risk vary based on the activity, the environment, and the individual involved. A skydiving instructor and a first-time jumper facing the same situation will experience it differently. For one, jumping is routine. For the other, it may be terrifying.

Whether you’re thinking about skydiving or investing, risk itself is subjective.

Investment risk is the possibility that an investment’s actual outcome will differ from expectations. This includes the potential to lose some or all invested capital.

But this definition is also simplistic. Real investment risk is complex, multifaceted, deeply personal, and frequently misunderstood. No single definition can encapsulate all investors’ tolerance or capacity.

And while there is a common misconception that investors can eliminate risk through careful selection or highly conservative strategies, the reality is that risk cannot be avoided, only managed to a level that a particular investor can reasonably and emotionally accept.

Several factors shape a person’s risk profile.

- Time horizon defines the length of time before invested funds are needed. Shorter time horizons generally warrant more conservative investments to protect invested capital. Longer horizons can allow for greater exposure to growth-focused or higher-risk investments.

- Financial goals are specific and actionable targets (such as purchasing a home or supporting a person in retirement) that define the purpose of the invested capital. In this context, risk is defined as failure to meet the intended objective.

- Liquidity needs determine what portion of assets must be accessible for near-term spending or unexpected expenses. Liquidity risk arises when investment losses coincide with the need for cash, potentially resulting in permanent loss of value.

- Risk capacity is the objective financial ability to withstand financial losses. It is a quantitative measure of financial resilience based on the individual investor’s income streams and financial stability, access to other assets, and ability to adjust their financial goals.

- Risk tolerance is its counterpart: a subjective and behavioral measure of how much uncertainty, market volatility, and loss an individual investor is willing to accept. Stated risk tolerance is often theoretical until it’s tested by real-world events.

Several less apparent forms of risk can be equally impactful to an investor’s long-term plan. These include shortfall risk (when realized returns are lower than expected and leave insufficient funds to meet financial objectives), inflation risk (purchasing power erosion from the failure to keep up with inflation), and longevity risk (in which returns fail to keep pace with financial goals due to external circumstances).

Taken together, these factors underscore why risk is neither simple nor static. Because investors experience and respond to risk differently, no two investors share the same risk profile. This makes a professional investor’s task increasingly complex as they work to combine stated goals with these elements to construct resilient portfolios.

Evolution Over Time

Adding complication is the reality that each investor’s relationship with risk is not fixed. As life changes, so do financial priorities and liquidity needs. Often, multiple objectives with different time horizons must be managed at the same time.

Consider a young couple, early in their careers. They want to buy a home soon, and they want to be prepared for retirement.

Given their circumstances, they may reasonably pursue a growth-oriented investment portfolio while retaining some element of conservatism that will lend them the liquid cash they need for a down payment. As their family grows, paying for school becomes another goal. Their investment strategy must adapt to accommodate this new goal and its time horizon.

Now consider an individual in her early 60s. Her income is stable, her kids have finished college, and now, she’s almost ready to retire. An unexpected change, such as the need to fund long-term care for an aging parent, can materially alter her liquidity needs and reduce her willingness to tolerate market volatility.

These examples underscore a critical reality. Risk is not just a market concept. It is life-driven and life-determined, and must continually adapt. Over time, portfolios must be recalibrated to stay aligned with financial goals, risk capacity, and risk tolerance.

Real-World Tolerance

Risk is often reduced to, or misunderstood as, volatility. Volatility is only one dimension of risk, but it often garners the most attention because it is the most easily observed.

Volatility is better defined as short-term price fluctuation driven by economic, political, corporate, or consumer events or data.

For example, we might note that market volatility was heightened in early 2026, driven by geopolitical events in the Middle East and shifting interest-rate expectations. This led to sharp, headline-driven swings in the S&P 500 Index.

Short-term, headline-driven market swings are an inherent part of investing.

True risk emerges when a person’s natural emotional response to volatility creates the potential for permanent loss or failure to meet stated financial goals. This can happen when people get spooked by market declines and withdraw money impulsively, thereby locking in permanent losses. Investment professionals can help clients look beyond volatility to maintain decision-making discipline, particularly around long-term goals.

How much volatility or market drawdown should investors be willing to endure? The answer depends on each individual’s unique risk tolerance. Remember, risk tolerance is a subjective measure. Often, it’s defined at the start of an advisory relationship via risk-profile questionnaires or personal conversation. However, it’s difficult to understand a person’s true risk tolerance until they’re faced with real-world volatility.

