Understanding Trump Accounts: A Flexible Planning Tool for Families

Families often look for ways to save and invest for a child’s future while balancing simplicity, tax efficiency, and control. One newer planning option is the Trump account. While less widely known than custodial accounts or 529 plans, Trump accounts can be a powerful tool when used thoughtfully.

What Are Trump Accounts?

A Trump account (TA) is a type of retirement account intended to give children a head start on long-term saving. As a result, it shares some features with traditional IRAs, with several key differences that apply until the child reaches age 18.

- Contributions are limited to $5,000 per year, with up to $2,500 permitted from an employer.

- Contributions may also come from the government (children born between 2025 and 2028 are eligible for a $1,000 contribution) or from a 501(c)(3) organization.

- Contributions from individuals are made on an after-tax basis, while contributions from employers, the government, and charitable organizations are made on a pre-tax basis.

- No earned income is required to contribute.

- No distributions are allowed, including returns of contributions, until the child reaches age 18.

- Investment options are limited to low-cost mutual funds or exchange-traded funds (ETFs) that track U.S. equity indices, such as the S&P 500 Index.

- Accounts can be opened with BNY Mellon while Robinhood Markets will design a Trump Accounts app and provide customer service.

When Does It Make Sense to Use a Trump Account?

Trump accounts are best suited for families who want to help their children begin saving for retirement at an early age. They may be especially compelling for parents of children born between 2025 and 2028, who are eligible for a one-time $1,000 federal contribution. Families may find additional value when an employer contributes to a child’s account, which is a feature not typically available in other savings vehicles for minors.

However, if a parent’s goal is to save for education or to set aside funds that can be used at any time for any purpose, a TA may not be the most tax efficient option.

529 plan accounts remain the gold standard for education savings. Like TAs, contributions grow tax-deferred, but the similarities largely end there. Withdrawals from 529 plans are tax- and penalty-free when used for qualified education expenses. By contrast, TA assets cannot be accessed before age 18, and distributions are taxed as ordinary income on a pro-rata basis, with the 10 percent penalty waived if used for higher education expenses.

Traditional custodial accounts offer the greatest flexibility. Assets can be used at any time and for any purpose without penalty. Like TAs, they are managed by a parent or guardian until the child is 18 or age of majority. Beyond that, the differences are significant. TAs offer tax-deferred growth, while custodial accounts generally do not provide preferential tax treatment beyond the kiddie tax rules. Custodial account assets also become the child’s property at the age of majority, whereas TAs remain subject to retirement account rules.

Case Study: Trump Account with Roth Conversion and Custodial Account

Another advantage of Trump accounts is the ability to convert the balance to a Roth IRA after the child turns 18. The following example compares outcomes at age 18 and age 60, assuming a Roth conversion, with a traditional custodial account.

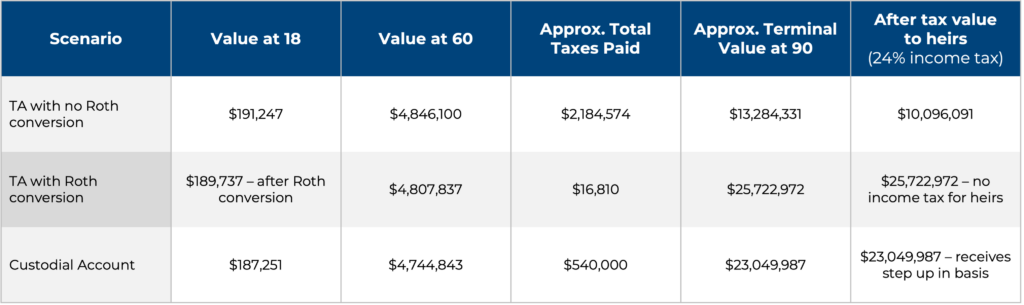

Assume Jane has had a TA since birth. She received the $1,000 contribution from the U.S. government, and her parents contributed the maximum $5,000 each year. Assuming an 8 percent rate of return, the balance in Jane’s TA at age 18 is $191,247, of which $90,000 represents contributions (basis) and the remainder is pre-tax growth.

If no further action is taken, the account balance grows to $4,846,100 by age 60, with only $90,000 of basis. Any withdrawals would be 1.8 percent non-taxable and 98.2 percent taxable at Jane’s ordinary income tax rate.

Assuming annual withdrawals of $200,000 to support retirement expenses, and accounting for both withdrawals and future required minimum distributions, Jane would pay more than $2.1 million in income taxes by age 90. Any remaining balance at her death would also be subject to income tax, which her heirs would owe as they distribute the account over a 10-year period.

Case Study Continued: Roth Conversion vs. Custodial Account

In same scenario, assume Jane converts the entire balance to a Roth IRA at age 18 and does not have other assets to pay the associated taxes. After accounting for ordinary income taxes and the 10 percent early withdrawal penalty, the Roth IRA would begin with a balance of $189,737 and grow to $4,807,837 by age 60. Her annual expenses of $200,000 would be covered with tax-free withdrawals from the Roth IRA. Any remaining balance would pass to her heirs free of income tax.

Now consider the same savings pattern from birth to age 18 in a custodial account. While there is no $1,000 government contribution, assume the same 8 percent rate of return. The account balance at age 18 would be $187,251 with a $90,000 cost basis. Jane can use these funds at any time and for any purpose, but in this example, she preserves the account for retirement.

Over time, the account may benefit from tax-loss harvesting and opportunities to increase the cost basis. By age 60, the balance grows to $4,744,843, and Jane begins withdrawing $200,000 per year. Withdrawals in excess of basis are taxed at long-term capital gains rates. Even if the basis never increased, taxes would be lower than under ordinary income treatment, given the maximum long-term capital gains rate of 20 percent. At Jane’s death, any remaining assets would receive a step-up in basis, allowing her heirs to inherit the account with no embedded capital gains tax liability and the flexibility to invest as they choose.

It’s important to consider potential pitfalls. If the 18-year-old is still a dependent, the kiddie tax rules may still apply to amounts converted to a Roth IRA. In addition, if there are no other assets (such as cash or taxable accounts) available to cover taxes on the conversion, the individual would need to withdraw additional funds from the IRA, triggering both income taxes and the 10 percent penalty, to complete the conversion. In many cases, a more efficient approach is to use outside assets to pay the tax or delay conversion until age 59 ½, though this may result in conversion at a at a higher tax bracket.

All values shown are hypothetical and assume an 8 percent annual rate of return for each scenario. Hypothetical performance has many inherent limitations. No representation is being made that any performance will or is likely to achieve the profits and losses similar to those shown. There are frequently sharp differences between hypothetical performance results and the actual results achieved by any particular investment strategy

Conclusion

As with all aspects of financial planning, understanding a client’s current circumstances and long-term goals is imperative. TAs are simply a new tool available to help families save for a child’s future. At minimum, opening an account to get the $1,000 federal contribution, if eligible, may be worth considering.

As illustrated above, when retirement savings is the primary objective, a TA—particularly when paired with a Roth IRA conversion—can be a compelling strategy. When integrated into a broader financial plan, TAs can complement custodial accounts and 529 plans, offering an additional pathway to long-term wealth building.

Source:

Resource by the CAPTRUST wealth planning team.