The reality of assets flowing out the door can change an investor’s perspective quickly. In this way, periods of market stress can validate true tolerance. Unfortunately, a person’s risk tolerance tends to correlate with recent market environments. Perceived risk tolerance is higher in up markets and lower in more volatile markets. This could be because, as humans, we tend to feel the pain of loss more acutely than we feel the joy of gain.

What matters is recognizing whether our stated tolerance aligns with our lived experience. If not, we need to reframe accordingly. Although risk cannot be fully eliminated, the level of risk in a portfolio should be bearable enough for a person to maintain throughout periods of market stress.

The Investment Professional’s Perspective

The investment advisor’s role in managing risk can be just as complicated as risk itself. After all, managing risk in a portfolio is not a one-time calculation. It is a core and continuous discipline.

First, the advisor must understand their client’s risk profile and financial objectives, then construct an appropriate investment strategy aligned to these priorities. They must continue to monitor and adjust risk exposure amid ongoing market events and shifts in investment positioning. Most importantly, they must clearly communicate the role that risk plays in each client’s portfolio.

Risk should never feel accidental. It must be intentional, understood, and appropriately compensated.

For investment advisors, failure often means a permanent loss of capital or the inability to achieve the desired level of return. These types of failure can have many drivers, including market volatility, forced decisions at inopportune times, misalignment between assets and time horizons, or inadequate liquidity when cash is needed.

To avoid these circumstances, professionals build and monitor portfolios with risk always in mind.

Connecting Risk to Portfolio Construction

One key investment idea says higher returns require more risk. But if higher returns were guaranteed, would the investment truly be risky?

Within this framework, lower-return investments are assumed to have lower risk. However—as you may have guessed by now—correlation between risk and return is not the sole consideration when predicting return potential.

The choice to avoid risk by holding excess cash or overly conservative assets introduces its own, separate forms of risk, including inflation risk and shortfall risk.

Also remember that all investments inherently carry the risk of an unlikely outcome that could lead to lower returns or asset losses. You’re probably familiar with the common disclaimer: Past performance does not guarantee future results. All investment involves risks.

Investment professionals manage these trade-offs by aligning investments returns with portfolio objectives, rather than investing in the highest-returning asset just to generate gains. Prudent portfolio design aligns assets to the client’s financial goals, liquidity needs, and time horizons.

Consider the same young couple from earlier. They have a growing family and three key financial goals: home purchase, college tuition, retirement. Their portfolio would need a combination of short-term, more conservative assets to meet the first goal, plus longer-term, higher-growth assets to help meet their goals for college and retirement.

Second, reconsider the woman who is caring for an ailing parent. Given her new and elevated liquidity needs, her portfolio should not be invested in illiquid assets, such as real estate, because she won’t be able to access their value when she needs it. Instead, her advisor is more likely to consider fixed-income assets with consistent yields.

Well-constructed portfolios recognize that different objectives can and should require different levels of risk.

Preparation Breeds Confidence

One more investment principle comes into play here: prepare, don’t predict.

Even the most well-informed and well-educated investment professional cannot predict what will happen in the future. Therefore, their goal is to make sure portfolios are prepared for a wide range of potential outcomes.

Stress-testing (also called scenario planning) under different economic and financial assumptions helps the advisor understand how portfolios may behave during downturns, how assets correlate under stress, and how financial flexibility could be impacted. Then, portfolios can be diversified accordingly, not only across asset classes but also across responses to various economic drivers.

Once a portfolio is constructed, the investment professional must manage risk on an ongoing basis.

Disciplined decision-making, particularly during difficult periods in financial markets, is more critical to long-term success than maximizing returns during stronger periods.

Preparation and planning can help investors avoid the sort of knee-jerk reactions that often lead to permanent losses. Preparation also enables adjustment, allowing investors to adapt as necessary when circumstances change.

Mitigation, Not Avoidance

Risk is a natural, unavoidable part of investing—and life. Its inevitability shouldn’t scare people away but should encourage thoughtful, intentional investment approaches that manage risk appropriately.

A skilled and trusted financial advisor can be a partner in the process. By viewing risk holistically and managing it proactively, advisors help investors stay focused on what matters, achieving long-term financial objectives with clarity and composure.

About the Author

Eshani Gupte is a manager in the CAPTRUST Investment Group, where she focuses on investment strategy and communications. Gupte brings more than a decade of investment research experience, having covered the technology, consumer discretionary, and real estate sectors in her previous roles at South Texas Money Management and Bloomberg LP.